On March 14, 2024 on the website of the Court of Justice of the European Union (CJEU) the opinion of Advocate General Emiliou in the Case C‑585/22, X BV versus the Dutch Staatssecretaris van Financiën, ECLI:EU:C:2024:238, was published.

Introduction

Benjamin Franklin’s renowned adage that, ‘in this world, nothing is certain except death and taxes’, captures a universal truth. However, it would often appear that a predisposed tendency of human nature is to elude those very inevitabilities.

The present request for a preliminary ruling arises in the context of provisions of national law on corporation tax, specifically designed to tackle tax avoidance practices. Under that legislation, the contracting of a loan debt by a taxable person with a related entity – for the purposes of acquiring or extending an interest in another entity – is, in certain circumstances, presumed to be an artificial arrangement, designed to erode the Netherlands tax base. Consequently, that person is precluded from deducting the interest on the debt from its taxable profits unless it can rebut that presumption.

The present request from the Hoge Raad der Nederlanden (Supreme Court of the Netherlands) invites the Court to clarify its case-law on, inter alia, the freedom of establishment laid down in Article 49 TFEU, specifically whether it is compatible with that freedom for the tax authorities of a Member State to refuse to a company belonging to a cross-border group the right to deduct from its taxable profits the interest it pays on such a loan debt. Most notably, the Court is asked to clarify its findings in its judgment in Lexel, on whether such intra-group loans may be, for that purpose, regarded as wholly artificial arrangements, even if carried out on an arm’s length basis, and the interest set at the usual market rate.

Facts, national proceedings and the questions referred

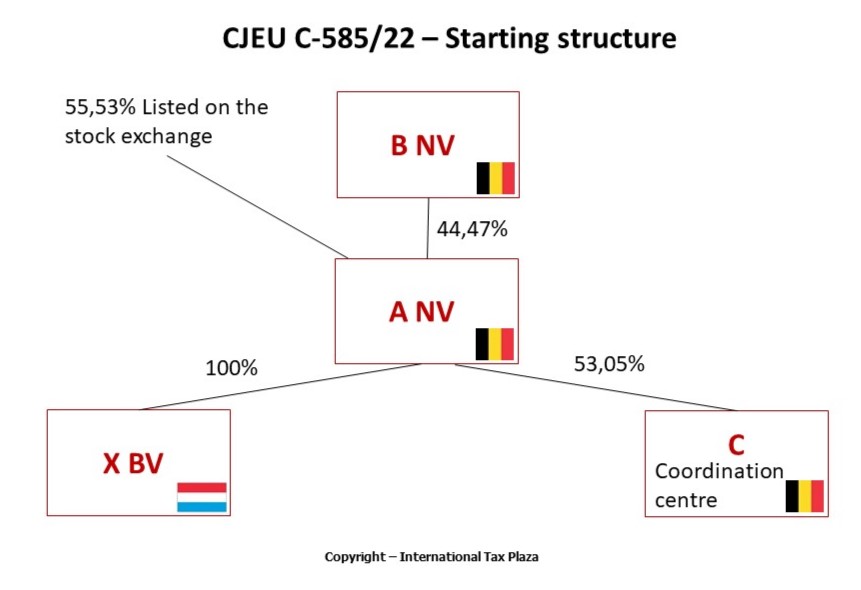

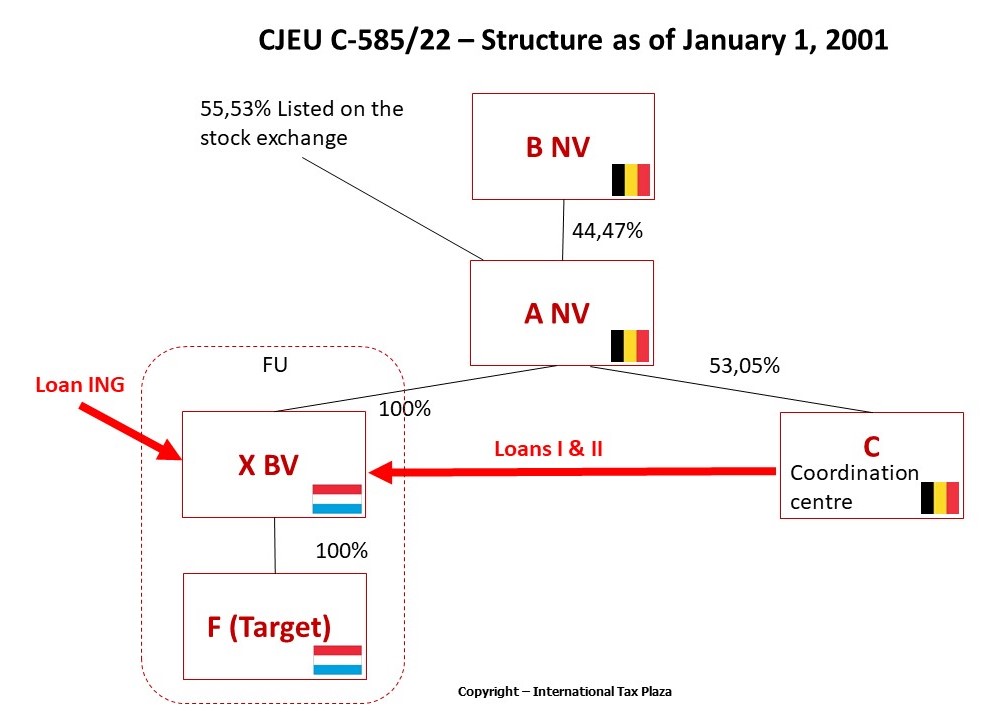

5. Company X (‘X’ or ‘the appellant’) is a holding company, incorporated under Netherlands law. It belongs to a multinational group, which includes, inter alia, Company A and Company C (respectively, ‘A’ and ‘C’).

6. A is the parent company established in Belgium. It is the sole shareholder of the appellant and the majority shareholder of C.

7. C is an internal bank, also established in Belgium. It offers intra-group services, which include financial restructuring and management. Between 1999 and 2010, it had the status of a ‘coordination centre’ (for tax purposes) under Belgian law, which meant that it benefited from a preferential tax regime under which its taxable profit was determined on a flat-rate basis.

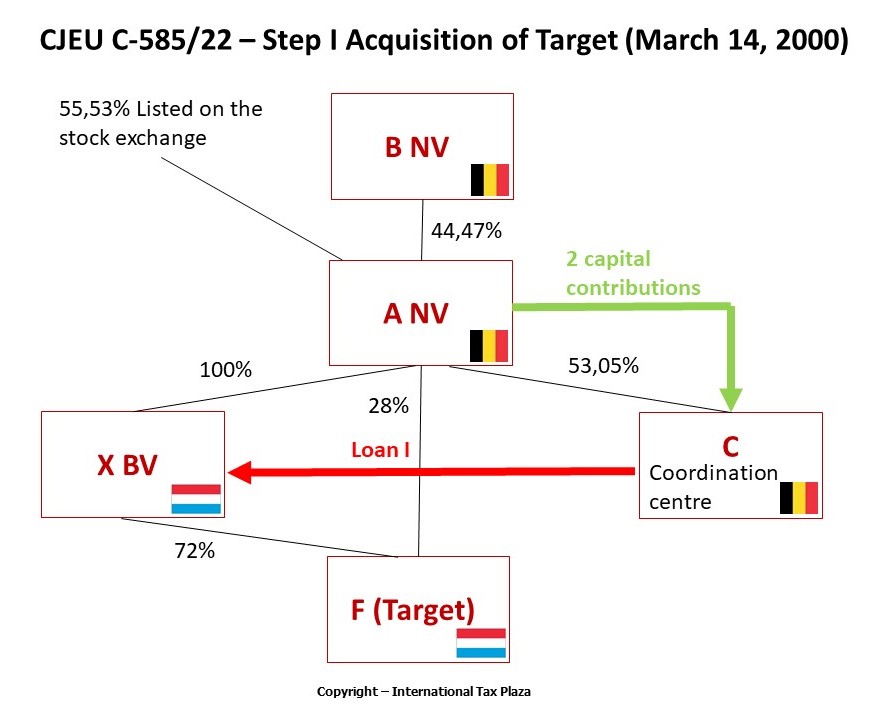

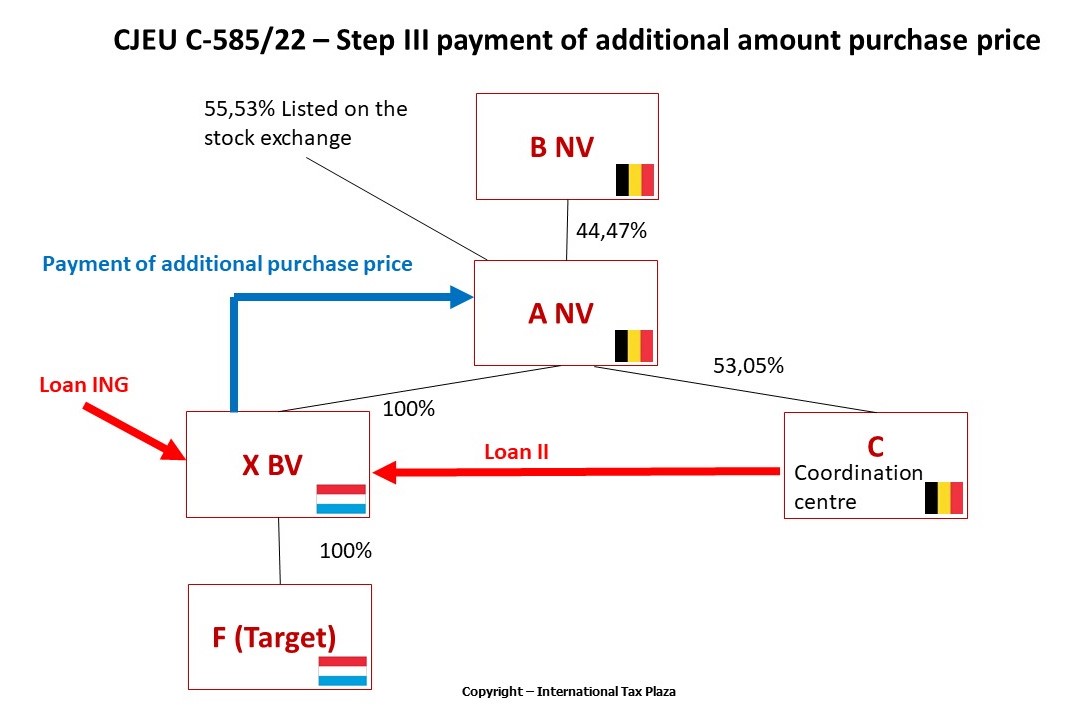

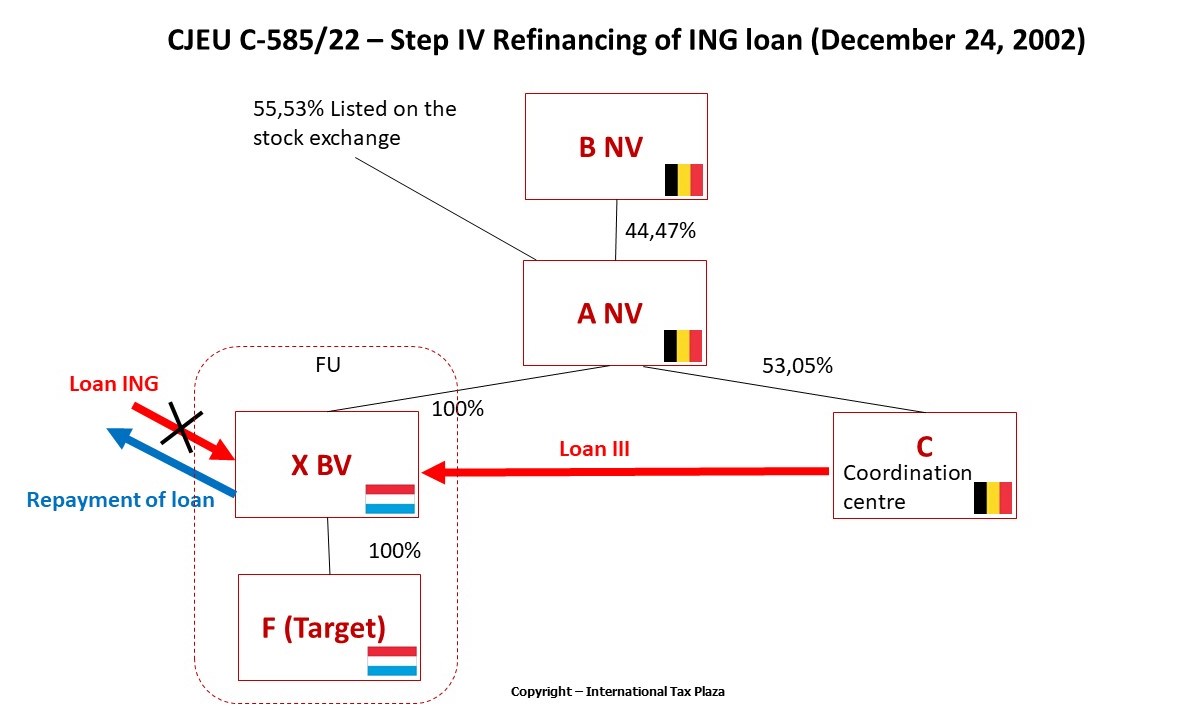

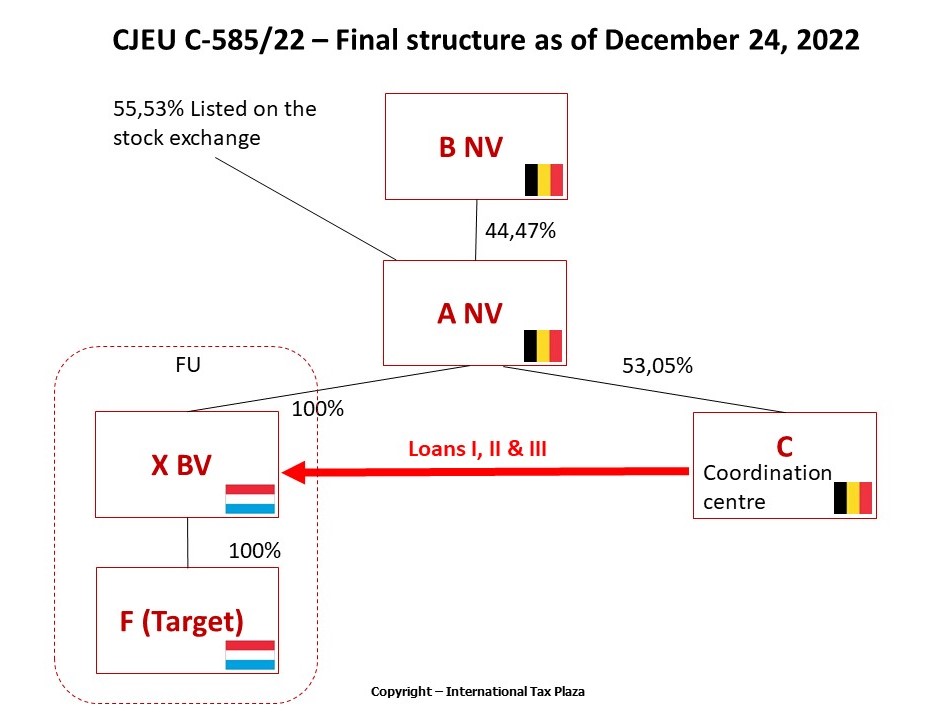

8. In 2000, X acquired the shares of Company F (‘F’), established in the Netherlands. As a result of that acquisition, F became an entity related to the appellant.

9. X financed that acquisition through loans taken out with C. The latter company granted those loans from its own funds, which it had obtained shortly before through a capital injection by A. The loans in question provided for interests set at the usual market rate.

10. As from 1 January 2001, X and F were consolidated into a tax unit, with X designated as the parent company. As such, the tax due by both F and X was levied on the latter company. X could also deduce the interest charges it paid to C from the profits generated by F. As a result of that deduction, the unit had very low corporation tax liability in the Netherlands.

11. In 2007, X deducted the interest on its loans from C in its corporation tax return. However, the Staatssecretaris van Financiën (State Secretary for Finance, Netherlands) refused that deduction on the basis of Article 10a of the Law on Corporation Tax.

12. The appellant challenged that refusal before the rechtbank Gelderland (District Court, Gelderland, Netherlands), and then before the Gerechtshof Arnhem Leeuwarden (Court of Appeal, Arnhem-Leeuwarden, Netherlands).

13. By decision of 20 October 2020, that latter court determined that that restriction on the deduction of interest was compatible with EU law. It held that the purpose of that legislation (which is to prevent the erosion of the Netherlands tax base through abusive practices, whereby artificially generated interest expenses are deducted from profits) was justified and proportionate.

14. The appellant lodged an appeal in cassation against that decision before the Hoge Raad der Nederlanden (Supreme Court of the Netherlands).

15. According to that court, in its settled case-law, debts contracted arbitrarily and without commercial justification constitute wholly artificial arrangements, intended merely to create a deductible expense, regardless of whether the interest rate is identical to that which would have been agreed between independent companies on an arm’s length basis.

16. Concurring with the findings made by the Gerechtshof Arnhem Leeuwarden (Court of Appeal, Arnhem-Leeuwarden), therefore, where such circumstances arise, the referring court takes the view that the complete refusal of interest deductions for debtors is appropriate and proportionate because such a measure aims to tackle tax avoidance by specifically targeting instances in which the debt is generated by a wholly artificial arrangement.

17. However, the referring court wonders whether, in the light of the Court’s judgment in Lexel, that position is correct.

18. Indeed, that judgment may be read in the sense that intra-group transactions, such as the contracting of debt with an entity related to the taxable person, cannot be regarded as wholly artificial arrangements if they are carried out on an arm’s length basis. If such an interpretation were correct, the referring court expresses further uncertainty as to whether the complete refusal of the right to deduct interest is compatible with the principle of proportionality under EU law.

19. Lastly, the referring court seeks clarity on whether the distinction between the national law at issue in the present case, which pertains to both internal restructuring and external acquisition, and the law at issue in the judgment in Lexel, which did not cover external acquisitions, holds any significance.

20. Against that background, the Hoge Raad der Nederlanden (Supreme Court of the Netherlands) decided to stay the proceedings and to refer the following questions to the Court of Justice for a preliminary ruling:

‘(1) Are Articles 49 TFEU, 56 TFEU and/or 63 TFEU to be interpreted as precluding national legislation under which the interest on a loan debt contracted with an entity related to the taxable person, being a debt connected with the acquisition or extension of an interest in an entity which, following that acquisition or extension, is a related entity, is not deductible when determining the profits of the taxable person because the debt concerned must be categorised as (part of) a wholly artificial arrangement, regardless of whether the debt concerned, viewed in isolation, was contracted at arm’s length?

(2) If the answer to Question 1 is in the negative, must Articles 49 TFEU, 56 TFEU and/or 63 TFEU be interpreted as precluding national legislation under which the deduction of the interest on a loan debt contracted with an entity related to the taxable person and regarded as (part of) a wholly artificial arrangement, being a debt connected with the acquisition or extension of an interest in an entity which, following that acquisition or extension, is a related entity, is disallowed in full when determining the profits of the taxable person, even where that interest in itself does not exceed the amount that would have been agreed upon between companies which are independent of one another?

(3) For the purpose of answering Questions 1 and/or 2, does it make any difference whether the relevant acquisition or extension of the interest relates (a) to an entity that was already an entity related to the taxable person prior to that acquisition or extension, or (b) to an entity that becomes an entity related to the taxpayer only after such acquisition or extension?’

21. Written observations have been submitted by the appellant, the Belgian, Spanish and Netherlands Governments, and the European Commission. The appellant, the Spanish and Netherlands Governments, as well as the Commission, presented oral argument at the hearing, which took place on 15 November 2023.

The conclusion of the Advocate General

In the light of all the foregoing considerations, Advocate General Emiliou proposes that the Court answer the questions referred by the Hoge Raad der Nederlanden (Supreme Court of the Netherlands) as follows:

Article 49 TFEU must be interpreted as meaning that it does not preclude national legislation under which the interest on a loan contracted with an entity related to the taxable person is not deductible when determining the profits of that person, where the conclusion of that loan was predominantly motivated not by commercial considerations, but by the objective of creating a deductible debt, even where the interest rate stipulated therein does not exceed that that would have been agreed upon between companies which are independent of one another. In that situation, the deduction of the interest shall be disallowed in full.

Legal framework

Article 10a of the Wet op de vennootschapsbelasting 1969 (Dutch Law on Corporate Income Tax of 1969; ‘the Law on Corporation Tax’), in the version in force at the time of the dispute in the main proceedings, provides:

‘1. When profit is being determined …, interest – including costs and currency exchange results – may not be deducted if it relates to debts which in law or in fact are directly or indirectly payable to a related entity or related natural person, in so far as the debt relates directly or indirectly, in law or in fact, to one of the following legal transactions:

…

c. the acquisition or extension by the taxable person, by an entity related to the taxable person and subject to corporate income tax or by a natural person related to the taxable person and resident in the Netherlands, of an interest in an entity that becomes an entity related to the taxable person subsequently to the acquisition or extension of that interest

…

3. Paragraph 1 shall not apply if the taxpayer can demonstrate that:

a. the loan and the associated legal transaction are predominantly based on commercial considerations; or

b. a profit tax or income tax that is reasonable in accordance with the Netherlands criteria is ultimately levied on the interest in respect of the person to whom, in law or fact, interest is directly or indirectly payable … A tax levied on profit is reasonable in accordance with the Netherlands criteria if it results in a levy at a rate of at least 10% on taxable profit determined in accordance with the Netherlands criteria …

4. For the purposes of this article …, the following shall be considered to be an entity related to the taxable person:

a. an entity in which the taxable person has an interest of at least one third;

b. an entity that has an interest of at least one third in the taxable person;

c. an entity in which a third party has an interest of at least one third, where that third party also has an interest of at least one third in the taxable person.

…’.

From the analysis of the Adviocate General

22. The referring court’s three questions originate from the rules on corporation tax in the Netherlands. Those questions concern, specifically, the following issue. Whereas, under those rules, a Netherlands-tax-resident company may, in principle, deduct from its taxable profits the interest on the debts it has contracted and, thus, reduce its tax liability, the contested provision, namely Article 10a(1)(c) of the Law on Corporation Tax, limits that possibility with respect to intra-group loans.

23. That provision applies when a loan debt is contracted by the taxable person with a related entity (that is to say, another company from the group to which that person belongs, for instance an internal bank) for the financing of an acquisition or extension of an interest in an entity that was already an entity related to the taxable person prior to such acquisition or extension (internal restructuring) or an entity that only subsequently becomes an entity related to the taxable person (external acquisition).

24. Under either scenario, the taxable person is barred from deducting the interest on such debt, even if the interest charges are equivalent to that which would have been agreed upon with an unrelated entity, such an external bank. This is because that provision establishes a presumption that such a debt, contracted with another company of the same group, constitutes (or is part of) a wholly artificial arrangement, whose sole purpose is to erode the Netherlands tax base.

25. Nevertheless, under Article 10a(3) of the Law on Corporation Tax, the taxable person can rebut that presumption and, thus, deduct such interest from its taxable profits by showing either that (a) the loan is, in fact, predominantly based on commercial considerations or (b) a profit tax or income tax that is reasonable in accordance with the Netherlands criteria (namely, around 10%) is ultimately levied on the interest in respect of the company that granted the loan.

26. By its three questions, which it is appropriate to deal with together, the referring court asks, in substance, whether that national legislation is compatible with Article 49 TFEU on the freedom of establishment, Article 56 TFEU on the freedom to provide services, and/or Article 63 TFEU on the free movement of capital.

27. As those questions refer to several fundamental freedoms, it is necessary to establish, at the outset, the freedom that is applicable to the present case (Section A). I will subsequently assess whether the national law at issue engenders a restriction on the relevant freedom (Section B), before considering whether such a restriction is permissible (Section C).

A. Freedom of establishment is the relevant freedom

28. It is settled case-law that, in order to determine the fundamental freedom which is applicable to a given piece of national legislation, the purpose of that legislation must be taken into consideration.

29. As the intervening governments and the Commission submit, it seems clear to me that, in the light of its purpose, Article 10a(1)(c) of the Law on Corporation Tax concerns the freedom of establishment, guaranteed in Article 49 TFEU.

30. In that regard, it is apparent from the Court’s case-law that national rules concerning only relationships within a group of companies primarily affect the freedom of establishment, under Article 49 TFEU. Similarly, national law which is intended to apply only to those shareholdings that enable the holder to exert a definite influence on a company’s decisions and to determine its activities also falls within the scope of that same EU law provision.

31. Article 10a(1)(c) of the Law on Corporation Tax applies, I recall, when a debt is contracted by a taxable person (i) with a ‘related entity’ and (ii) for the financing of an acquisition or extension of an interest in an entity that was already ‘related’ to that person prior to the acquisition or extension or an entity that subsequently becomes ‘related’ to that person. Pursuant to Article 10a(4) thereof, entities are considered ‘related’, for the purpose of the first provision, where they hold, directly or indirectly, a minimum of 33.3% of the shares in the other, or that a third entity holds 33.3% of the shares in both entities.

32. Therefore, the contested provisions concerns only relationships within a group of companies, as its purpose is limited to intra-group loans. Furthermore, it applies only to interest on such a loan contracted by the taxable person for the purpose of acquiring a percentage of shareholding which is high enough to enable that person to exert a definite influence over the targeted entity. In fact, the order for reference specifies that X actually possesses a significantly larger share in F than the minimum required by those provisions.

33. Accordingly, I consider it appropriate to examine the national law at issue, and respond to the questions submitted by the referring court, solely in the light of Article 49 TFEU.

B. Such a national legislation entails a restriction on freedom of establishment

34. I recall that freedom of establishment, conferred on EU nationals by Article 49 TFEU, entails, according to Article 54 TFEU, for companies or firms formed in accordance with the law of a Member State and having their registered office, central administration or principal place of business within the European Union, the right to exercise their activity in another Member State through a subsidiary, branch or agency.

35. In the present case, X argues that Article 10a(1)(c) of the Law on Corporation Tax entails a restriction on that freedom because that provision treats less favourably cross-border situations than purely internal ones.

36. Specifically, X submits that, if the taxable person contracts a loan debt with a related entity (for instance, the internal bank of the group it is part of) established in the Netherlands, it can systematically deduct from its taxable profits the interest on that loan, since the condition provided in Article 10a(3)(b) of that law is always satisfied. The related entity is obviously subjected, in relation to that interest, to a profit or income tax ‘that is reasonable in accordance with the Netherlands criteria’, as the Netherlands tax rate of 10% applies. By contrast, where the taxable person contracts such a loan debt with a related entity established in another Member State, it is harder for that person to deduct the interest on that loan, since that condition would not always be satisfied (as lower profit tax or income tax may be applied by other Member States to such an entity, like Belgium did with respect to C at the material time). Where that is not the case, the taxable person could only obtain that advantage by meeting the condition laid down in Article 10a(3)(a), that is to say by demonstrating that the loan and the associated transaction are predominantly based on commercial considerations. The referring court and the Commission agree with that assessment.

37. Conversely, the Netherlands Government argues that there is no restriction on freedom of establishment. In the case in the main proceedings, only A (the parent company), seated in Belgium, has exercised that freedom notably by creating its subsidiary X in the Netherlands. Freedom of establishment aims to guarantee to such a parent company the benefit of national treatment in the Member State where it creates a subsidiary, by prohibiting all discrimination based on the place in which it has its seat. In the present case, Article 10a(1)(c) of the Law on Corporation Tax does not entail such a discrimination. Indeed, with respect to the possibility, for a Netherlands-based company, to deduct interest on intra-group loans, that provision applies the same way, whether the parent of the latter is seated in the Netherlands or in another Member State.

38. On a subsidiary basis, the Netherlands Government submits that, even if the location of the lending entity (the internal bank of the group) were a relevant consideration to assess the existence of a restriction on freedom of establishment, there would still be no difference of treatment amounting to such a restriction. Indeed, Article 10a(1)(c) of the Law on Corporation Tax applies without distinction to debts contracted between related entities established in the Netherlands and debts contracted between related entities established in different Member States, and the condition laid down in Article 10a(3)(b) may, in fact, be satisfied even where the internal bank has its seat in another Member State. The Spanish Government shares, in essence, that view.

39. I concur with X and the Commission.

40. Admittedly, as the Netherlands Government submits, the focus of the analysis, here, should be whether Article 10a(1)(c) of the Law on Corporation Tax restricts the exercise by A of its freedom of establishment, since it is, indeed, the only company that used that freedom, inter alia, by creating a subsidiary (X) in a Member State (the Netherlands) other than the one in which it has its seat (Belgium). I also admit that that provision does not entail a discrimination based on the place in which that company has its seat. Under that provision, A’s subsidiary, X, would have been treated the same if A had been established in the Netherlands instead of Belgium.

41. Nevertheless, the concept of restriction to freedom of establishment is not limited to such a discrimination. Whilst the provisions of the TFEU concerning that freedom aim at ensuring that foreign nationals and companies are treated in the host Member State in the same way as nationals and companies of that State, the Court has repeatedly ruled that freedom of establishment is very broad. In fact, all measures which prohibit, impede or render less attractive its exercise must be considered to be restrictions on that freedom.

42. In the present case, I would observe, first, that, if the contested provisions of Netherlands law treat differently, with respect to the possibility to deduct interest on an intra-group loan, a tax-resident subsidiary (such as X) of a parent company domiciled in another Member State (such as A) depending on whether the internal bank of the group that granted that loan (here, C) is located in the Netherlands or in another Member State, then that difference of treatment is liable to make the exercise by that parent company of its freedom of establishment less attractive.

43. Such a difference could dissuade that parent company from structuring its group the way it wants, by setting the internal bank of the latter in a Member State other than the Netherlands. De facto, it puts cross-border groups of companies, the existence of which stems on the exercise of freedom of establishment, at a disadvantage compared to groups which are ‘purely internal’ to the Netherlands. Indeed, the former are, conversely to the latter, often structured in such a way that their internal bank is located in another Member State.

44. The reasoning is the same if one flips the perspective and reasons, instead, in the light of the hypothetical scenario, evoked by the Netherlands Government, where A would have its seat in the Netherlands. In that scenario as well, such a difference of treatment would be liable to make the exercise by that company of its freedom of establishment through the creation of an internal bank in another Member State less attractive. Indeed, if that company did so, it could suffer a disadvantage by comparison with a similar company which does not exercise that freedom and creates, instead, an internal bank within the Netherlands.

45. The Court’s judgment in Lexel confirms, in my view, that interpretation. I recall that that case concerned the impossibility, under Swedish law, for a Swedish company, part of an international group, to deduct the interest on a loan debt contracted with the internal bank of the group, namely another company located in France. The parent company of that group also had its seat in France. In that case, the difference of treatment lied in the fact that, had the internal bank been in Sweden, such a deduction would have been possible. The Court rightly took the view that that difference amounted to a restriction to freedom of establishment.

46. I would observe, secondly, that the contested provisions of Netherlands law would seem, indeed, to create such a difference of treatment based on the seat of the internal bank of groups of companies.

47. Admittedly, as the Netherlands Government submits, the relevant provisions of Netherlands law do not directly distinguish according to whether the internal bank that granted the intra-group loan in question to the taxable person is seated in the Netherlands or in another Member State. In particular, the criterion laid down in Article 10a(3)(b) of the Law on Corporation Tax is not whether that bank is subjected, in relation to that interest, to a profit or income tax ‘in the Netherlands’. That is a notable difference with the case that led to the judgment in Lexel, where a similar condition required, for the deduction of such interest to be obtained, the internal bank to be taxed in Sweden.

48. However, as X argues, the criterion used in Article 10a(3)(b) of the Law on Corporation Tax (namely that the internal bank be subjected, on that interest, to ‘a profit tax or income tax that is reasonable in accordance with the Netherlands criteria’ (that is to say, at least 10%)), while seemingly objective, may de facto disadvantage cross-border situations.

49. Admittedly, the contrary arguments of the Netherlands Government carry some weight. That government submits, drawing an analogy with the judgment of the Court in Köln-Aktienfonds Deka, that that criterion is not specific to the Netherlands market, in such a way that it could only be satisfied where taxable persons obtain intra-group loans from internal banks seated in the Netherlands. At the material time, all the Member States applied a corporate tax rate of 10% or higher. Thus, that condition would generally be met even where such a loan is obtained from internal banks seated in other Member States, save in the exceptional situation where the bank in question benefits (like C) from a preferential tax regime in the State where it is established. That government also asserts that there are circumstances where interest charges on loans are taxed at a rate that is lower than 10% in the Netherlands. Consequently, there exist instances in which the conditions laid down in Article 10a(3)(b) of the Law on Corporation Tax are not met although the internal bank has its seat in that Member State. Thus, a parent company, like A, would not be dissuaded from establishing such a bank in a Member State other than the Netherlands, or put at a disadvantage where it does so.

50. Nevertheless, in my view, national laws do not have to use criteria which are specific to a national market, nor to the sole benefit of the domestic companies thereon, in order for them to de facto disadvantage cross-border situations. The crucial question, in that regard, is whether the criteria used therein are liable to affect cross-border situations more than purely internal ones. To determine whether that is the case here, one needs to compare the (potential) proportion of groups of companies with internal banks seated in the Netherlands that could not meet the condition laid down in Article 10a(3)(b) of the Law on Corporation Tax to the (potential) proportion of groups of companies with internal banks in other Member States that would be disadvantaged by that condition.

51. Although this would be for the referring court to verify, it seems that, in proportion, the second category of groups of companies is more affected by the condition in question than the first.

52. On the one hand, the Netherlands Government admitted, at the hearing, that the condition laid down in Article 10a(3)(b) of the Law on Corporation Tax is virtually always fulfilled where the internal bank has its seat in the Netherlands. Indeed, interest charges on a loan are taxed, in the Netherlands, at a rate lower than 10% only in the anecdotal scenario where the loan is granted by a foundation or an association, which does not have a commercial activity. At the hearing, X submitted, and the Netherlands Government confirmed that that exception is never applied in relation to commercial internal banks such as C and that no other exception exists in Netherlands law. Thus, the proportion of groups of companies with internal banks seated in the Netherlands that could not meet that condition is negligible.

53. On the other hand, the Netherlands Government admits that the condition laid down in Article 10a(3)(b) of the Law on Corporation Tax would not be fulfilled where the internal bank has its seat in a Member State that applies a preferential tax regime to such a bank. One can reasonably assume that various iterations of such regimes exist in the 27 Member States of the European Union. Furthermore, the Commission observes, not without merit, that, while all Member States have a general, or theoretical, rate of corporate tax of 10%, the effective rate is often lower. All in all, a sufficiently significant proportion of groups of companies with internal banks in Member States other than the Netherlands are liable to be disadvantaged.

54. Finally, I am not convinced by the argument of the Spanish Government that such a difference in treatment is mitigated by the alternative condition, laid down in Article 10a(3)(a) of the Law on Corporation Tax, which permits a taxable person to deduct the interest on an intra-group loan if it can substantiate the commercial considerations behind the loan in question and the associated transaction. In fact, that provision represents a burden on that person, for the purpose of deducting interest, which it would (virtually) never have to bear if the internal bank that granted the loan had its seat in the Netherlands (since, as discussed above, the condition under Article 10a(3)(b) would virtually always be fulfilled in that case). That confirms the difference of treatment at issue.

C. Such a restriction is permissible under Article 49 TFEU

55. That being said, I share the view of the intervening governments and the Commission that the restriction on freedom of establishment entailed by Article 10a(1)(c) of the Law on Corporation Tax is permissible under Article 49 TFEU. Indeed, as will be explained in the next subsections, that restriction is justified by an overriding reason in the public interest (Subsection 1). Furthermore, that restriction is appropriate to ensuring the attainment of the legitimate objective which it pursues (Subsection 2) and does not go beyond what is necessary in order for it to be attained (Subsection 3).

1. The restriction is justified

56. The intervening governments and the Commission submit that the restriction on freedom of movement entailed by Article 10a(1)(c) of the Law on Corporation Tax is justified on grounds relating to the fight against abusive tax avoidance. The specific objective of that provision is, precisely, to prevent conduct involving the creation of wholly artificial arrangements which do not reflect economic reality, with a view to escaping the tax normally due on the profits generated by activities carried out in the Netherlands. The referring court shares that view.

57. It is settled case-law that such an objective constitutes an overriding reason in the public interest in the field of taxation. In my view, there is no doubt that Article 10a(1)(c) of the Law on Corporation Tax genuinely pursues that objective and, thus, can be justified by such an overriding reason.

58. The Court has already made such a finding in its judgment in X and X in relation to a provision of the same law (but in an earlier version) which was, in substance, identical to Article 10a(1)(c). The sole difference between the two is that the earlier version concerned internal restructuring only, whereas Article 10a(1)(c) applies also to external acquisitions. However, the objective pursued by either provisions is the same. As the Court observed in that judgment, ‘it is a question of preventing own funds of a group from being artificially presented as funds borrowed by a Netherlands entity of that group and the interest in respect of that loan from being deducted from the taxable profits in the Netherlands’, while that interest is not otherwise (reasonably) taxed. The purpose of the prohibition of the deduction of interest in respect of intra-group loans is expressly confirmed by the rule that loan interest may be deducted, pursuant to Article 10a(3)(a), if such a loan and the associated transaction are economically justified.

2. The restriction is appropriate

59. Pursuant to the Court’s settled case-law, the requirement that any restriction on freedom of establishment be ‘appropriate’ encompasses two cumulative criteria: the measure at issue must, first, be suitable to contribute to the achievement of the objective pursued, as well as, secondly, ‘genuinely reflect a concern to attain it and be implemented in a consistent and systematic manner’.

60. That the present case meets the first criterion is undisputed. By providing that a taxable person cannot deduct, from its taxable profits, interest on an intra-group loan which constitutes (or is part of) a wholly artificial arrangement designed to erode the Netherlands tax base, Article 10a(1)(c) of the Law on Corporation Tax can thwart such arrangements. Evidently, that legislation contributes to the achievement of the objective pursued.

61. Whether the present case also meets the second criterion is, by contrast, disputed by X. The appellant argues that Article 10a(1)(c) of the Law on Corporation Tax does not combat artificial intra-group loans in a consistent and systematic manner. Indeed, if the interest on such a loan is taxed at a reasonable rate in the Member State where the lending company is established, the Netherlands-based borrowing company can deduct that interest (under Article 10a(3)(b) of that law), even where the loan and/or the associated transaction have no economic justification.

62. In my view, the fact that the contested provisions allow for the deduction of interest on an intra-group loan in the scenario mentioned by X is, in reality, consistent with the objective pursued. Admittedly, in that scenario, allowing such a deduction may entail a shifting of taxable profits from the Netherlands to the Member State where the lending company is established. Nevertheless, if that interest is taxed at a reasonable rate in that last State, taxation is not avoided altogether. Thus, the fight against tax avoidance could not justify refusing that deduction in the scenario in question.

3. The restriction is necessary

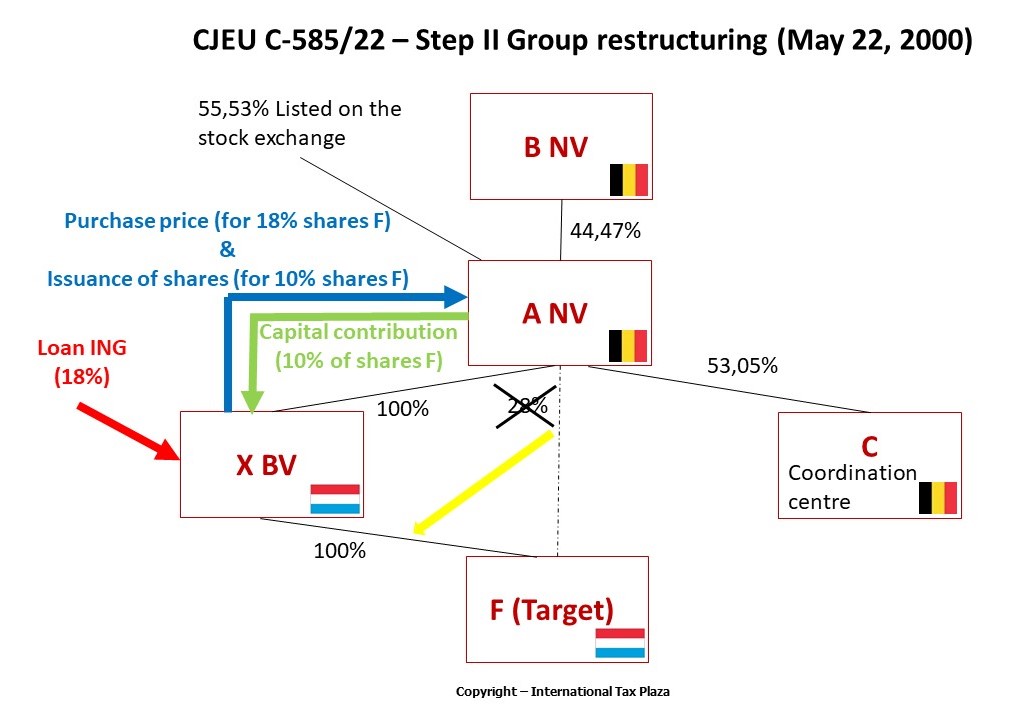

63. In my view, the restriction entailed by the contested provisions of Netherlands law does not go beyond what is necessary to achieve its legitimate purpose since the application of those provisions is limited to wholly artificial arrangements (a) and the consequences stemming from a transaction being characterised as such are not excessive (b).

(a) The application of the contested rules is limited to wholly artificial arrangements

64. Pursuant to the Court’s settled case-law, for national provisions to be considered necessary in the light of the objective of preventing wholly artificial arrangements, designed to escape the tax normally due on the profits generated by activities carried out on the national territory, the application of those provisions must be limited to such arrangements, leaving legitimate transactions aside.

65. The issue of whether the Netherlands rules satisfy that requirement was left open by the Court in its judgment in X and X. Nevertheless, the intervening governments and the Commission submit that it is satisfied. Indeed, Article 10a(1)(c) of the Law on Corporation Tax covers only transactions which do not reflect economic reality, where intra-group loans are concluded with a taxable entity in the Netherlands for the only (or main) purpose of creating a debt deductible from the taxable profits of that entity, thus, eroding the Netherlands tax base. By contrast, where the loan and associated transaction predominantly rest on valid commercial reasons, that provision does not apply, according to Article 10a(3)(a) of that law.

66. X disagrees. In its view, the opposite conclusion is set out in the judgment in Lexel. In that case, the Court reviewed the compatibility with Article 49 TFEU of the Swedish rules on corporate tax, specifically the provisions on deduction of interest expenses. Much like the Netherlands rules, those provisions stated, in substance, that such a deduction was, by way of an exception, not allowed where the taxable entity had taken the loan in question with a related entity, unless it was shown that that loan was justified primarily on commercial grounds and, thus, had not been concluded just to create a deductible debt. There as well, the Swedish Government argued that those provisions aimed at preventing wholly artificial arrangements designed to escape the tax normally due on the profits generated by activities carried out on the national territory. The Court considered that the Swedish provisions could not be justified on that ground because, in its view, their application was not limited to such arrangements. The Court stated the following in that regard:

’53 As the [Swedish tax authorities] acknowledged in essence at the hearing, the exception [to the right to deduction] relates to debts resulting from civil-law transactions, not relating solely to fictitious arrangements. Consequently, according to [those authorities’] assessment of the objectives of the transaction at issue, the exception may also cover transactions carried out on an arm’s-length basis, that is to say, in conditions analogous to those which would apply between companies which are independent of one another.

54 In other words, the fictitious nature of the transaction at issue is not decisive for refusing the right to a deduction because the intention of the company concerned to take on a debt, mainly for tax reasons, is sufficient to justify refusal of the right to a deduction. …

…

56 It must be held that the exception [to the right to deduction] may include within its scope transactions which are carried out at arm’s length and which, consequently, are not purely artificial or fictitious arrangements created with a view to escaping the tax normally due on the profits generated by activities carried out on national territory.’

67. In X’s view, it follows that national tax authorities cannot consider an intra-group loan (or the series of transactions it is part of) to be a wholly artificial arrangement and refuse, on that ground, the deduction of interest, simply because that loan was contracted for tax reasons. It would be perfectly legitimate for a group to do so. Such a loan would be artificial only if, and in so far as, the interest paid by the borrowing company to the lending company exceeds what those companies would have agreed upon on an arm’s length basis, that is to say if the applicable interest rate is higher than the market rate those companies would have agreed on if they had not formed part of the same group. By contrast, if such a loan is carried out on an arm’s length basis, then, irrespective of its purpose, it cannot be regarded as artificial. That is the case with respect to the loans concluded between X and F.

68. Still in the appellant’s view, because Article 10a(1)(c) and (3) of the Law on Corporation Tax erroneously focuses on the purpose for which an intra-group loan had been contracted (whether it is tax avoidance or commercial reasons) instead of the terms applicable to that loan, the deduction of interest may be refused not only in relation to loans with excessive interest rates (which are artificial, as explained above), but also in relation to loans to which the usual market rate applies (and which, for that reason, cannot be regarded as such). Hence, just like in the case that led to the judgment in Lexel, the scope of those provisions is not limited to wholly artificial arrangements, but encompasses legitimate transactions as well.

69. That debate is at the heart of the first question of the referring court. Clearly, one cannot determine whether Article 10a(1)(c) of the Law on Corporation Tax applies only to ‘wholly artificial arrangements’ if the very meaning of that concept is in dispute. It is equally clear that the intervening governments and the Commission, on the one hand, and X, on the other, suggest very different approaches in that regard. The first approach consists in focusing on the purpose for which a loan was contracted. The second one focuses only on the terms applicable to that loan. The first approach gives the Netherlands tax authorities a significantly wider margin of manoeuvre than the second, which, conversely, offers more certainty to tax payers. Under the first approach, national tax authorities can characterise an intra-group loan as a ‘wholly artificial arrangement’ (or as a part of such an ‘arrangement’) and refuse, on that ground, the deduction of interest, if it was taken for the main purpose of obtaining a tax advantage, irrespective of the terms applicable to the loan. Under the second approach, an intra-group loan is ‘immune’ against such consequences as long as its terms, including the interest rate, are, so to speak, ‘normal’, even if it was put in place for tax purposes.

70. At this stage, I wish to highlight that, while the intervening governments and the Commission spent a significant part of their respective submissions explaining that ‘their’ approach is not contrary to the judgment in Lexel because (i) the present case should be distinguished from the case that led to that judgment and/or (ii) that judgment cannot be read in the way suggested by X, I am not convinced by those explanations. It follows from point 66 above that, on all relevant aspects, the contested provisions of Netherlands law bear a striking resemblance to the rules at issue in Lexel. Notably, those rules have an identical target: intra-group loans taken for the sole (or main) purpose of obtaining a tax advantage. The general issue, thus, is the same: if, and to what extent, such a loan can be regarded as a ‘wholly artificial arrangement’ (or as a part of such an ‘arrangement’) and treated as such by tax authorities. Furthermore, the judgment in Lexel is neither vague nor ambiguous and, thus, open to different readings on that issue. In my view, it can only be read in the way that X understood it. The Court considered, indeed, that the purpose for which the loan was concluded is not relevant and, instead, distinguished between loans contracted on an arm’s length basis (which it regarded as genuine) and those which are not contracted on such basis (which it regarded as artificial). Therefore, the only question left is whether the Court should, in the present case, confirm Lexel, or depart from it.

71. In my view, the approach suggested by the intervening governments and the Commission is the correct one. Consequently, I urge the Court to revisit the approach it took in the judgment in Lexel on the matter at issue.

72. Freedom of establishment, as guaranteed by Article 49 TFEU, offers quite a wide opportunity for tax ‘optimisation’. The Court has repeatedly held that European groups of companies can legitimately use that freedom to establish subsidiaries in Member States for the purpose of benefiting from a favourable tax regime. Thus, as X submits, A could legitimately choose to establish the internal bank of its group, C, in Belgium for that very purpose. Similarly, C may well grant loans to other companies of the group established in other Member States, like X in the Netherlands. Cross-border intra-group loans are not, per se, objectionable. Certainly, such a loan may entail a reduction of the corporate tax base of the borrowing company in the Member State where it is established. Indeed, by deducting the interest on that loan from its taxable profits, that company reduces its tax liability with respect to that Member State. In effect, some of the profits made by the borrowing company are shifted, in the form of interest charges, from the Member State where it is established to the Member State where the lender company has its seat. However, that is something that the Member States must, in principle, accept in an integrated, single market such as the internal market of the European Union.

73. Nevertheless, the Court recognised a clear limit in that regard. It is a general legal principle that EU law, including freedom of establishment, cannot be relied on for abusive ends. The concept of ‘wholly artificial arrangements’ must be read in that light. Pursuant to the settled case-law of the Court, it is abusive for economic operators established in different Member States to carry out ‘artificial transactions devoid of economic and commercial justification’ (or, stated differently, ‘which do not reflect economic reality’), thus fulfilling the conditions to benefit from a tax advantage only formally, ‘with the essential aim of benefiting from [that] advantage’.

74. Furthermore, in its judgment in X (Controlled companies established in third countries), the Court has specified, with respect to the free movement of capital guaranteed by Article 63 TFEU, that ‘the artificial creation of the conditions required in order to escape taxation in a Member State improperly or enjoy a tax advantage in that Member State improperly can take several forms as regards cross-border movements of capital’. In that context, it held that the concept of ‘wholly artificial arrangement’ is capable of covering ‘any scheme which has as its primary objective or one of its primary objectives the artificial transfer of the profits made by way of activities carried out in the territory of a Member State to [another country] with a low tax rate’.

75. That interpretation is equally valid, in my view, with respect to the intra-group transactions covered by the freedom of establishment. Indeed, that interpretation is perfectly in line with the explanation given in point 73 above. Furthermore, with respect to national legislation tackling intra-group transactions, such as the contested Netherlands rules, free movement of capital and freedom of establishment are inextricably linked. It is because capital cannot circulate freely between companies of the same group that freedom of establishment is restricted. Thus, those rules could, theoretically, be reviewed under either fundamental freedom. Hence, there is no reason to apply different criteria depending on the applicable freedom.

76. In sum, as the intervening governments and the Commission submit, in order to determine whether an intra-group loan constitutes (or is a part of) a ‘wholly artificial arrangement’, the objective pursued by the economic operators in question is decisive. An intra-group loan constitutes such an ‘arrangement’ where that transaction was carried out for the sole (or main) purpose of benefiting from a tax advantage (such as the deduction of the interest on that loan from taxable profits), as demonstrated by the fact that it is otherwise devoid of economic and/or commercial justification (or, stated differently, ‘does not reflect economic reality’). Whether that is the case requires an overall assessment of the relevant facts and circumstances of the case.

77. As the Netherlands Government observes, and as the Court implied in the judgment in Test Claimants in the Thin Cap Group Litigation, two scenarios may be distinguished in that regard.

78. On the one hand, an intra-group loan concluded for valid economic and/or commercial reasons may contain specific terms which do not ‘reflect economic reality’. An excessively high interest rate may be agreed (artificially, since the group is, ultimately, paying that interest to itself) in an otherwise legitimate transaction with the aim of benefiting from a correspondingly high tax deduction in the Member State where the borrowing company is established. The arm’s length principle (that is, whether unrelated companies would have agreed on the same terms in comparable circumstances) serves as an objective benchmark to determine whether that is indeed the case.

79. On the other hand, related companies may also conclude a loan which is overall devoid of economic and/or commercial justification, for the sole (or main) purpose of generating interest payments in the seat of the borrowing company. Contrary to what the Court ruled in paragraph 54 of the judgment in Lexel, and as indicated in point 76 above, that motive, demonstrated by that absence of justification, is a decisive consideration. For that very reason, such a loan must be regarded as ‘wholly artificial’. Whether the terms applicable to that loan correspond to those that would have been agreed by unrelated entities in similar circumstances is, by contrast, an irrelevant consideration. As the Netherlands Government submits, such a loan cannot be regarded as ‘reflecting economic reality’ simply because the applicable interest rate is set at market value. In fact, that loan does not ‘reflect economic reality’ because, but for the relationship between the companies and the tax advantage sought, it would never have been taken. Such artificially generated debts are precisely the target of Article 10a(1)(c) of the Law on Corporation Tax.

80. As the intervening governments and the Commission observe, if intra-group transactions devoid of economic and/or commercial justification could never be regarded as ‘wholly artificial arrangements’ where they are carried out in an arm’s length basis, that would seriously impede the potential for national tax authorities to combat abusive tax avoidance. The arm’s length principle would, effectively, be turned into an undesirable ‘safe harbour’ for multinational groups. Their astute tax advisers would be free to conjure up all sorts of convoluted arrangements designed for the sole purpose of eroding a company’s corporate tax liability in a Member State and transferring its profits to another State with a lower tax rate. As long as those advisers cleverly stipulate terms therein reflecting the ones usually found on the market, those arrangements would be ‘immune’ from counteracting measures by tax authorities.

81. That would be all the less desirable given the fact that national tax authorities have, under the general principle of prohibition of abuse of EU law, not merely the right, but the duty to prevent tax advantages being obtained through ‘wholly artificial arrangements’. Indeed, effective measures against tax avoidance are essential not only to ensure the sovereign right of the Member States to tax income and profits generated in their territory, but also for the functioning of the internal market, generally. Abusive tax avoidance threatens the economic cohesion and the proper functioning of the internal market, by distorting the conditions of competition.

82. In fact, the growing impact of tax base erosion and profit shifting strategies by multinational groups on the public treasury of the Member States and the functioning of the internal market led the European Union to deal with this matter. The EU legislature has adopted various measures in that regard, including Council Directive (EU) 2016/1164 laying down rules against tax avoidance practices that directly affect the functioning of the internal market (‘the Anti Tax Avoidance Directive’). That directive contains, in Article 6, a ‘general anti-abuse rule’, drafted in the light of the case-law of the Court referred to in point 73 above, and which should be interpreted accordingly. If national tax authorities could not treat intra-group transactions devoid of economic and/or commercial justification as ‘wholly artificial arrangements’ where they are carried out at an arm’s length basis, that policy would be undermined. Furthermore, the ‘anti-abuse rule’ in question would lose a significant part of its effectiveness. A great deal of transactions put in place not ‘for valid commercial reasons which reflect economic reality’ but ‘for the main purpose … of obtaining a tax advantage’ (to use the terms of that provision) would be out of its reach.

83. For the reasons set out above, I am of the view that the Court should, in the present case, depart from paragraphs 53, 54 and 56 of the judgment in Lexel. Intra-group loans, put in place without any valid commercial and/or economic justification for the sole (or main) purpose of creating a deductible debt in the seat of the borrowing company constitute ‘wholly artificial arrangements’, whether or not they are carried out on an arm’s length basis. National provisions which target such loans must be considered necessary in the light of the objective to prevent those ‘arrangements’.

84. With that being clarified, some final arguments brought forward by X concerning the scope of Article 10a(1)(c) of the Law on Corporation Tax remain to be examined.

85. First, X submits that the Netherlands tax authorities may apply that provision to an ill-defined range of intra-group transactions because its scope depends on a condition formulated in vague and ambiguous terms, namely whether or not the loan and the associated legal transaction ‘are predominantly based on commercial considerations’ (under Article 10a(3)(a) of that law). For that reason, the contested Netherlands rules do not comply with the principle of legal certainty, as companies could not foresee with sufficient precision which transactions could be regarded as abusive by the tax authorities.

86. Pursuant to the settle case-law of the Court, the principle of legal certainty requires, most notably, that rules of law be sufficiently clear, precise and predictable in their effect, especially where they have negative consequences on taxpayers.

87. In that regard, I would observe that the contested Netherlands rule are formulated much like other anti-abuse clauses found in national law and EU law. In particular, the application of the ‘general anti-abuse rule’ laid down in Article 6 of the Anti Tax Avoidance Directive to a given transaction similarly depends on whether that transaction was made ‘for valid commercial reasons which reflect economic reality’ and not ‘for the main purpose … of obtaining a tax advantage’. Admittedly, those are open concepts which, by nature, create some degree of uncertainty as to their scope. Furthermore, as I indicated in point 76 above, whether such conditions are fulfilled in a given case requires a case-by-case, overall assessment of a set of facts and circumstances, which also creates some degree of uncertainty.

88. Nevertheless, that degree of uncertainty is an unavoidable and acceptable side effect of such anti-abuse provisions. As Advocate General Kokott observed in her Opinion in SGI, ‘legislation aimed at counteracting abusive practices must inevitably have recourse to imprecise legal concepts in order to cover the greatest number of conceivable arrangements created for the purposes of tax avoidance’. Furthermore, those provisions are meant to tackle conduct which is disguised as legitimate and is, thus, complex to apprehend.

89. It does not follow that the application of such a legislation is left to the complete discretion of the tax authorities, making it unpredictable in its effects. As the referring court and the Netherlands Government indicate, whether a given arrangement is ‘wholly artificial’ is determined on the basis of objective and verifiable elements.

90. As indicated in point 79 above, the decisive question is whether, but for the relationship between the companies and the tax advantage sought, the intra-group loan in question would never have been taken. The type of analysis to be carried out under such a test is sufficiently clear. The assessment of the relevant facts and circumstances involves an examination of the overall structure and apparent purpose of the arrangement whose that loan forms part. As the referring court indicates, the questions are essentially the following: had the tax advantage not been there, would the taxpayer concerned have had an interest in setting up the arrangement in question? Does the structure of the arrangement appear, in the light of its stated purpose, overly complex and, especially, includes steps which appear (if were not for their impact on tax liability), unnecessary? These are questions that should not be difficult to address for tax professionals and multinational groups of companies, who can regulate their conduct accordingly.

91. In the case in the main proceedings, the referring court and the Netherlands Government explain that, while the acquisition of an external entity and the taking of a loan for that purpose by a taxable entity with a related entity are generally regarded as ‘predominantly based on commercial considerations’ within the meaning of Article 10a(3)(a) of the Law on Corporation Tax, the arrangement surrounding the acquisition of F by X has been seen as ‘wholly artificial’ because of its complex nature and the (apparently) unnecessary steps involved. Those steps were, I recall, (i) the redirection of A’s own funds towards C; (ii) the subsequent conversion of those funds into a loan granted to X; (iii) the acquisition of F by X; and (iv) the constitution of a single fiscal unit between F and X, so that the interest charges paid by X to C could be deducted from the taxable profits generated by F in the Netherlands.

92. In particular, the fact that the loan granted to X was provided with funds ‘redirected’ from A taints, prima facie, the whole arrangement. It begs the question of whether that loan was really needed and why it was X, instead of A, that acquired F. The Commission submits that, in a counterfactual scenario reflecting economic reality, F would have been acquired by A and, as such, fewer steps would be involved in that acquisition. However, in that scenario, X would pay, with respect to the profits generated by it and F in the Netherlands, dividends to A. Such a distribution would not entail a reduction of the corporate tax liability in the Netherlands. By contrast, under the arrangement pursuant to which F was acquired by X through a loan granted by C with funds redirected from A, because X deducted the interest on that loan from the taxable profits generated by it and F in the Netherlands, the tax liability of those two companies in that Member State was reduced to almost zero.

93. In such a situation, the referring court and the Netherlands Government highlight that it is for the taxpayer to justify, to a plausible degree, the economic and/or commercial reasons underpinning the steps of the arrangement and, in particular, the ‘redirection’ of the funds lent. In accordance with the case-law of the Court, the taxable person is duly given the opportunity, without being subject to undue administrative constraints, to provide evidence in that regard. Furthermore, if the tax authorities, in the light of the explanations and evidence provided by the taxpayer, still considers the arrangement to be artificial, the latter can challenge those authorities’ decision before the courts. Simply, X did not manage to provide such evidence in the case in the main proceedings, and the national courts confirmed the tax authorities’ decision.

94. X replies that the issue of which economic and/or commercial reasons can validly be advanced to justify such a ‘redirection’ of funds is unclear in the practice of the Netherlands tax authorities and courts. Until now, explanations have always been rejected. Furthermore, those authorities and courts fail to take into account, in that regard, considerations pertaining to the structure of the group at issue, such as the fact that the lending company generally plays (like C in the present case) a key role in the financing of that group.

95. In my view, there will always be grey areas in the operation of an anti-abuse clause such as Article 10a(1)(c) of the Law on Corporation Tax. This does not make that rule incompatible with the principle of legal certainty. In the present case, the practice of the tax authorities and the Netherlands courts will progressively clarify the issue highlighted by X. In that regard, I will limit myself to observing that, when evaluating whether an arrangement should be regarded as artificial or economically justified, tax authorities and courts should consider all valid economic reasons, including financial ones. It cannot be excluded that the reason advanced by X qualifies as such. It would be for the referring court to assess the matter.

96. Secondly, X contests the allocation of the burden of proof under the contested provisions of Netherlands law. Specifically, the appellant submits that Article 10a(1)(c) of the Law on Corporation Tax introduces a general presumption of abuse, going beyond what is necessary to achieve the objective pursued. The Netherlands tax authorities may, on the basis of that provision, refuse a taxable entity the deduction of the interest it pays on an intra-group loan without being required to provide even prima face evidence of abuse, whereas that entity, to obtain that tax advantage, has the burden to prove, under Article 10a(3)(a) of that law, that the loan and the associated legal transaction are predominantly based on commercial considerations.

97. I disagree. Clearly, where national tax authorities seek to refuse a tax advantage to a taxpayer on grounds of abuse, they have, generally speaking, the burden of establishing that the latter is attempting to obtain that advantage through a ‘wholly artificial arrangement’, taking into account all the relevant facts and circumstances of the case, in the light of the criteria discussed above. It does not mean, however, that Member States are prevented from enacting legal presumptions in their national law, provided that they are specific and rest on sufficient grounds.

98. In the present case, Article 10a(1)(c) of the Law on Corporation Tax, and the obligation for the tax payer to justify that the arrangement in question is genuine, apply, in principle, only in cases where an intra-group loan has been concluded by a taxable entity with a related entity established in another Member, in which the interest charges collected by the latter are not taxed, or not taxed at a reasonable rate. Those specific circumstances can legitimately be regarded as indications of conduct that might amount to abusive tax evasion, justifying a reversal of the burden of proof.

99. Once the national tax authorities have determined that such an intra-group loan falls within the scope of that provision and, thus, might have been concluded for tax avoidance purposes, it is not excessive for those authorities to require the taxpayer to adduce evidence of the economic and/or commercial character of the arrangement and to refuse the deduction of the interest on that loan where it fails to do so. After all, the taxpayer is best placed to furnish explanations and evidence of the motives of the transactions it carries out. Besides, the Court has repeatedly ruled that ‘there is no reason why the tax authorities concerned should not request from the taxpayer the evidence that they consider they need for a concrete assessment of the taxes … concerned and, where appropriate, refuse the [advantage] applied for if that evidence is not supplied’.

(b) The consequences stemming from a transaction being regarded as such an arrangement are not excessive

100. Pursuant to Article 10a(1)(c) of the Law on Corporation Tax, where an intra-group loan is found to constitute a wholly artificial arrangement (under the conditions discussed in the previous subsection), the deduction of the interest on that loan is disallowed in full when determining the profits of the borrowing taxable entity in the Netherlands.

101. While the referring court considers that such a consequence logically follows from the finding of artificiality of the loan, it nevertheless wonders (specifically, by its second question) whether, in the light of paragraph 51 of the judgment in Lexel, a complete refusal of the right to a deduction goes beyond what is necessary to achieve the objective pursued. Indeed, the Court stated, in that paragraph, that, where tax authorities take the view that a loan concluded by a taxable entity with a related entity represents a wholly artificial arrangement, ‘the principle of proportionality requires that the refusal of the right to a deduction should be limited to the proportion of that interest which exceeds what would have been agreed had the relationship between the parties been one at arm’s length’.

102. I agree with the intervening governments and the Commission that that is not the case. In that respect, the two scenarios mentioned in points 78 and 79 above should be distinguished here as well.

103. On the one hand, where artificiality consists in the unusually high interest rate stipulated in an otherwise genuine intra-group loan, the answer in accordance with the principle of proportionality is to proceed to a correction concerning the fraction of interest charges that is above the usual market rate. It would go beyond the objective of preventing wholly artificial arrangements to refuse all deduction on that interest.

104. On the other hand, where the loan is, in itself, devoid of economic and/or commercial justification and, but for the relationship between the companies and the tax advantage sought, would never have been taken, it is perfectly logical and proportionate to refuse the deduction of the whole interest, not a mere fraction of it. Such a wholly artificial arrangement must, indeed, be ignored by the tax authorities when calculating the corporate tax due. Without the loan, there is no interest to deduct.

105. If tax authorities were to refuse deduction of only a fraction of the interest on the loan in the second scenario, the coherence of the anti-abuse regime would be called into question. Indeed, a part (or even the entire) tax advantage sought through abusive means would end up being granted to the taxpayer, contrary to the objective pursued.

If you are interested you can find the judgment of the Dutch Supreme Court in which it decided to refer this case to the CJEU for a preliminary ruling you can find here.

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)