As a tax adviser I have never been a big fan of structures that include a dual resident entity and in general I would not advise a client to use dual residency in a structure. I might consider using a dual resident entity if the entity would have a certain minimum presence in the jurisdiction that it was relocated to and if next to that its board of directors would consists out of qualified experienced individuals of which a majority would be a residing in the jurisdiction to which the entity moved would want to move its (tax) residency. This to minimize the risk that tax authorities might question where the place of effective management of the entity is located. For the same reason I have never been a big fan of using trust offices or their employees as directors of group entities.

On February 6, 2023 on the website of the Dutch courts a judgment of the Lower Court of Zeeland-West-Brabant from January 27, 2023 was published. In the underlying case the combination of the taxpayer being a dual resident entity and the hiring of a trust office to provide directory services creates a perfect storm resulting in the Court concluding that at least for the years 2012, 2013 and 2015 the taxpayer was not a resident of Malta, as it intended to be, but of the Netherlands.

Legal context

In the Dutch corporate income tax (DCIT) Act it is arranged that if the incorporation of an entity has taken place under Dutch law, then for the purposes of the DCIT Act the entity is always deemed to be a resident of the Netherlands. (An exception is made for a few articles of the DCIT Act).

The tie-breaker rule as laid down in Article 4, Paragraph 4 of the Dutch-Maltese DTA arranges that where a person other than an individual is a resident of both States it shall be deemed to be a resident of the State in which its place of effective management is situated.

Summary of the base facts

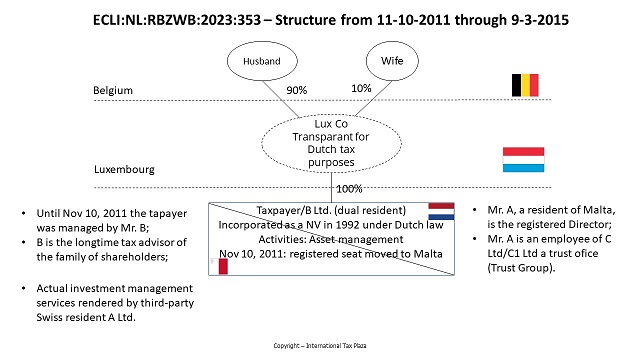

On September 1, 1992 the taxpayer was incorporated as a NV (public limited company) under Dutch law. Since December 7, 2011 all shares in the taxpayer are held by the Company shareholder and his wife. For 90% by the Company shareholder and for 10% by his wife wife. These individuals hold the shares in the taxpayer through a Luxembourg-based body (Hereafter: LuxCo) that is considered to be transparent for Dutch tax purposes. The Company shareholder and his wife have been living in in Belgium since the end of 2011. The total outstanding shares amounts to 100,000 and the total nominal value of those shares amounts to EUR 45,000.

The taxpayer’s main activities consist of asset management. To this end, services are provided to the taxpayer by a Swiss resident company (Hereafter: A Ltd.). In this respect on April 14, 2011 an investment management agreement was concluded by van Lanschot on behalf of the taxpayer and A Ltd. The fees that A Ltd charged for its services amount to a 0.35 % fee plus 15 % of the performance above 7 % hurdle. In 2012 only the basic fee of 0.35 % was charged, which amounted to EUR 111,469.37. From that we understand that the total assets that A Ltd managed on behalf of the taxpayer during the year 2012 amounted to approximately to EUR 32 million.

As of November 10, 2011, the registered seat of the taxpayer was moved to Malta. As of that date, the taxpayer is registered in Malta as B. Ltd. and Mr. A is registered with the Chamber of Commerce as a director of the taxpayer. Mr. A lives in Malta and works for C. Ltd., after a name change now called C1. Ltd. C1 Ltd. is a Maltese trust office (Hereafter: the Trust Group).

Until November 10, 2011 the taxpayer was managed by a BV, which in its turn was managed by Mr. B. For several years Mr. B has been the tax adviser to the family of shareholders.

Already since prior to 2011 the authorized representative 1 (To me it is not completly clear whether Mr. B and representative 1 are one and the same person. If not: then representative 1 is also a Durch resident which by coincidence has the same profession as Mr. B) and his colleagues who are all affiliated with belastingadviesbureau NV (Hereafter: the Dutch tax advisory firm) have been involved in the various restructurings of the taxpayer.

A Principal Party Agreement dated November 11, 2011 has been concluded between the Trust Group and the Company shareholder. Next to that a Management Agreement dated November 11, 2011 has been concluded between the Trust Group and the taxpayer. Since November 10, 2011 the taxpayer has been registered at the successive Maltese addresses, where also the Trust Group is/was registered.

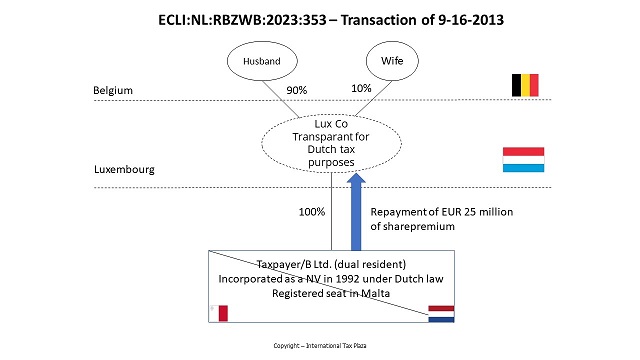

As per September 16, 2013 the share premium reserve of the taxpayer amounts to EUR 29,865,880 and the taxpayer does not have negative profit reserves.

During a shareholders’ meeting that took place on September 16, 2013 it was decided that an amount of share premium of EUR 25,000,000 to pay back to its shareholder (LuxCo) bringing the share premium reserve after repayment to EUR 4,865,880.

On 20 July 2015, the interested party changed its legal form from a public limited company (NV) to a private limited company (BV) under Dutch law.

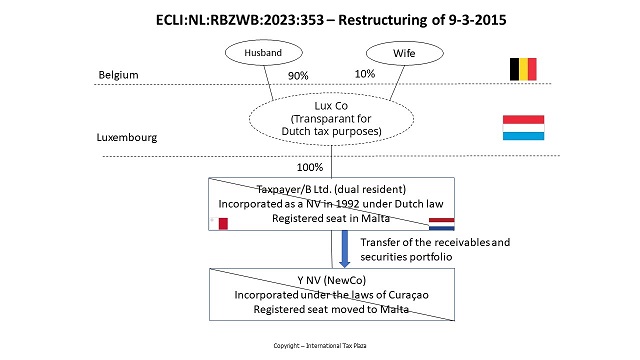

On September 3, 2015 a new entity (Y NV) was incorporated under the laws of Curaçao. The taxpayer holds a 100% interest in Y NV. Later the name of the Y NV was changed to A NV and its registers seat was moved to Malta. Mr. A was appointed as director A NV. The taxpayer’s receivables and securities portfolio have been transferred to A NV.

On December 15, 2015 the legal form of the taxpayer was changed from a BV (private limited company under Dutch law) a to a Kumpani Privati under Maltese law.

The contested assessments

For the year 2012 the Dutch tax authorities have raised an ex officio Dutch corporate income tax assessment for a taxable profit of EUR 309,550.

With respect to the ‘profit distribution’ that was made on September 16, 2013 the Dutch tax authorities raised an ex officio dividend withholding tax assessment amount to EUR 3,750,000 (15% x 25,000,000) of dividend withholding tax and EUR 733,541 of interest.

For the year 2015 the Dutch tax authorities have raised an ex officio Dutch corporate income tax assessment for a taxable profit of EUR 301,110.

The taxpayer in the underlying case appealed against the aforementioned assessments.

The judgment of the Court

To start the with the most important: the Court denied the appeal of the taxpayer.

According to established case law, the place where an entity is led and governed is to be understood as the place where key decisions relating to the activities of that entity are taken, where the final responsibility for these decisions is borne and from where instructions are given to the persons working within the entity. Whoever has the day-to-day management with respect to the implementation of the aforementioned is not relevant for determining where of the place of effective management is located. It is up to the inspector to establish and make plausible the facts and circumstances from which it follows that in the years in question the actual management of the taxpayer was not exercised by its statutory board, but by someone else.

The Court is of the opinion that the inspector has made it plausible that in 2012, 2013 and 2015 the place of effective management of the taxpayer was located in the Netherlands. According to the Court the relevant facts and circumstances, considered in conjunction, point to actual leadership in the Netherlands exercised by the authorized representative 1 and Mr. B.

Interesting is that in its considerations the Court states that for its conclusion that in 2012, 2013 and 2015 the place of effective management of the taxpayer was located in the Netherlands it also took into considerations facts and circumstances from other years because it is plausible that they shed light on the actual situation in the years 2012, 2013 and 2015.

Facts and circumstances that made the Court come to this conclusion

So what facts and circumstances are crucial for the Court’s conclusion?

In the concluded Principal Party Agreement and the Management Agreement, the trust office is in fact almost fully indemnified against regular liabilities of a director and that only in exceptional, predetermined circumstances it could refuse to implement certain decisions. In the opinion of the Court, this is a strong indication that the statutory board of directors did not operate independently and did not bear final responsibility for decisions taken. In the opinion of the court, this conclusion is reinforced and supported by a number of elements, which are discussed below.

On July 10, 2015 a general meeting of the taxpayer took place in Malta. In this general meeting the incorporation of new subsidiary in Curacao (“NewCo”), the transfer of assets and liabilities from the Company to NewCo and the transfer of the effective management of NewCo to Malta were decided. The Court notes that according to the e-mail correspondence, the documentation, including board decisions, were prepared and drawn up by employees of representative 1 who work at the Dutch tax advisory firm. In addition, the Court sees that the detailed minutes of the meeting - containing a representation of who was present, how the meeting went and which board decisions were taken - are attached to an e-mail which was sent on July 10, 2015 at 11:39 am. However, according to the e-mails of the previous day, the meeting was not scheduled until late afternoon and representative 1 had not yet landed in Malta at the time the minutes of the meeting were shared. The Court agrees with the tax inspector that this indicates that the decisions were actually taken in the Netherlands and that these decisions were then formally ratified by the statutory board by signing in Malta.

With respect to the investment management agreement which was concluded on April 14, 2011 between the taxpayer and A Ltd the Court notes the following. This agreement concerns the management of a significant part of the assets of the taxpayer. The inspector argues that on November 10, 2011 the statutory board of the taxpayer (Mr. A) ratified this agreement for the future, while Mr. A did not have access to the agreement. The Court notes that the statutory board ratified this agreement on November 10, 2011, but that no documents are available that show that prior to 2013 Mr. A had a copy of the agreement.

In addition, in the opinion of the Court, the other communication with A. Ltd. gives further insight into the actual course of events regarding the way key decisions regarding the taxpayer are taken. The Court notes that on September 15, 2015 the statutory board has sent an e-mail to A Ltd. In which it does not provide substantive answers to questions raised by A Ltd regarding the restructuring of the taxpayer, but replies that the restructuring was “proposed by PwC”. The same applies to the email exchange with Mr. B regarding the question whether or not interest should be charged over the only receivable the taxpayer has on its the ultimate shareholder.

The inspector also argued that the statutory board annually only spent 15 to 19 hours regarding the taxpayer. The taxpayer contested this and argued that annually Mr. A spent an additional 20 hours on the taxpayer. The Court concludes that the statutory board (Mr. A), annually spent 15-19 hours per on the taxpayer. Other than signatures on various documents the Court found no concrete indications in the very extensive file that these hours were spent on making key decisions. The Court also included in its judgment the extent of the (very) limited hours accounted for by the director (annually 15-19 hours) and the amount of the compensation received (annually EUR 1,500 - EUR 2,500). In the opinion of the court, such a low remuneration in combination with such limited hours accounted for is a further indication for the conclusion of the Court (that the place of effective management of the taxpayer was located in The Netherlands).

A few takeaways

In its considerations the Court starts by stating it also took into considerations facts and circumstances from other years because it is plausible that they shed light on the actual situation in the years 2012, 2013 and 2015. Unfortunately the Court does not further specify to which facts it refers. We however feel that the Court might a.o. refer to the fact that until November 10, 2011 the taxpayer was managed by a BV, which in its turn was managed by Mr. B. who was still heavily involved with the taxpayer after the taxpayer’s registered seat was moved to Malta. Furthermore we feel that the Court means to state that for its decisions regarding the assessments raised for the years 2012 and 2013 it also took into account the way in which the group restructuring that took place in 2015 was handled.

Another thing that this court case shows is the importance that if individuals that are residents of another jurisdiction than the ‘chosen’ jurisdiction are involved in the effective management of an entity it is of the utmost importance that evidence is available that these individuals were actually present in the country where the decision is supposed to be taken. One can think for example a clear appointment in the individual’s calendar, airplane/train tickets, hotel and restaurants bills, check-in time of the office building where the meeting will take place. The more, the better This to avoid that a discussion might arise that the individual that actually takes the important decisions was not even in the country at the moment that the important decisions were taken.

Another takeaway might be that saving money on services to be rendered by a trust office might come back to hunt you. But to be clear: in our view they underlying judgment goes further than cases in which a dual resident company is involved or structures in which trust offices are involved. In the underlying case the facts clearly seem to indicate that the Maltese director of the taxpayer was not actively involved, if involved at all, in the group restructuring that took place in 2015.

In our view it is preferred that a majority of the board exists out of residents of the jurisdiction in which the registered seat of the entity is located. Furthermore it is preferred that the foreign resident individuals that act as (registered) directors of foreign subsidiaries, dual resident or not, are capable, qualified individuals that get remunerated in accordance with their qualifications and experience. Furthermore it is advised that with respect to important decisions a paper trail (e-mail correspondence, meeting summaries, summaries of telephone calls) is kept that clearly shows the active involvement of the local registered directors of the foreign subsidiary in the discussions concerning these decisions as well as in the decision making itself. In the underlying case it would for example have been helpful if the Mr A (the Maltese resident that acted as the registered director of the taxpayer) would:

1. have participated in the discussion that led to the restructuring that took place in 2015;

2. would have been the person that had asked PWC to advise on the intended restructuring;

3. would have participated in meetings/conference calls in which the intended restructuring was discussed with PWC;

4. would have participated in the meeting/conference call in which the final advise of PWC was discussed.

Personally we are flabbergasted that although, or perhaps even better, because, several tax advisers were extensively involved in the management of the taxpayer the underlying case looks like a perfect textbook example to show first year international tax advisers on what could all go wrong when setting up a dual resident entity in a structure or when using a trust office to render directory services to a subsidiary.

Obviously the taxpayer in the underying case can still appeal against the Court's judgment.

Here you can find the full text of the judgment of the Lower Court of Zeeland-West-Brabant from January 27, 2023 as published on the website of the Dutch courts.

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)