On May 16, 2022 on the website of the Dutch courts (rechtspraak.nl) a judgment of the District Court of Zeeland-West-Brabant was published (the judgment in Case: AWB - 21 _ 2426 (ECLI:NL:RBZWB:2022:2432). And although it is only a judgment of a District court, it still is a very interesting judgment. The case regards a structure which was used to take over Dutch and Belgian satellite television providers, which were sold a few years later again. In the judgment the facts of the underlaying case are described very extensively, so in this article we will summarize the facts.

The underlying case regards the appeal(s) against the following additional dividend withholding tax assessments that the tax authorities have imposed on the ‘taxpayer’:

|

Year |

Tax |

Penalty |

Interest due |

|

2015 |

€ 3,367,362 |

€ 5.278 |

€ 641,753 |

|

2017 |

€ 14,520,035 |

€ 5.278 |

€ 1.807.421 |

We put taxpayer between quotation marks because the tax assessments are imposed on an entity residing in Luxembourg, whereas the additional assessments were imposed for distributions made by A BV, an entity incorporated under Dutch law and a resident of the Netherlands. However, since the distributions, A BV was first merged into A S.à.r.l. which on its turn was merged into the ‘taxpayer’.

The taxpayer and the Dutch tax authorities dispute several issues, but in this article we will focus on the question whether or not one of the taxpayer’s predecessors (namely A BV) abused Union law (EU law) in an attempt to avoid that Dutch dividend withholding tax had to be withheld over certain dividend distributions made by this predecessor.

Summary of the facts

As stated above, the judgment contains a very extensive description of the facts. However, sometimes it looks like small, less important, details of the facts are missing. Below we will give summary of the facts.

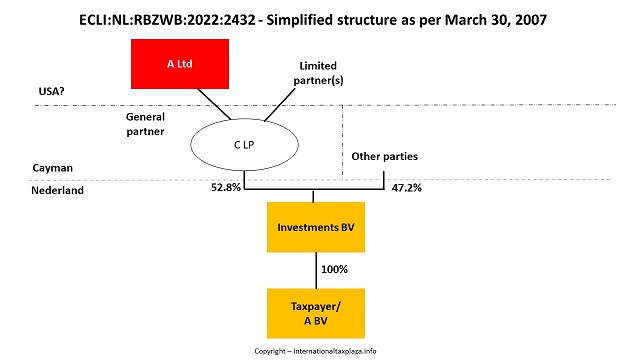

The underlying case regards a structure that is used by a US-based private equity firm (A LLC). In 2007 the A LLC incorporated a structure to take over Dutch and Belgian satellite television providers that were either operated by A BV itself, or by subsidiaries of A BV. The structure A LLC incorporated in 2007 included a.o. C LP, a limited partnership that was established under the laws of the Cayman Islands and that was a resident of the Cayman Islands. A Ltd was the general partner of C LP. Unfortunately the facts do not state under the laws of which jurisdiction A Ltd was established. Nor does it contain any information regarding the jurisdiction of which A Ltd was a resident. C LP, together with several other parties established Investments BV (unfortunately the judgment does not contain any information regarding the other parties involved). Investments BV was established under Dutch law and was a resident of the Netherlands. C LP had an interest of 52.8% in Investments BV. Investments BV in its turn had an (100%?) interest in the taxpayer’s predecessor (A BV). A BV was established under the laws of the Netherlands and was a resident of the Netherlands.

On November 1, 2013 C LP, A LP, Investments BV and the tax authorities agreed on an Advance Tax Ruling (ATR). The ATR stipulates, among other things, that C LP is considered to be transparent for Dutch tax purposes and that no dividend withholding tax on the basis of Article 1, Paragraph 7 of the Dutch dividend withholding tax Act in conjunction with Article 1, Paragraph 1 of the Dutch dividend withholding tax Act is due over profit distributions made from Investments BV to C LP.

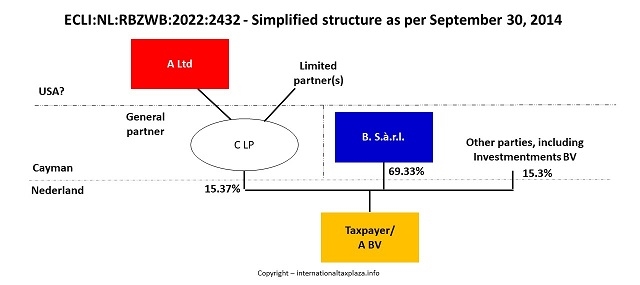

On July 9, 2014 the members (ITP: We would expect either the shareholders or Members of the Board) of Investments BV decided to sell A BV to a French private equity company (French company). Because it was unfamiliar with the industry, the French company demanded that C LP and Investments BV would remain associated with A BV as minority shareholders for a minimum period of two years.

On September 30, 2014 Investments BV delivered 69.33% of the shares in A BV to B. S.à.r.l., an intermediate holding company of the French company. Also on September 30, 2014 Investments BV distributed the remaining shares in A BV to its members (ITP: probably the court meant shareholders instead of members). As of September 30, 2014 C LP directly held 15.37% of the shares in A BV.

On September 30, 2014 the shareholders of A BV concluded a shareholders agreement. For as far as relevant the text of this shareholders’ agreement reads as follows:

“Initial Board

4.7 At Completion, the Board will consist of the following nine (9) Directors:

(a) Person 1 as chairman of the Board and as French company Director;

(b) Person 2, Person 3, Person 4 and Person 5 as French company Directors;

(c) Person 6 and Person 7 as C. S.à.r.l. Directors; and

(d) Person 8 and Person 9 as Investments BV Directors.

(…)

Board decisions to be taken by a majority

4.14 Resolutions of the Board shall be passed:

(a) at a duly convened and quorate meeting, by a simple majority of the Directors present or represented (…)

(…)

Intention to achieve an Exit

9.1 The Parties confirm their intention and commitment to work to achieve an Exit at an appropriate time in the future. Each Investor and the Company agrees to consult together with a view to determining a suitable time to effect an Exit. Subject to the other provisions of the Agreement, no Exit may take place without the prior written consent of French company, and French company shall, subject to its other obligations in this Clause and the Lock-in Period, generally determine any process initiated with a view to achieving an Exit, (…).

MINORITY LIQUIDITY RIGHT

14.1 After the Lock-in Period, C. S.à.r.l. or Investments BV may, by notice in writing to the Company and the other Investors (a “Liquidity Notice” ), require French company and the Company to comply with Clause 14.2 in respect of all of the relevant Investor’s Shares and that relevant Investor’s Coop Proportion of the Coop’s Shares (together, the “Liquidity Shares” ). Following receipt of a Liquidity Notice from the other Investor, C. S.à.r.l. or Investments BV (as applicable) may, by notice in writing to the Company and the other Investors delivered within 10 Business Days of the date of such Liquidity Notice (a “Participation Notice” ), elect to require French company and the Company to comply with Clause 14.2 in respect of all of the relevant Investor’s Liquidity Shares. (…)

(…)

14.2 During the Liquidity Period, each of French company and the Company shall use alle reasonable efforts to procure a Liquidity Event to be effected at the Relevant Price. Such Liquidity Event may include:

(a) procuring the acquisition by another person of the Liquidity Shares at the Relevant Price;

(b) to the extent legally permissible, causing the Group to undertake a buyback, redemption or dividend payment in respect of the Liquidity Shares at the Relevant Price, including without limitation by causing the Group to undertake a refinancing or incur additional indebtedness to fund such buyback, redemption or dividend. Following such event, each Party shall do all such acts and things as are necessary to put the Parties in the position they would have been in had such event been a buyback of all of the relevant part of (as determined by reference to the proceeds received by each holder of Liquidity Shares as a result of such Liquidity Event) the Liquidity Shares at the Relevant Price; or

(c) causing the Group to undertake an Initial Public Offering at such a price that will, immediately following completion thereof, imply a valuation of the Liquidity Shares equal to at least their Relevant Price (and each Shareholder which is not a Relevant Investor irrevocably and unconditionally agrees that each holder of Liquidity Shares shall have priority with regard to the allocation of Shares to be sold on completion of such Initial Public Offering),

(…)”

Annex 6 to the shareholders agreement provides an overview of the definitions used. In it a.o. the following is stated:

““Lock-in Period” the period of 24 months commencing on the date of Completion;

“Completion” the completion of this Agreement, (…)”

In the beginning of 2015 the French company has requested the other shareholders in A BV to agree with a dividend distribution of € 6.100.000 to be made by A BV. On February 3, 2015 Person 10 (the CFO of A BV) has sent an e-mail in this respect to Person 7 and Person 11, both employed by C. S.à.r.l. According to the website of C. S.à.r.l. Person 11 is “Managing Director, responsible for European tax restructuring and compliance”. This e-mail read as follows:

“Please have a look at the minutes and calculation of the dividend distribution via A BV.

I guess we need to withhold for all DR’s.

Agree?”

On February 3, 2015 Person 11 replied a.o. the following:

“One point on the withholding though, as we now own direct from [company] , we would also have a 15% withholding. We had always planned to introduce a new holding company and were on the way to doing this but did not expect a dividend quite so early.

If it’s ok I will look into putting this in place in the next few days but will also check the requirements on withholding (to see if it is required).”

On February 9, 2015 Person 11 sent an e-mail to Person 10 which reads as follows:

“We always intended to put in place a Lux entity to hold our interest in CDS (A BV) and if the timing works we will try and do that now (so as soon as possible, should be early next week).

If we do this then there should not be any withholding tax on the dividend payment to B. S.à.r.l.”

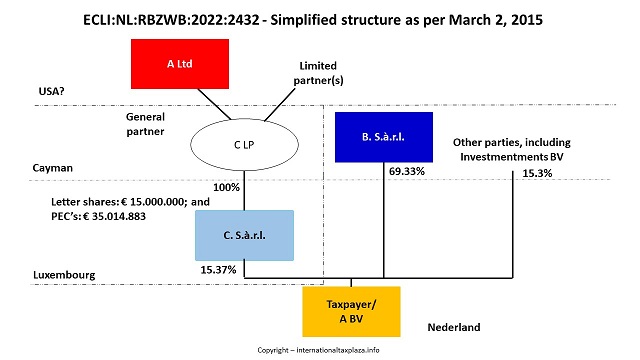

On February 12, 2015 C LP established C. S.à.r.l. C. S.à.r.l. is an entity established under Luxembourg law and is resident in Luxembourg. 4 persons were appointed to serve on the initial board of C. S.à.r.l. Two of these persons were employed by C. S.à.r.l.: Person 11 and Persoon 12 (according to the website of C. S.à.r.l. “Director, Taxation”.

From its date of establishment, C. S.à.r.l. registered at the address of a trust office. On December 15, 2015 C. S.à.r.l. moved to a so-called multi-tenant building, which is a building in which various companies are housed. No housing costs were included in C. S.à.r.l.’s annual accounts for the financial years 2015 through 2017.

On March 2, 2015 C LP transferred the shares it held to C. S.à.r.l. per notarial deed. In return C. S.à.r.l. issued letter shares and Preferred Equity Certificates (PECs) to C LP. In the 2015 annual accounts the shares in A BV were valued at € 50.014.883, of which € 15.000.000 was allocated to the letter shares and € 35.014.883 to the PECs.

On March 11, 2015 A BV distributed a dividend of € 6.100.000, of which € 937.299 was distributed to C. S.à.r.l. (dividend 1). No (Dutch) dividend withholding tax was withheld, nor paid, over the dividend distribution made to C. S.à.r.l. In a dividend withholding tax return filed by A BV the distribution made to C. S.à.r.l. was reported.

On April 9, 2015 the Board of A BV approved a refinancing of a bank debt and a dividend distribution of € 140.000.000. The shareholders’ resolution regarding the dividend distribution was taken on July 28, 2015. € 21.511.778 of the dividend distribution of that date was made to C. S.à.r.l. (dividend 2). No (Dutch) dividend withholding tax was withheld, nor paid, over the dividend distribution made to C. S.à.r.l. In a dividend withholding tax return filed by A BV the distribution made to C. S.à.r.l. was reported.

In the course of 2015, C. S.à.r.l. paid € 569,014 of interest over the PECs and repaid € 20,930,986 (together payment 1). These payments were made from the funds obtained via dividend 2. In 2016, C. S.à.r.l. paid €76,853 interest over the PECs to C LP and repaid €723,147 on them (together payment 2). The total of Payment 1 and Payment 2 is 99.3 percent of the total of Dividend 1 and Dividend 2.

On March 9, 2017 C. S.à.r.l. sent a Liquidity Notice to a.o. A BV. For as far as relevant the text of this Liquidity Notice reads as follows:

“Pursuant to clause 14 (Minority Liquidity Right) of the Shareholders’ Agreement, we hereby serve this notice on you as a Liquidity Notice and request that French company and the company accordingly comply with clause 14.2 of the Shareholders’ Agreement in respect of all of C. S.à.r.l. ’s Liquidity Shares.”

On March 20, 2017 also Investments BV issued a Liquidity Notice.

The Minority Liquidity Right was executed on December 22, 2017. The total issued share capital of A BV was valued at € 63,000,000 (€ 3,500 per share). A BV paid a total of € 175,999,471 under the denominator 'Distribution', of which € 96,800,234 was due to C. S.à.r.l. (payment 3). In A BV’s shareholders' resolution of December 22, 2017 it is stated, insofar as relevant:

“2. Background

(…)

2.5 It is proposed to declare a distribution from the freely distributable reserves to C. S.à.r.l., Investments BV, Person 10 and Person 13 on the Shares in the aggregate amount of EUR 175,999,471.30 (Distribution)

2.6 It is further proposed to reduce the issued and outstanding capital of the Company by means of a cancellation (intrekking) of the Shares (Cancellation) against a payment on the Shares of the aggregate amount of EUR 5,028.70 (Repayment).

2.7 The Company shall pay the Distribution and Repayment, as follows:

(a) to C. S.à.r.l. - EUR 96,803,000 (EUR 2,765.80 as repayment and EUR 96,800,234.20 as distribution):

(…)

3 Resolutions

3 1 The General Meeting resolves to the Distribution, the Cancellation and the Repayment and to:

(a) have the Company declare the Distribution. The Distribution will be payable as per the date thereof; and

(b) hereby reduce the issued and outstanding share capital of the Company by means of a cancellation of the Shares as per the date hereof.

(…)”

The Board Resolution of December 22, 2017 states a.o.:

“2. Background

2.5 The general meeting of shareholders intends to declare a distribution from the freely distributable reserves to C. S.à.r.l., Investments BV, Person 10 and Person 13 on the Shares in the aggregate amount of EUR 175,999,471.30 (Distribution).

2.6 The general meeting of the Company further intends to reduce the issued and outstanding capital of the Company by means of a cancellation (intrekking) of the Shares (Cancellation) against a payment on the Shares of an aggregate amount of EUR 5,028.70 (Repayment).

2.7 The Company shall pay the Distribution and Repayment, as follows:

(a) to C. S.à.r.l.: EUR 96,803,000 (EUR 2,765.80 as repayment and EUR 96,800,234.20 as distribution);

(…)

3 Resolutions

3.1 The Board approves the Distribution, Cancellation and the Repayment in accordance with Sections 2:208 paragraph 6 and 2:216 of the Dutch Civil Code, (…).”

On December 28, 2017 C. S.à.r.l. paid an amount of € 2.393.037 of interest over the PECs to C LP. At the same date C. S.à.r.l. repaid the remaining amount of PECS that was still outstanding (€ 13.360.750). Furthermore, C. S.à.r.l. repurchased, and subsequently cancelled, the letter shares it issued on March 2, 2015 for €81,011,175.

A BV filed a (Dutch) dividend withholding tax return on 17 January 2018 regarding the payments made to Investments BV, Person 10 and Person 13 under the denominator 'Distribution'. In this dividend withholding tax return an exemption has been claimed regarding the payment made to Investments BV. Over the payments made to the two other shareholders it is stated that 15 percent dividend withholding tax is being withheld and it is stated (via checking a box) that it regards the repurchase of own shares. On payment 3, made to C. S.à.r.l., no dividend withholding tax was withheld and paid. With respect to this payment that was made on January 17, 2018, a 'Declaration dividend withholding tax - Exempt distributions to foreign beneficiaries in subsidiary situations' (‘Opgaaf dividendbelasting - Vrijgestelde uitkeringen aan buitenlandse gerechtigden in deelnemingssituaties’) was included as an appendix to the dividend withholding tax return. In such declaration the nature of the dividend payment cannot be stated. In the declaration, on behalf of the distributing entity it is stated that the conditions of Article 4, paragraphs 2, 3 and 4 of the Dutch dividend withholding tax Act have been met.

Dividend 1 and 2 and together with payment 3 amount to a total of € 119.249.311. Payment 1 and 2 together with on-payment 3 amount to a total of € 119.064.962. The difference between the income and outgoing payments at the level of C. S.à.r.l. therefore amounts to € 184.349. In total therefore 99.84% of the payments received by C. S.à.r.l. was paid on to C LP.

According to the annual accounts of C. S.à.r.l. for the years 2015 through 2017, apart from the interest payments on the PECs, C. S.à.r.l.’s costs in those years amounted to:

|

Year |

Amount |

|

2015 |

€ 81.359 |

|

2016 |

€ 27.681 |

|

2017 |

€ 67.507 |

|

Total |

€ 176.547 |

For 2015 it concerns ‘notary fees’, ‘legal fees’, ‘tax advisor fees’, ‘bank fees’, ‘COC’ and ‘tax license fees’.

For 2016 it concerns ‘legal fees’, ‘tax advisor fees’, ‘bank fees’, ‘register of commerce’, ‘administrative expenses’, ‘wages’ (€ 10.975), ‘social security costs’ (€ 1.513), ‘director fees’ (€ 2.200) and ‘registration fees’.

For 2017 it concerns ‘notary fees’, ‘legal fees’, ‘tax advisor fees’, ‘bank fees’, ‘liquidation fees’, ‘register of commerce’, ‘administrative expenses’, ‘wages’ (€ 13.716), ‘social security costs’ (€ 1.786) and ‘director fees’ (€ 2.590).

On October 18, 2018 C LP liquidated C. S.à.r.l.. The only activities that C. S.à.r.l. has developed during its existence were holding shares in A BV, receiving amounts from A BV and paying these amounts on to C LP.

The tax inspector is of the opinion that the sole purpose of interposing C. S.à.r.l. was to avoid Dutch dividend withholding tax. The inspector is of the opinion that A BV wrongly applied the withholding exemption with respect to dividend 1, dividend 2 and payment 3 to (all made to C. S.à.r.l.). Therefore the tax inspector imposed the additional assessments, imposed penalties and issued the interest decisions.

From the considerations of the court

Withholding exemption incorrectly not applied? Abuse of EU law?

Parties are disputing that C. S.à.r.l. is entitled to proceeds of dividends 1 and 2 and of payment 3 (all together: the payments). Nor are they disputing that the conditions, as laid down in Article 4, Paragraph 2 of the Dutch dividend withholding tax Act, for the withholding exemption to apply are met with respect to the payments. The inspector however argues that despite this the withholding exemption still does not apply:

(i) on the ground that C. S.à.r.l. is not the beneficial owner as meant in Article 4, Paragraph 4, whether or not in combination with paragraph 7, of the Dutch dividend withholding tax Act;

(ii) because of abuse of law; or

(iii) because there is abuse of Union law.

Because this last argument is the most far-reaching argument of the three, the court will deal with this argument first. For this argument the inspector mainly relies on the T-Danmark judgment (CJEU February 26, 2019, ECLI:EU:C:2019:135).

The court states first and foremost that the CJEU has ruled that a Member State must refuse to apply the provisions of EU law if those provisions are not invoked to achieve their objective but to obtain an advantage under EU law, while the conditions for claiming this advantage are only formally met. (consideration 72 of the T-Danmark judgment)

When asked at the hearing, the interested party stated that the application of the withholding exemption does not constitute an advantage under EU law, because the Netherlands grants the withholding exemption more broadly than required by the Parent-Subsidiary Directive.

The court is of the opinion that in this case the application of the withholding exemption constitutes an advantage under Union law as referred to above. Parties are rightfully not disputing that the withholding exemption as laid down in Article 4, Paragraph 2 of the Dividend withholding tax Act concerns an implementation of the Parent-Subsidiary Directive. Insofar as there is an implementation, the withholding exemption is therefore in any case an advantage under Union law. The mere circumstance that the Netherlands grants the withholding exemption more broadly than is required by the Parent-Subsidiary Directive does not alter the fact that in this case there is an advantage under Union law, since – as is also not disputed – the underlying case falls within the scope of the Parent-Subsidiary Directive.

The T-Danmark judgment also concerns the exemption from dividend tax at source under the Parent-Subsidiary Directive. For the purposes of proof of abuse, the Court distinguishes between an objective element (contrary to the purpose of the scheme) and a subjective element (the intention to artificially obtain an advantage under Union law). Whether these components are present is to be be assessed on the basis of an examination of all the facts (considerations 97-98). The CJE gave the following guideline in this respect:

“A group of companies may be regarded as being an artificial arrangement where it is not set up for reasons that reflect economic reality, its structure is purely one of form and its principal objective or one of its principal objectives is to obtain a tax advantage running counter to the aim or purpose of the applicable tax law. That is so inter alia where, on account of a conduit entity interposed in the structure of the group between the company that pays dividends and the company in the group which is their beneficial owner, payment of tax on the dividends is avoided.” (consideration 100 of the judgment in the T-Danmark case)

The CJEU furthermore gives several indications for the presence of abuse and when doing so the CJEU does not explicitly distinguish between the objective and subjective component (considerations 101-106). In this context, the CJEU also names elements to determine whether an entity constitutes a conduit company as referred to by the CJEU (consideration 104; hereinafter: 'conduit company'). The CJEU furthermore names contra-indications (considerations 110). Furthermore the CJEU elaborates on the burden of proof (considerations 115-117).

The inspector – on whom the burden of proof rests in this regard – argues that C. S.à.r.l. was only interposed by C LP in order to avoid the liability of Dutch dividend withholding tax. In his opinion so that C. S.à.r.l. can therefore not be regarded as the beneficial owner of the amounts received from A BV.

The court is of the opinion that the inspector succeeded in fulfilling the burden of proof that is resting on him in the light of the indications as given in the T-Danmark judgment for determining whether there has been abuse. In this respect the court takes the following into account:

Because of its place of residence and because of its legal form C LP is not an entity that can claim the benefits of the Parent-Subsidiary Directive.

A withholding tax of 15 percent would be due in the Netherlands over a dividend payment from A BV to C LP. This argument was brought forward and substantiated by the tax inspector and not disputed by the taxpayer. It was also stated in the e-mail message of February 3, 2015 that Person 11 sent to Person 10.

When it became known that A BV would be distributing a dividend, in a shirt timeframe C LP set up the establishment of C. S.à.r.l. and transferred its shares in A BV to C. S.à.r.l. As such, this 'timing' is also an indication of abuse.6

The tax inspector argued and the taxpayer disputed with insufficient motivation that C. S.à.r.l. issued letter shares and PECs because in Luxembourg no withholding tax is due on the redemption of letter shares and the redemption of PECs. Thus, by including C. S.à.r.l. in the structure a situation has arisen in which – when only the formal conditions are taken into consideration – the dividend income from A BV could reach C LP without Dutch or Luxembourg withholding tax having to be withheld. While without C. S.à.r.l. 15% Dutch dividend withholding tax would be due. This is not only an indication of the presence of the subjective component of abuse. The latter also implies that a contra-indication for abuse is absent. Furthermore, the circumstances under which A BV was transferred, in particular the issuance of the letter shares and PECs, are also indications that there is an artificial construction in which C. S.à.r.l. functions as a 'conduit company'.

99.84% of the total of dividends 1, 2 and payment 3 have been paid on from C. S.à.r.l. to C LP as interest payments on the PECS, the repayment of the PECS and a (re-)purchase of the letter shares issued earlier by C. S.à.r.l. The tax inspector has stated that no Luxembourg withholding tax was withheld over these payments. The taxpayer disputed this, but did not substantiate its plea. The court however considers the aforementioned percentage a confirmation that no Luxembourg withholding tax has been withheld.

The height of the aforementioned percentage also indicates that C. S.à.r.l. acted as a 'conduit company' that facilitated cash flows from A BV to the ultimate beneficial owner of the distributed amounts. That C. S.à.r.l. is a “conduit company” is also confirmed by the following. The only activities that C. S.à.r.l. has developed during its existence are the holding of shares in A BV, receiving amounts from A BV and passing these amounts on to C LP. An actual economic activity was never deployed by C. S.à.r.l. This is also supported by the nature of the costs incurred by C. S.à.r.l. and the absence of any employees apart from directors.

Two of the four board members of C. S.à.r.l. were employed by C. S.à.r.l. and also worked in the field of tax law. In its conclusion of reply, the taxpayer notes that it is possible that not all the costs of these directors and of two accountants and two lawyers, who were employed by C LP, were charged on to C. S.à.r.l. However, this has not been substantiated further. Moreover, these alleged costs do not indicate the existence of an actual economic activity.

C. S.à.r.l. was first registered at the address of a trust office and later in a multi-tenant building.

Only € 184,349 of the amounts C. S.à.r.l. received from A BV was not passed on to C LP. This amount C. S.à.r.l. needed to pay its relatively small costs, amounting to a total of € 176,547 for the years 2015 through 2017.

After the ties with A BV were severed and C. S.à.r.l. had made the aforementioned payments to C LP, C LP proceeded to liquidate C. S.à.r.l. This again supports that C. S.à.r.l. had no other role than to hold the shares in A BV and to act as a 'conduit company'.

Finally, the speed with which C. S.à.r.l. has almost fully passed the amounts it received on to C LP. Dividend 2 was passed on within six months and payment 3 was passed on within one month. The passing on of dividend 1 took a little longer, but that is because the amount received was kept to pay costs. The funds have not been used for any economic activity.

The court recognizes that not all facts and circumstances that have been taken into account above were already known at the time that dividend 1 was distributed. However, that is no reason to rule differently regarding dividend 1. Weighty with respect to dividend 1 is that this dividend payment was the immediate cause for the establishment of C. S.à.r.l. and to have C. S.à.r.l. hold the shares in A BV, while the ultimate interest in ABV did not change and nothing has been submitted which objectively shows that at the time of the restructuring another motive other than a tax motive existed for the restructuring. All this indicates prima facie the presence of both the objective and the subjective elements of abuse of Union law. It has subsequently not become apparent that the restructuring had any real economic significance, on the contrary.

The foregoing does not alter the fact that – as the taxpayer argues – C. S.à.r.l. had no contractual or legal obligation to pass the amounts it received from A BV on to C LP. In the opinion of the court, C. S.à.r.l., essentially did not have the right to use and enjoy the amounts it received from A BV. From an economic point of view as a 'conduit company' C. S.à.r.l. was not free to dispose of the amounts it received from A BV.

The taxpayer further argues that at the time of the establishment of C. S.à.r.l. it was not yet foreseeable that A BV would make a payment in 2017. Also hat doesn't change the judgment. Once it has been established that C. S.à.r.l. was a 'conduit company' and not the ultimate beneficial owner of the dividends, this applies to all distributions made to C. S.à.r.l. regardless of whether a specific distribution was already foreseeable at the time of the restructuring.

Contrary to what the interested party argues, the interposing of C. S.à.r.l. doesn’t constitute a lasting reorganization, at least not one with real economic significance. After all, C. S.à.r.l. only functioned as a 'conduit company' and was dissolved after virtually all funds received from A BV had been passed on to C LP. That C. S.à.r.l. and other shareholders of A BV owned several entities in Luxembourg, does not mean that – contrary to what the taxpayer argues – the interposing of C. S.à.r.l. had real meaning.

Finally, the argument of the taxpayer that (i) A BV had nothing to do with the alleged abuse and, in conjunction therewith, that (ii) the inspector wrongly equates A BV with C. S.à.r.l., cannot the taxpayer. For the assessment of whether the withholding exemption should be withheld because of abuse of Union law, it is only relevant whether Union law is being abused. If this is the case, it is irrelevant whether A BV was involved in the abuse nor whether A BV knew or should have known about the abuse nor whether or not A BV acted in good faith.

Taking all what has been considered above into consideration, C. S.à.r.l. was not the ultimate beneficiary of the amounts it received from A BV and the interposing of C. S.à.r.l. by C LP is to be considered as an abuse of Union law. Therefore A BV wrongly applied the withholding exemption to the distributions it made to C. S.à.r.l.

Penalties

When imposing an additional assessment the Dutch tax authorities each time also imposed a penalty amounting to € 5.278 for withholding and paying to little amounts of dividend withholding tax. (ex Article 67c of the General tax Act)

First and foremost the court states that when imposing a default penalty, no distinction is made between the degree of guilt or negligence. Only in the absence of all guilt or if there is an arguable position no fine will be imposed. An arguable position exists if the return is based on a position that is based on an arguable interpretation of the (tax) law, in the sense that at the time of filing the tax return – measured by objective standards – the taxpayer could and should reasonably believe that this explanation and thus the tax return filed by him are correct. To the opinion of the court at the time of making the present dividend payments – this also applies to dividend 1 – the interested party could reasonably believe, taking into account the state of the development of the law, measured by objective standards, that no dividend withholding tax had to be withheld over the dividend distributions to C. S.à.r.l. The court takes into account that according to the main rule applying the withholding exemption was correct, that – as the Inspector has also acknowledged – this is no 'classic' form of dividend stripping, that the concept of 'ultimately beneficiary' is not a well-defined concept, that the T-Danmark judgment had not yet been delivered and that it cannot be said – partly in view of A-G Kokott's conclusion prior to the T-Danmark judgment – that the it was not obvious what the anti-abuse principle regarding Union law meant for a case like the underlying one. The default penalties will therefore be annulled.

Other matters disputed

Did the Dutch tax authorities impose the additional assessments to right entity?

The taxpayer argues that based on Article 20, Paragraph 2 of the Dutch General State Taxes Act, the Dutch tax authorities should not have imposed the additional assessments to the successor of A BV but to the successor of C. S.à.r.l. The court sets the arguments brought forward by the taxpayer aside and comes to the conclusion that in the underlying case the main rule applies, which is that additional assessments have to imposed to the party that had to withhold the (dividend) withholding taxes. According to the court the exception to the main rule as laid down in Article 20, Paragraph 2 of the Dutch General State Taxes Act does not apply in the underlying case. Therefore, according to the court the additional assessments had to be imposed to (the successor of) A BV.

Is payment 3 a dividend distribution as meant in the Dutch-Luxembourg DTA?

The taxpayer argues that payment 3 does not constitute a dividend distribution as meant in the Dutch-Luxembourg DTA. According to the taxpayer payment 3 is a payment that is paid in respect of the repurchase of the outstanding letter shares. Therefore according to the taxpayer the Dutch tax authorities had no right to levy taxes over this payment. The court sets the argument brought forward by the taxpayer aside based on the wordings used in the Shareholders’ Resolution and the Board Resolution. The court a.o. points out that the Shareholders’ Resolution states that payment 3 is made from the freely distributable reserves. Furthermore the court points out that the Shareholders’ Resolution makes a clear distinction between on oneside the Distribution and on the otherside the Cancellation of shares against a Repayment. Therefore the court concludes that payment 3 is a dividend distribution as meant in the Dutch-Luxembourg DTA. Subsequently according to the court the Netherland was entitled to levy Dutch dividend withholding tax over payment 3.

Violation of the general principles of good governance

The taxpayer argues that the tax inspector violated the general principles of good governance, especially the principle of due care. The court concludes that the taxpayer did not substantiate its position. When discussing this matter, the court makes an interesting remark, perhaps not tax technically interesting, but still interesting: “The fact in an e-mail message to a colleague the tax inspector calls it a salient detail when he notes that C LP was involved as a co-shareholder in the the T-Danmark case, does not mean that the inspector is biased or was biased.”

The amounts for which additional assessments were imposed

The taxpayer argues that until September 30, 2014 a structure was in place in which, a.o. because of the ATR (Advance Tax Ruling), no Dutch dividend withholding tax was due over dividend distributions from A BV to C LP. According to the taxpayer therefore a compartmentalisation should be made whereby only the increase in value of the shares A BV in the period from September 30, 2014 to March 2, 2015 (the date on which C LP contributed its shares in A BV into C. S.à. r.l. should be taxed. The court sets this argument simply aside by stating that a dividend withholding tax is tax that is raised based solely based on the facts as they are at the date of the distribution. According to the court therefore there is no room for compartmentalization.

The taxpayer also argues that since the purchase price that C. S.à.r.l. paid to C LP when it obtained the shares A BV on May March 2, 2015 amounted to € 50.014.883, therefore the maximum amount of dividend that was ‘stripped’ cannot exceed the amount of € 50.014.883. According to the court this argument already fails because it assumes that the withholding exemption is refused because of the dividend stripping provisions. However, the exemption is refused on the grounds of abuse of Union law because of the artificial nature of the structure.

Those who would like to read the whole text of the judgment as made available on the website of the Dutch courts can the find the text here. (only available in the Dutch language)

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)