On November 19, 2021, on the website of the Dutch courts (De Rechtspraak) a very interesting judgment of the Court of Appeal of The Hague in the Joined Cases with case numbers: BK-19/00754 upto and including BK-19/00758, ECLI:NL:GHDHA:2021:2143 was published. The judgment already dates from October 27, 2021, but it was only published on November 19, 2021.

In the underlying case the taxpayer and the tax authorities a.o. are disputing whether or not a currency exchange gain that the ‘taxpayer’ realized on so-called Forwards Swap Agreements is to be attributed to the foreign permanent establishment of the ‘taxpayer’. We say ‘taxpayer’ because the permanent establishment is actually the permanent establishment of a subsidiary that is included in the fiscal unity of which the taxpayer is the parent entity.

Next to the matter of the attribution the currency exchange gain realized over the Forward Swap Agreements the taxpayer and the tax authorities are disputing whether interest that has been paid on an intercompany/inter fiscal unity loan must be taken into account when determining the taxable income that is to be attributed to the PE for the prevention of double taxation for the years 2006 and 2007.

In this article we will focus on the dispute regarding the attribution of the currency exchange gain realized on the Forward Swap Agreements.

Facts of the underlying case

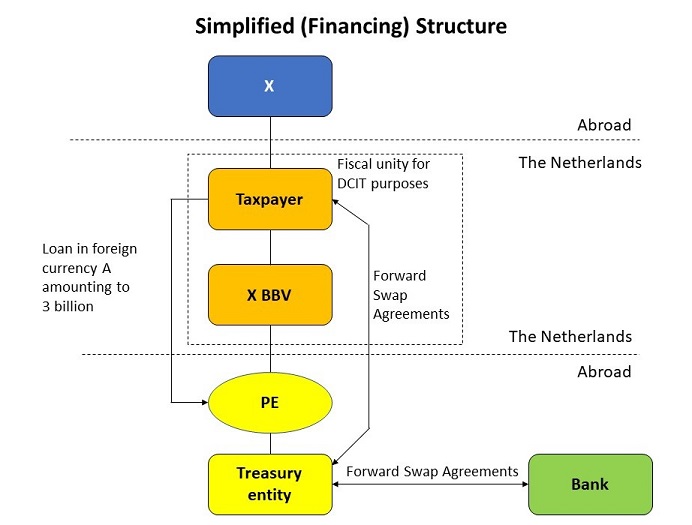

The Dutch taxpayer is part of the international X Group. The headquarters of the X Group is a non-Dutch resident.

The group undertakes various activities in the Netherlands. The Dutch and Belgian trading activities are performed by X BBV. In addition, the group has three logistics centers in the Netherlands. The group employs approximately 400 employees that work in the Netherlands.

The taxpayer is a wholly owned subsidiary of X. X is incorporated under foreign law. X functions as the international holding company of the group.

The taxpayer has a 100% interest in X BBV. X BBV is part of a fiscal unity for Dutch corporate income tax (DCIT) purposes of which the taxpayer is the parent company.

Until October 2004 the group’s financing activities were performed by the Swiss permanent establishment of the taxpayer.

Since June 15, 2004, X BBV has had a (foreign) permanent establishment (hereinafter: the permanent establishment or PE). The PE acts as the group’s treasury center. For this the PE employed an average of 20 employees (FTEs) in the relevant years. These employees were involved in the group's financial back-office activities. The PE acquired the shares in the entity “Treasury”, which was incorporated under foreign law and which was residing abroad. In the relevant years Treasury had an average of 3 employees who were mainly involved in the financial front office activities.

In the Annual Accounts of the PE, under the header “Accounting of revenue” the following is stated:

“As net revenue, the company reports the actual value of the administrative services invoiced to X, Treasury and the taxpayer. Invoicing takes place in accordance with signed service agreements and is based on underlying costs and the agreed market-based surcharge.”

In the context of the group restructuring that took place in 2004, the receivables and debts that were previously attributed to the Swiss PE of the taxpayer transferred by the taxpayer to the PE (of X BBV) against the recognition of debt in October 2004. This transfer resulted in the taxpayer getting a receivable on X BBV amounting to the balance of the group receivables and debts (the receivable) amounting to 3 billion (which is 3 billion denominated in a foreign currency). To this end, on September 30, 2004 the taxpayer and X BBV/the PE concluded five loan agreements. The group receivables and debts were subsequently contributed by the PE on the shares in Treasury. The loan payable to the taxpayer and the shares in Treasury were allocated/attributed to the PE of X BBV. The taxpayer included the corresponding loans receivable in its balance sheet.

In 2005, employees of the PE identified a currency exchange risk on the loan that was included in the (stand-alone) 2005 Annual Accounts of the shareholder (the taxpayer). These stand-alone Annual Accounts were prepared in euros. In order to eliminate this currency exchange risk, Treasury entered into so-called Forward Swap Agreements with a bank. Subsequently Treasury entered into mirroring Forward Swap Agreements with the taxpayer, of which it sent internal confirmations to the taxpayer. In some cases these confirmations were signed for approval on behalf of taxpayer. In other cases no signature for approval was required. Until receiving the confirmations, the taxpayer was not aware of the existence of the internal Forward Swap Agreements with Treasury to which it was bound.

As a result of the hedging instrument(s) described above (hereinafter also: the hedge), the currency exchange risk on the loan receivable was borne by Treasury. As stated above Treasury on its turn hedged this risk by entering into Forward Swap Agreements with a bank . During the existence of the various Forward Swap Agreements, an increase or decrease of exchange rate of the foreign currency against the euro is neutralized at the level of the taxpayer by a mirroring result on the internal Forward Swap Agreements.

In a letter dated May 26, 2010, the taxpayer gave the following reply to questions raised by the tax inspector regarding the background of the hedge:

“As you know, in 2004 the taxpayer provided a loan to X BBV. This loan amounts 3 billion denominated in foreign currency A (the “Loan”). This Loan was subsequently used by the (foreign) permanent establishment of X BBV (“the PE”). Now that this Loan is denominated in foreign currency A, whereas the taxpayer prepares its annual accounts in euros, the treasury department of the group, which is placed in the PE, has identified a possible currency exchange risk that is incurred with respect to the Loan. PE therefore instructed Treasury to enter into a number of so-called Forward Swap Agreements with a bank (the “Hedge”). Subsequently, Treasury entered into mirrored contracts with the taxpayer. The total of the different Forward Swap Agreements corresponds to the nominal value of the existing loan note receivable, as a result of which this loan note receivable that the taxpayer has outstanding is hedged to Euros.”

When preparing the 2005 Annual Accounts the taxpayer’s management discovered a material amount of results stemming from these Forward Swap Agreements. These results have subsequently been reported to PE and to Treasury. The persons involved abroad then concluded that the hedging instruments tried to hedge a currency exchange risk that did not exist at a group level and that (because of the existence of a fiscal unity for DCIT purposes) would also not arise for tax purposes. As of that moment, Treasury has no longer extended the various Forward Swap Agreements. The settlement of the existing external Forward Swap Agreements took until 2010.

During the existence of the internal Forward Swap Agreements, in the period from 2006 until 2010, a total profit of EUR 59,827,801 has been realized on these Forward Swap Agreements by the fiscal unity. This profit can be broken down as follows over these respective years:

|

2006 |

-/- € 18.386.000 |

|

2007 |

€ 18.624.000 |

|

2008 |

€ 45.222.801 |

|

2009 |

€ 13.529.000 |

|

2010 |

€ 838.000 |

The results realized on the Forward Swap Agreements were not included in the Annual Accounts of the PE and they were also not taken into account for foreign tax purposes.

During the years 2006 through 2010 X BBV incurred the following interest costs with respect to the loan:

|

2006 |

€ 12.153.000 |

|

2007 |

€ 15.072.000 |

|

2008 |

€ 17.745.000 |

|

2009 |

€ 18.540.000 |

|

2010 |

€ 21.192.000 |

These interest costs have been included in the result of the PE. For the years 2008, 2009 and 2010, the deduction of these interest costs was denied by the tax authorities of the country in which the PE was located. However, the interest deduction for the years 2006 and 2007 has not been adjusted in the country where the PE is located.

The dispute

The Dutch tax inspector has attributed the results realized over the internal Forward Swap Agreement to the Dutch taxable income of the taxpayer. Whereas the taxpayer is of the opinion that these results should be allocated to the PE.

Secondly parties are disputing whether based on Article 15ac, Paragraph 5 of the DCIT Act the interest that has been paid on the loan must be taken into account when determining the taxable income that is to be attributed to the PE for the prevention of double taxation for the years 2006 and 2007. However as discussed above, in this article we will not elaborate extensively on this discussion. The final decision of the Court of Appeal is that in the situation in which no fiscal unity would exist the loan between the taxpayer and X BBV would also not be attributable to the permanent establishment of X BBV. Therefore the Court judges that also in situations as in the underlying case (in which a fiscal unity exists) such loan, and therewith the interest costs/income cannot be attributed to PE.

From the considerations of the Court

The taxpayer argues that the District Court erroneously judged that a causal and functional-economic relationship exists between the loan and the Forward Swap Agreements. To this end (summarized) the taxpayer has argued the following. Since from a commercial-economic and tax perspective the Forward Swap Agreements did not hedge any currency exchange risk, they cannot related to any asset or liability. Therefore based on a functional criterion and consequently based on the Significant People Functions (hereinafter: the SPF-criterion) they are to be attributed to PE (abroad) and not to the parent entity of the fiscal unity (the taxpayer). PE is the group's treasury center, and as such by virtue of its activities it decided to enter into unnecessary Forward Swap Agreements. Based on the SPF-criterion, the results coming from these transactions are therefore attributable to PE. The fact that in the underlying case the SPF-criterion must be used is in accordance with the Authorized OECD Approach (AOA) as described in the 2010 OECD PE Report on the Attribution of Profits to Permanent Establishments and with the Profit Allocation of Permanent Institutions Decree (the Decree of the Dutch Secretary of State from January 15, 2011) (Hereinafter: the Decree), which follows the AOA. The taxpayer is of the opinion that a legitimate expectation that the allocation should take place on the basis of the SPF-criterion is derived from the aforementioned Decree. In the event that the Forward Swap Agreements would be associated with another asset or liability (quod non), these Forward Swap Agreements can only be associated with the shareholding in Treasury, since the loan does not exist for tax purposes and since a currency exchange risk is incurred with respect to the shareholding in Treasury. The shareholding in Treasury is part of the assets of PE and therefore the taxpayer is of the opinion that also the Forward Swap Agreements are part of PE’s assets. In the event that, notwithstanding the foregoing, it nevertheless must be considered that a functional economic relationship exists between the Forward Swap Agreements and the loan, then to the opinion of the taxpayer based on the SPF-criterion the loan must also be attributed to PE.

The 'as if' approach which is laid down in Article 15, Paragraph 1 of the DCIT Act means that the taxpayers that are part of a fiscal unity continue to exist as tax subjects, but that for the taxable object they are treated as if they are a single taxpayer. During the existence of a fiscal unity this is also the starting point for the calculation of the reduction for which avoidance of double taxation should be granted (see Article 15ac, paragraph 4 of the DCIT Act). It is the subsidiary (X BBV) that carries on part of its business abroad through a permanent establishment. Based on the AOA, it is determined which part of the benefits of that enterprise must be allocated to the permanent establishment for the application of the tax treaty as concluded between the Netherlands and the country in which PE is located. The activities and assets of X BBV as a subsidiary, including the permanent establishment of the subsidiary, are deemed to form part of the activities and assets of the taxpayer. The reduction for the avoidance of double taxation which the Netherlands must grant with respect to the benefits attributed to the PE is therefore taken into account at the level of the taxpayer as the parent company of the fiscal unity.

The way in which a fiscal unity functions means that receivables and debts between the parent and its subsidiary are eliminated. It is then by no means obvious that the assets associated with such a receivable (in this case the Forward Swap Agreements) are to be attributed to another member of the fiscal unity (in this case that would be X BBV) than to the company in which stand-alone balance sheet the receivable is included (in the underlying case the taxpayer). That would also be inconsistent with the fiscal unity's principle that the parent company and the subsidiaries continue to exist as tax subjects. In the underlying case, also the circumstance arises that that other company (X BBV) is the debtor. It is not apparent that application of the AOA would lead to such an allocation, whereby an asset belonging to the assets of one legal entity is to be allocated to the permanent establishment of another legal entity. Contrary to what the taxpayer argues (in the alternative), from this it follows that the receivable cannot be attributed to the permanent establishment.

The foregoing entails that for the purpose of the allocation of related assets the receivable continues to be part of the assets of the taxpayer and the debt remains part of the assets of X BBV/PE. Taking into account the nature of the Forward Swap Agreement as such, and also taking into account the relation that exists between the receivable and the Forward Swap Agreements, according to the Court a causal link exist between the two. Therefore the Court considers that the Forward Swap Agreements should also be attributed to the taxpayer (cf. HR 23 January 2004, ECLI:NL:HR:2004:AI0670, BNB 2004/214). Contrary to what the taxpayer (primarily) argues, the fact that, on closer inspection, the Forward Swap Agreements did not appear to hedge any currency exchange risk, cannot lead to the conclusion that no (longer) a relation exists between the Forward Swap Agreements and the receivable. The taxpayer’s argument that since the receivable does not exist for tax purposes, the hedge relates to the shareholding in Treasury, which is part of the assets of the PE, is also incorrect. The Court of Appeal therefore agrees with the District Court judgment and is of the opinion that the results realized on the Forward Swap Agreements are not part of the taxable profit of (X BBV’s) PE.

The Court of Appeal also rejects the taxpayer’s claim on the principle of legitimate expectations. Contrary to what the taxpayer argues, the Decree does not provide any basis for the position that with respect to assets that from a stand-alone position belong to the parent company of a fiscal unity, it must be determined by using the SPF-criterion whether these assets can be attributed to the permanent establishment of a subsidiary that is included in the fiscal unity. The attribution of profits to permanent establishments based on the SPF-criterion as described in the Decree therefore (translated to the present case) only refers to assets that on a stand-alone basis belong to X BBV.

The full text of the judgement of the Court of Appeal in the underlying (only available in the Dutch language) can be found here.

Copyright – internationaltaxplaza.info