On September 22, 2022 on the website of the Court of Justice of the European Union (CJEU) the judgment of the Court of Justice of the European Union (the CJEU) in Case C-538/20, Finanzamt B versus W AG with the as intervener the Bundesministerium der Finanzen, ECLI:EU:C:2022:717, was published.

Introduction

This request for a preliminary ruling concerns Articles 49 and 54 TFEU.

The request has been made in proceedings between Finanzamt B (Tax Office B, Germany) and W AG, a public limited company established in Germany, concerning the refusal of Tax Office B to take into account, for the calculation of the tax payable by that company in that Member State for the year 2007, the losses incurred by that company’s permanent establishment that was situated in the United Kingdom and closed during that year.

The dispute in the main proceedings and the questions referred for a preliminary ruling

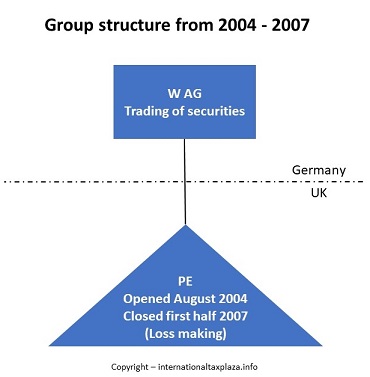

7 W, a public limited company whose registered office and place of management are in Germany, operates a securities trading bank. In August 2004, W opened a branch in the United Kingdom. As that branch did not make a profit, W closed it during the first half of 2007, so that the losses incurred by that establishment could not be carried forward in the United Kingdom for tax purposes.

8 Since Tax Office B refused to take account of those losses when determining the amount owed by W in Germany by way of corporation tax and business tax for the 2007 tax year, that company brought an action before the Hessiches Finanzgericht (Finance Court, Hesse, Germany). By judgment of 4 September 2018, that court upheld that action

9 Tax Office B brought an appeal on a point of law against that judgment before the Bundesfinanzhof (Federal Finance Court, Germany), the referring court.

10 That court notes that, although W is liable in Germany to corporation tax on its entire income, in accordance with Paragraph 1(1) and (2) of the KStG, the losses incurred by its permanent establishment in the United Kingdom are excluded from the basis of assessment of its corporation tax under Article XVIII(2) of the DBA, which exempts foreign profits from corporation tax. It observes that the same applies to business tax, since the provisions of the Gewerbesteuergesetz (Law on local business tax) refer to the determination of profits subject to corporation tax for the purposes of calculating that tax. Those factors should lead to the appeal being upheld.

11 However, the referring court is unsure whether the losses incurred by W’s permanent establishment in the United Kingdom should not be taken into account for the calculation of the tax payable by that company in Germany under freedom of establishment. According to the referring court, the Court’s case-law, resulting most recently from the judgment of 12 June 2018, Bevola and Jens W. Trock (C‑650/16, EU:C:2018:424), does not provide a clear answer to that question in the particular case where the exemption of foreign profit is provided for by a double taxation convention. If that question is answered in the affirmative, it also asks in what circumstances losses incurred by the foreign permanent establishment must be regarded as ‘final’, within the meaning of that case-law, how the amount of those losses is to be determined and whether the obligation to take them into account also applies to business tax.

12 In those circumstances the Bundesfinanzhof (Federal Finance Court) decided to stay the proceedings and to refer the following questions to the Court of Justice for a preliminary ruling:

‘(1) Is Article 43, in conjunction with Article 48 [EC] (now Article 49, in conjunction with Article 54 [TFEU]) to be interpreted as precluding legislation of a Member State which prevents a resident company from deducting losses incurred by a permanent establishment in another Member State from its taxable profits where, first, the company has exhausted the possibilities to deduct those losses available under the law of the Member State in which the permanent establishment is situated and, second, it has ceased to receive any income through that permanent establishment, so that there is no longer any possibility of account being taken of the losses in that Member State (“final” losses), including if the legislation in question concerns an exemption for profits and losses under a bilateral convention for the avoidance of double taxation between the two Member States?

(2) If the first question is answered in the affirmative: is Article 43, in conjunction with Article 48 [EC] (now Article 49, in conjunction with Article 54 [TFEU]) to be interpreted as also precluding the provisions of the Law on local business tax which prevent a resident company from deducting from its taxable business earnings “final” losses, of the type referred to in the first question, of a permanent establishment situated in another Member State?

(3) If the first question is answered in the affirmative: in the event of the closure of the permanent establishment in the other Member State, can there be “final” losses of the type referred to in the first question, even though there is at least a theoretical possibility that the company might once more open in the Member State concerned a permanent establishment, any profits of which could be offset against the previous losses?

(4) If the first and third questions are answered in the affirmative: can the losses of the permanent establishment which, under the law of the State in which that establishment is situated, could have been carried forward to a subsequent tax period on at least one occasion also be considered to be “final” losses of the type referred to in the first question, of which account is to be taken by the State in which the parent establishment is resident?

(5) If the first and third questions are to be answered in the affirmative: is the obligation to take account of cross-border “final” losses limited as to amount by the amount of losses which the company could have calculated in the State in which the permanent establishment is situated, were the taking account of losses not precluded there?’

Judgment

The Court (Fourth Chamber) hereby rules:

Articles 49 and 54 TFEU must be interpreted as not precluding a tax system of a Member State under which a company resident in that Member State may not deduct from its taxable profits the final losses incurred by its permanent establishment situated in another Member State where the Member State of residence has waived its power to tax the profits of that permanent establishment under a double taxation convention.

Legal context

German law

3 Paragraph 1 of the Körperschaftsteuergesetz (Law on corporation tax), in the version applicable to the dispute in the main proceedings (‘the KStG’), provides:

‘(1) The following legal persons, associations of persons and pools of assets which have their management or their registered office on national territory shall have unlimited liability to corporation tax:

1. capital companies (in particular European companies, public limited liability companies, limited liability companies and limited partnerships);

…

2. The unlimited obligation to pay corporation tax applies to all income.

…’

4 Paragraph 8(2) of the KStG stipulates that all the income of a taxpayer with unlimited tax liability within the meaning of points 1 to 3 of Paragraph 1(1) is to be regarded as arising from industrial or commercial activity.

The Double Taxation Convention

5 Article III(1) of the Convention of 26 November 1964 between the Federal Republic of Germany and the United Kingdom of Great Britain and Northern Ireland for the avoidance of double taxation and the prevention of fiscal evasion, as amended by an addendum of 23 March 1970 (BGBl. 1966 II, p. 359; BGBl. 1967 II, p. 828; and BGBl. 1971 II, p. 46) (‘the DBA’) states:

‘The industrial or commercial profits of an undertaking of one of the territories shall be subject to tax only in that territory unless the undertaking carries on an industrial or commercial activity in the other territory through a permanent establishment situated there. If the undertaking carries on an industrial or commercial activity in the other territory through a permanent establishment, the profits shall be taxable in the other territory, but only in so far as they are attributable to that permanent establishment.’

6 Article XVIII(2) of the DBA provides:

‘The tax shall be levied as follows for persons resident in the Federal Republic of Germany:

(a) source income and assets situated in the United Kingdom which are taxable in the United Kingdom under the present convention shall be excluded from taxation in the Federal Republic of Germany …; profits referred to in Article VIII(1) shall, however, be excluded only if they are subject to tax in the United Kingdom. The Federal Republic nevertheless retains the right to take into account, for the purposes of the determination of the rate of tax, the items of income or assets excluded from the tax base.

…’

From the considerations of the Court

The first question

13 By its first question, the referring court asks the Court, in essence, whether Articles 49 and 54 TFEU must be interpreted as precluding a tax system of a Member State under which a company resident in that Member State may not deduct from its taxable profits the final losses incurred by its permanent establishment situated in another Member State where the Member State of residence has waived its power to tax the profits of that permanent establishment under a double taxation convention.

14 According to the Court’s settled case-law, the freedom of establishment guaranteed by Articles 49 and 54 TFEU includes, for companies or firms formed in accordance with the law of a Member State and having their registered office, central administration or principal place of business within the European Union, the right to exercise their activity in other Member States through a subsidiary, branch or agency (judgment of 12 June 2018, Bevola and Jens W. Trock, C‑650/16, EU:C:2018:424, paragraph 15).

15 Even though, according to their wording, the provisions of EU law on freedom of establishment are aimed at ensuring that foreign nationals are treated in the host Member State in the same way as nationals of that State, they also prohibit the Member State of origin from hindering the establishment in another Member State of one of its nationals or of a company incorporated under its legislation. Those considerations are also valid where, as in the present case, a company established in one Member State carries on business in another Member State through a permanent establishment (see, to that effect, judgment of 12 June 2018, Bevola and Jens W. Trock, C‑650/16, EU:C:2018:424, paragraphs 16 and 17 and the case-law cited).

16 In the present case, it is apparent from the request for a preliminary ruling that, under Paragraph 1(1) and (2) of the KStG, companies which have their place of management or registered office in Germany are subject to corporation tax on all their income. However, in accordance with the provisions of the DBA, where a company which has its place of management or registered office in Germany carries on an industrial or commercial activity in the United Kingdom through a permanent establishment, the profits attributable to that permanent establishment are excluded from the basis of assessment for corporation tax payable by that company in Germany, without prejudice to the possibility for that Member State to take those profits into account when calculating the rate of taxation, provided that they are subject to tax in the United Kingdom. The same applies, symmetrically, to losses attributable to such a permanent establishment.

17 In such a situation, resident companies enjoy, for the purpose of determining their taxable income, a tax advantage which consists of allowing them to take into account the losses incurred by a resident permanent establishment. To exclude that possibility in respect of the losses incurred by a permanent establishment situated in another Member State creates a difference in treatment which could discourage a resident company from carrying on its business through such a permanent establishment (see, to that effect, judgment of 12 June 2018, Bevola and Jens W. Trock, C‑650/16, EU:C:2018:424, paragraphs 18 and 19 and the case-law cited).

18 Such a difference in treatment is permissible only if it concerns situations which are not objectively comparable, or if it is justified by an overriding reason in the public interest proportionate to that objective (see, to that effect, judgment of 12 June 2018, Bevola and Jens W. Trock, C‑650/16, EU:C:2018:424, paragraph 20 and the case-law cited).

19 It follows from the Court’s case-law that the comparability of an internal situation with a cross-border situation must be examined having regard to the aim pursued by the national provisions at issue (judgment of 12 June 2018, Bevola and Jens W. Trock, C‑650/16, EU:C:2018:424, paragraph 32 and the case-law cited).

20 As regards measures laid down by a Member State in order to prevent or mitigate the double taxation of a resident company’s profits, companies which have a permanent establishment in another Member State are not, in principle, in a comparable situation to that of companies possessing a resident permanent establishment (see, to that effect, judgment of 12 June 2018, Bevola and Jens W. Trock, C‑650/16, EU:C:2018:424, paragraph 37 and the case-law cited).

21 The situation is different where national tax legislation itself treats those two categories of establishment in the same way for the purposes of taking into account the losses and profits made by them (see, to that effect, judgments of 17 July 2014, Nordea Bank Danmark, C‑48/13, EU:C:2014:2087, paragraph 24, and of 17 December 2015, Timac Agro Deutschland, C‑388/14, EU:C:2015:829, paragraph 28).

22 However, where the Member State in which a company is resident has waived, pursuant to a double taxation convention, the exercise of its power to tax the profits of the non-resident permanent establishment of that company, situated in another Member State, the situation of a resident company possessing such a permanent establishment is not comparable to that of a resident company possessing a resident permanent establishment in the light of the measures taken by the first Member State in order to prevent or mitigate the double taxation of profits and, symmetrically, the double deduction of resident companies’ losses (see, to that effect, judgments of 17 December 2015, Timac Agro Deutschland, C‑388/14, EU:C:2015:829, paragraph 65).

23 The judgment of 12 June 2018, Bevola and Jens W. Trock (C‑650/16, EU:C:2018:424), to which the referring court refers, did not call that conclusion into question.

24 It is true that, in that judgment, the Court held, as regards losses attributable to a non-resident permanent establishment which had ceased activity and whose losses could not, and no longer could have been deducted from its taxable profits in the Member State in which it carried on its activity, that the situation of a resident company possessing such an establishment did not differ from that of a resident company possessing a resident permanent establishment, from the point of view of the objective of preventing double deduction of the losses. It added that the ability to pay tax of a company possessing a non-resident permanent establishment which has definitively incurred losses is affected in the same way as that of a company whose resident permanent establishment has incurred losses, with the result that the two situations are comparable in that regard (judgment of 12 June 2018, Bevola and Jens W. Trock, C‑650/16, EU:C:2018:424, paragraphs 38 and 39).

25 However, in that case, the Member State of residence of the company which requested that the final losses incurred by its non-resident permanent establishment be taken into account had not, by means of a double taxation convention, waived its power to tax that establishment’s profits. It had decided unilaterally, except in the event of the option, by the company in question, for an international joint taxation scheme, not to take into account the profits made and losses incurred by non-resident permanent establishments of resident companies, even though that Member State would have been competent to do so, which is different.

26 In the present case, it is apparent from the request for a preliminary ruling that, under the DBA, the Federal Republic of Germany waived its power to tax profits made by permanent establishments situated in the United Kingdom through which their resident companies carry on industrial or commercial activities. The same applies, symmetrically, to the taking into account of losses recorded by those establishments.

27 Since, under a double taxation convention, the Federal Republic of Germany has waived its power to tax the profits made and losses incurred by such a permanent establishment situated in another Member State, a resident company which has such an establishment is not in a situation comparable to that of a resident company which has a permanent establishment situated in Germany in the light of the objective of preventing or mitigating the double taxation of profits and, symmetrically, the double taking into account of losses.

28 Consequently, in a situation such as that at issue in the main proceedings, no restriction on the freedom of establishment guaranteed by Articles 49 and 54 TFEU can be established.

29 In the light of the foregoing considerations, the answer to the first question is that Articles 49 and 54 TFEU must be interpreted as not precluding a tax system of a Member State under which a company resident in that Member State may not deduct from its taxable profits the final losses incurred by its permanent establishment situated in another Member State where the Member State of residence has waived its power to tax the profits of that permanent establishment under a double taxation convention.

The second to fifth questions

30 In view of the answer given to the first question, there is no need to answer the second to fifth questions.

Costs

31 Since these proceedings are, for the parties to the main proceedings, a step in the action pending before the national court, the decision on costs is a matter for that court. Costs incurred in submitting observations to the Court, other than the costs of those parties, are not recoverable.

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)