On November 17, 2023 on the website of the Dutch courts the judgment of the Dutch Supreme Court in case 21/05123, ECLI:NL:HR:2023:1579 was published. In the underlying case the Dutch Supreme Court ruled on several issues. One of them being the question whether a currency exchange gain that is realized over the purchase price that was due with respect to the purchase of a participation qualifies as a tax-exempt result of an earn-out payment. To be honest we don’t understand how the taxpayer thought he could be successful in his appeal with the position he took with respect on this matter.

The Dutch Supreme Court furthermore ruled on how the loss compensation rules work in case a pure holding and group financing entity with pre-merger losses (legally) merges with an operating entity.

Facts

2.1 Until the legal merger as referred to in 2.6 below, the activities of the taxpayer exclusively consisted of holding and financing activities.

2.2 As of the financial year 2014 the taxpayer calculates its taxable income for Dutch corporate income tax purposes in US dollars (USD).

2.3 As per January 1, 2014, the taxpayer had an amount exceeding USD 68 mio of holding and financing losses available that could be carried forward within the meaning of Article 20, Paragraph 4 of the Dutch corporate income tax Act (text as it read until 2019; hereinafter: the DCIT Act).

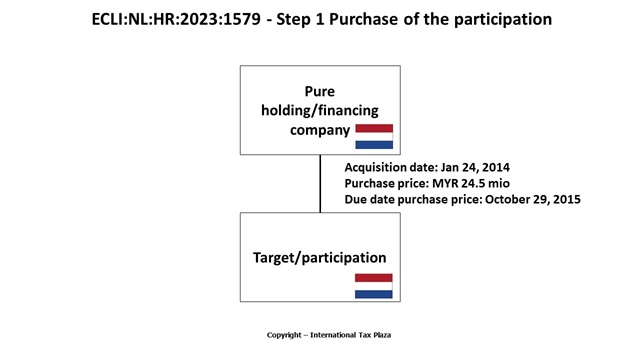

2.4 On January 24, 2014 the taxpayer acquired all shares in a group company residing in the Netherlands (hereinafter: the subsidiary). The purchase price for these shares was agreed upon in Malaysian ringgit (MYR) and amounted to MYR 24,493,878 (hereinafter: the purchase price). The subsidiary was mainly involved in the trade and marketing of lubricating oils and as per January 1, 2014 the subsidiary had no losses available that could be carried forward.

2.5 On October 29, 2015 the taxpayer paid the purchase price. Because of a change in the MYR/USD exchange rate the taxpayer realized a currency exchange gain (hereinafter: the currency exchange rate).

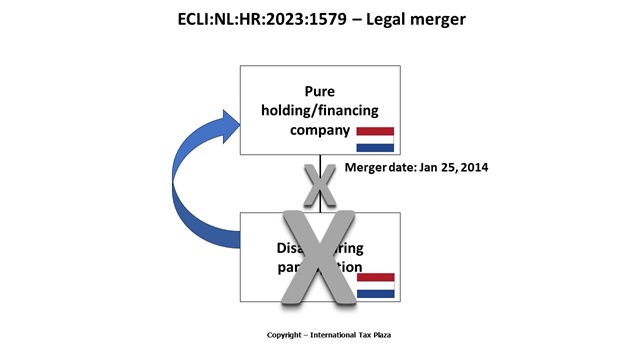

2.6 On January 25, 2014 the taxpayer and the (newly obtained subsidiary) legally merged. In this merger the taxpayer was the acquiring legal entity and the subsidiary was the disappearing legal entity.

2.7 The tax inspector has issued a decree as referred to in Article 14b, Paragraph 3, last sentence of the DCIT Act with respect to the taxpayer and the subsidiary. In that decree, the tax inspector stated that, subject to the conditions set out in the Decree of the Secretary of State for Finance of July 8, 1998 (hereinafter: the Decree), he would not levy Dutch corporate income tax over the profit realized as a result of the transfer under universal title of the assets of the disappearing entity. The merger date is set at January 1, 2014 (hereinafter: the merger date).

2.8 Amongst others the following conditions are included in the Decree:

“Settlement of losses, foreign results and withholding tax

2. For the application of Article 20 of the DCIT Act with respect to losses incurred before the time of the merger, settlement will take place under the following conditions:

Profit split

2a. Each year the profit of the acquiring legal entity is split into parts that relate to the enterprises that were operated by each of the merging legal entities before the merger (hereinafter: profit split).

This profit split takes place as if the merger did not taken place, whereby a profit can only be attributed to the enterprise of a merging legal entity to the extent that it is expressed as such by the acquiring legal entity.”

and

“Vertical settlement of losses

2d. The pre-merger losses the acquiring legal entity will only be settled with the part of the profit of the acquiring legal entity as determined in accordance with parts (a) and (b) that relates to the enterprise as operated by the acquiring legal entity before the time of the merger, except to the extent that the settlement of these losses is limited on other grounds.”

2.9 As a result of the legal merger with the subsidiary, the actual activities of the taxpayer in the underlying year (2015) did no longer consisted entirely or almost intirely out of the holding of subsidiaries or the directly or indirectly financing of its affiliated bodies as referred to in Article 20, Paragraph 4 of the DCIT Act.

Judgment of the District Court of the Hague

3.1.1 The first dispute before the District Court the Hague was whether pursuant to Article 13, Paragraph 6 of the DCIT Act the currency exchange gain is to be regarded as an exempt benefit from a participation.

3.1.2 The Court ruled that Article 13, Paragraph 6 of the DCIT Act does not apply to foreign exchange gains. The participation was not acquired for a price referred to in Article 13, Paragraph 6 of the DCIT Act. Meaning a price consisting wholly or partly out of a right to one or more installments of which the number or the size of which has not yet been determined.

3.2.1 Secondly, before the District Court the parties were disputing whether Article 20, Paragraph 4 of the DCIT Act precludes the carrying forward of pre-merger holding and financing losses suffered by the taxpayer from being settled against the currency exchange gain. The taxpayer argues that this is not the case because the legal merger must be ignored for the application of the so-called activities test included in that provision. To this end, the taxpayer relies on condition 2a cited above in 2.8 (hereinafter: condition 2a). The taxpayer also refers to the arrangement of Article 15ae, Paragraph 3 of the DCIT Act with regard to the consequences of entering into a fiscal unity for the application of Article 20, Paragraph 4 of the DCIT Act.

3.2.2 The District Court is of the opinion that the taxpayer’s legal view is incorrect where it argues that for the application of the activities test of Article 20, Paragraph 4 of the DCIT Act the legal merger must be ignored. Because the actual activities of the taxpayer in 2015 did not meet that activities test, according to the District Court the taxpayer can no longer be regarded as a holding or financing company. In view of this, the taxpayer cannot settle holding and financing losses from previous financial years with profits the taxpayer realized in 2015. According to the District Court condition 2a does not change this.

Judgment of the Dutch Supreme Court

After the judgment of the District Court of November 4, 2021 parties did not go to a Court of Appeal but immediately started a cassation procedure.

In its first plea the taxpayer disputes the ruling of the District Court of the Hague (as referred to above under 3.1.2) that Article 13, Paragraph 6 of the DCIT Act does not apply to the currency exchange gain.

In its judgment the Dutch Supreme Court confirms the judgment of the District Court of the Hague that Article 13, Paragraph 6 of the DCIT Act does not apply to the currency exchange gain. In our remarks below we will elaborate a bit more on this.

In its second plea the taxpayer disputes that the ruling of the District Court of the Hague (as referred to above under 3.2.2) that based on Article 20, Paragraph 4 of the DCIT Act the pre-merger losses of the taxpayer cannot be settled with its taxable profit of the financial year 2015.

In its judgment the Dutch Supreme Court confirms the previous ruling of the District Court that based on Article 20, Paragraph 4 of the DCIT Act the pre-merger losses of the taxpayer cannot be settled with its taxable profit of the financial year 2015. In our remarks below we will elaborate a bit more on this.

Remarks by ITP

An earn-out for Dutch corporate income tax purposes

First of all it should be noted that in the underlying case the taxpayer has opted to use the US dollar as functional currency to calculate its taxable profits instead of using the euro.

Article 13 of the DCIT Act contains the basic provisions regarding the Dutch participation exemption. Article 13, Paragraph 6 of the DCIT Act reads as follows:

“If a subsidiary or part thereof has been alienated or acquired for a price which wholly or in part consists of a right to one or more installments of which the number or size of which has not yet been determined in the financial year of the alienation or acquisition, the changes in value of that right, and for the acquirer the changes in value of the obligation corresponding to that right constitute benefits stemming from the participation.(…).”

Article 13, Paragraph 6 of the DCIT Act applies to so-called earn-out payments. These are situations in which the total amount of the consideration for the acquisition or disposal of a shareholding is uncertain at the moment of the transaction because the total consideration wholly or in part consists of a right to one or more installments of the number or size of which has not yet been determined at the time of that acquisition or alienation.

In our view, that now seems to have been confirmed by the Dutch Supreme Court, in case the consideration to be paid/received for the participation is denominated in another currency than the currency in which the taxpayer calculates its taxable profits at should be assessed at the time of the transfer of the shares whether the total amount of that consideration is uncertain in the currency in which the consideration is denominated (in the underlying case in Malaysian ringgit).

Since in the underlying case the purchase price was a specific amount of Malaysian ringgit that was due on a later date, the purchase price does not constitute a so-called earn-out payment. Yes in US dollars the value of the purchase price might change but in Malaysian ringgit it dis not change. On January 24, 2014 the taxpayer should have included the newly obtained participation in its books for the US Dollar equivalent of MYR 24,493,878 and for the same amount it should include a payment liability. The Dutch participation exemption does not apply to later changes of this liability. Therefore currency exchange results will lead to a taxable profit/ deductible loss depending on how the MYR/USD exchange rate will change.

In case the total consideration partly consists out of a payment term of which the size is uncertain (eg a payment term that is based on a future EBITA of the participation) the Dutch participation exemption would apply to a change is the size of this payment term. In that case the taxpayer would have to access to which amount it reasonably expects this payment term to amount. The payment liability is than to be include in the taxpayer’s balance sheet. The Dutch participation exemption then applies to a later change in value of this payment liability that for as far as this change in value is caused by the fact that the EBITA of the purchased entity is either higher or lower than expected at the time of the acquisition. At the same time the historic cost-price of the participation is to be adjusted for the same amount (an earn-out gain leads to a lower historic cost-price of the participation and an earn-out loss leads to a higher historic cost-price of the participation). It should however be noted that in case the purchase price is also denominated in a foreign currency (not being the functional) currency, the difference between the original purchase price and the amount actually being paid should be split in the difference that is caused by the change of the purchase price to be paid in the foreign currency (to which the participation exemption applies) and the part of the difference that is caused by a change in exchange rate (to which the participation exemption does not apply). The aforementioned obviously applies to both the buyer and the seller.

Settlement of the pre-merger losses

In the underlying court case the taxpayer wished to settle its pre-merger losses with the post-merger profits.

Since the actual pre-merger activities of the taxpayer entirely or almost entirely consisted out of holding and (group-)financing activities. The pre-merger losses therefore qualify as holding and financing losses as meant in Article 20, Paragraph 4 of the DCIT Act as it was in place until January 1, 2019.

(NB As of January 1, 2019 the provision as was laid-down in the DCIT Act is no longer included in the DCIT Act. Since the rules however still apply to holding/financing losses that were incurred in financial years beginning before January 1, 2019 we think it is useful to shortly elaborate on the matter)

Based on Article 20, Paragraph 4, under a of the DCIT Act such holding/financing loss can only be settled with taxable profits of years in which the actual activities of the taxpayer during the entire or almost the entire year consist entirely or almost entirely out of the holding of interests in participations or the directly or indirectly financing of affiliated entities. As a result of the legal merger, the taxpayer also carried out other types of activities in 2015. Consequently the actual activities of the taxpayer during that year did not entirely or almost entirely consist out of the holding of interests in participations or the financing of affiliated entities. Without further provision, the provisions of Article 20, Paragraph 4 of the DCIT Act therefore mean that the pre-merger holding and financing losses of the taxpayer cannot be settled with its taxable profit for the year 2015.

The Dutch legislator included such a provision in Article 15ae, Paragraph 3 (old) of the DCIT Act for situations in which an entity with losses as meant in Article 20, Paragraph 4 (old) of the DCIT Act is included in a fiscal unity. The Dutch legislator however did not include a similar provision in the DCIT Act with respect to (legal) mergers. In this respect the Dutch Supreme Court notes the following:

“The second plea fails insofar as it means that without justification the Dutch legislator treats similar cases differently. A fiscal entity involves separate legal entities, so that a distinction between the activities and the profits attributable to each of those legal entities will cause fewer technical complications than a split of activities and profits within one legal entity that was created by a legal merger would. In view of the drafting history of Article 20 Paragraph 4 of the DCIT Act, it must be assumed that the legislator, partly for this reason, has chosen not to include a similar provision that would apply in the event of a change in status of the taxpayer (in this case: the losing of the status of a holding and financing company), also not if this change is the result of a legal merger. It cannot be said that this choice is clearly without reasonable grounds.

Neither can a further provision as referred above be found in condition 2a either. That condition only means that the profit of the acquiring legal entity is split with a view to the limitation of the possibility of loss settlement provided for in the Act, as regulated in condition 2d. Condition 2a does not provide for division of the actual activities of the acquiring legal entity. That condition does not provide for a settlement of losses that goes beyond what results from the application of the statutory provision, including Article 20(4) of the Act.

Since a further provision as referred to above is also not included in any other regulation, based on Article 20, Paragraph 4 of the DCIT Act the pre-merger holding and financing loss of the taxpayer cannot be settled with the taxpayer’s taxable profit of the year 2015.

The judgments of the District Court as mentioned above in 3.2.2 are therefore correct, so that the second plea of the taxpayer also fails for the rest.”

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)