On December 17, 2021 the OECD released the Global Anti-Base Erosion (GloBE) Model Rules under Pillar Two. The GloBE Model Rules do not directly/automatically apply to multinational enterprises (MNEs), but they have to be implemented by local jurisdictions in order for the rules to apply to MNEs. For the EU this will be done via a two-step implementation process. Step one is an EU Directive, which obliges the EU Member States to implement the (minimum) regulations laid down in a Directive. The second step is then that the EU Member States will have to transpose the regulations laid down in the Directive into their national domestic tax laws.

From the beginning it has been clear that the European Commission wanted to speed up the implementation process. Already on December 22, 2021 the Commission released a Proposal for a Council Directive on ensuring a global minimum level of taxation for multinational groups in the Union.

In its Explanatory Memorandum the Commission a.o. states that the proposal for an EU Directive lays down rules for ensuring a minimum level of effective corporate taxation of large multinational groups and large-scale purely domestic groups operating in the Single Market, which are consistent with the agreement reached by the IF on 8 October 2021, and follow closely the OECD Model Rules agreed by the IF and published on 20 December 2021. Later the Commission adds that the Directive reflects the global OECD agreement, with some necessary adjustments, to guarantee conformity with EU law.

According to the European Commission one of the necessary adjustments to the OECD Model Rules is that in its initial form the proposal for an EU Directive arranges that the minimum taxation rules do not only apply to MNEs but that they also apply to large-scale purely domestic groups operating within the EU. Currently it seems that within the EU discussions are ongoing whether or not the Directive should also apply to large-scale purely domestic groups.

In this article I will focus on the adjustments that will have to be made to the financial accounting net income or loss for excluded dividends to arrive at an entity’s GloBE/qualifying income or loss. More precisely I will focus on the difference in the definitions of excluded dividends as given in the OECD Model Rules and in the proposal for an EU Directive and what consequences the difference in the definition in certain cases might have on the GloBE/qualifying income or loss of an entity and therewith also on the ETR of such entity.

Adjustments to determine the GloBE/qualifying income or loss

Article 3.2.1 of the OECD GloBE Model Rules arranges that a constituent entity’s financial accounting net income or loss is to be adjusted for a.o. excluded dividends (Article 3.2.1, sub b) to arrive at that entity’s GloBE Income or Loss.

The corresponding Paragraph in the Commission’s proposal for an EU Directive is Article 15, Paragraph 2. This paragraph arranges that the financial accounting net income or loss of a constituent entity shall a.o. be adjusted by the amount of excluded dividends (Art 15, Paragraph 2, sub c) to determine the qualifying income or loss of that entity.

Definitions of excluded dividends

So the texts of Article 3.2.1 of the OECD GloBE Model Rules and Article 15, Paragraph 2 of the proposal for an EU Directive are very similar. Under both the OECD Model Rules and the proposal for an EU Directive an adjustment has to be made to an entity’s financial accounting net income or loss (commercial results) to determine that entities GloBE/qualifying income or loss. So the next thing we have to check is whether the OECD GloBE Model Rules and the proposal for an EU Directive use the same definitions of excluded dividends?

Definition as given by the OECD Model Rules

Article 10.1.1 of the OECD Model Rules gives the following definition of excluded dividends: “Excluded Dividends means dividends or other distributions received or accrued in respect of an Ownership Interest, except for:

(a) a Short-term Portfolio Shareholding, and

(b) an Ownership Interest in an Investment Entity that is subject to an election under Article 7.6.”

In this article I will not pay attentions to dividends distributed by investment entities. In other words I will focus on the question when dividends are considered not to qualify as excluded dividends because they fall within the scope of Article 10.1.1, sub a of the OECD Model GloBE Rules. Therefore we need to know what definition the OECD Model Rules give of a short-term portfolio shareholding. The OECD Model Rules come to a definition of a short-term portfolio shareholding via the following 2 steps.

First the OECD Model Rules give the following definition of a portfolio shareholding. According to the OECD GloBE Model Rules a portfolio shareholding is an ownership interests in an entity that are held by the MNE Group and that carry rights to less than 10% of the profits, capital, reserves, or voting rights of that Entity at the date of the distribution or disposition.

Subsequently the OECD Model Rules give the following definition of a short-term portfolio shareholding: a short-term portfolio shareholding means a portfolio shareholding that has been economically held by the constituent entity that receives or accrues the dividends or other distributions for less than one year at the date of the distribution.

So, under the OECD rules a dividend received qualifies as an excluded dividend unless it stems from a shareholding in a subsidiary if:

1. the shareholding represents less than 10% of the ownership in the subsidiary; and

2. the shares have been owned (economic ownership) for less than a year at the date that the dividend is distributed.

Definition as given by the proposed EU Directive

Article 15, Paragraph 1, sub b of the proposed Directive gives the following definition of excluded dividends:

“‘excluded dividend’ means a dividend or another distribution received or accrued in respect of an ownership interest, except a dividend or another distribution received or accrued in respect of:

(i) an ownership interest in an entity of less than 10% (a “portfolio shareholding”) in respect of which a constituent entity is entitled to all or substantially all of the rights to profits, capital or reserves, irrespective of whether the constituent entity owns the legal ownership of such portfolio, for less than one year at the date of the distribution; and

(ii) an ownership interest in an investment entity that is subject to an election pursuant to Article 41.”

Let me first note that I have some problems in understanding how I should read “less than 10%” of sub 1 in relation to the phrase “in respect of which a constituent entity is entitled to all or substantially all of the rights to profits, capital or reserves”.

So, under the OECD rules a dividend received qualifies as an excluded dividend unless it stems from a shareholding in a subsidiary that represents less than 10% of the ownership in the subsidiary.

Difference between the 2 definitions

The most obvious difference between the two definitions is that the OECD GloBE Model Rules contain a ‘safe harbor rule’ which arranges that when the shares over which the dividend is being distributed have been held for a minimum period of 1 year at the date of the distribution, the dividend received also qualifies as an excluded dividend even if at the date that the dividend is distributed the shareholding represents less than 10% of the ownership in the subsidiary. Whereas such ‘safe harbor rule’ is absent in the proposal for an EU Directive.

Another important difference seems to be that under the OECD GloBE Model Rules the economic ownership of the shares is the determining factor to determine whether or not a shareholding is considered to be a short-term portfolio shareholding. Whereas the under the rules laid down in the proposed EU Directive the legal ownership of the shares is the determining factor to determine whether or not a shareholding is considered to be a portfolio shareholding.

An example

A Company is part of A MNE Group. A has a shareholding in non-related entity B. B has issued 10,000 ordinary shares. B has only has 1 class of shares. All issued ordinary shares in B carry an equal right to profit/dividend distributions and capital. Each year on March 31 B distributes a dividend. A is a resident of jurisdiction A and B is a resident of jurisdiction B.

On January 1 of Year 1 A Company has obtained 400 ordinary shares (equaling a 4% shareholding) in B (Shareholding 1). Subsequently on December 1 of Year 1 A Company has obtained another 200 ordinary shares (another 2% of the shares) in B (Shareholding 2). Consequently as of December 1 of Year 1, A Company owns a total of 600 ordinary shares (equaling a 6% shareholding) in B.

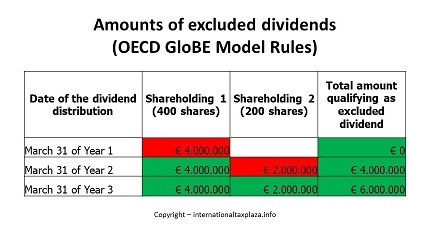

On March 31 of of each year B distributes EUR 10,000 per outstanding ordinary share. This results in A receiving the following dividends.

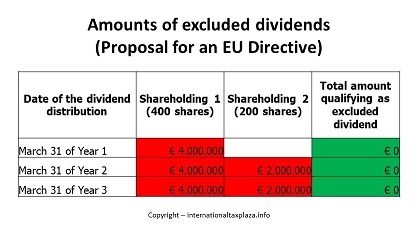

On March 31 of Year 1: EUR 4,000,000;

On March 31 of Year 2: EUR 6,000,000; and

On March 31 of Year 3: EUR 6,000,000.

So let’s have a look how these dividends received would be treated under the OECD GloBE Model Rules and how would be treated under the proposal for an EU Directive when the A group has to determine the GloBE/qualifying income or loss of A Company.

Under the OECD GloBE Model Rules

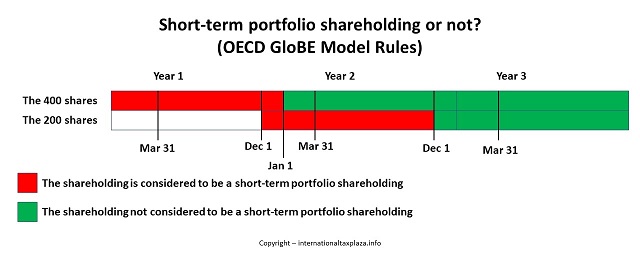

During the whole period the shareholding that A Company has in B stays below 10%. Therefore under the OECD GloBE Model Rules the shareholdings qualify as a portfolio shareholding. However, as we discussed above under the OECD GloBE Model Rules a dividend received on a portfolio shareholding can still qualify as an excluded dividend if the shareholding does not qualify as short-term portfolio shareholding. Therefore under the OECD GloBE Model Rules for both shareholdings it has to be separately determined whether or not the at the date that each of the dividends is distributed the specific shareholding is to be considered to constitute a short-term portfolio shareholding.

Under the OECD GloBE Model Rules the Shareholding 1 is considered to constitute a short-term portfolio shareholding for the period from January 1 until December 31 of Year 1. As of January 1 of Year 2 Shareholding 1 no longer is considered to constitute a short-term portfolio shareholding under the OECD GloBE Model Rules. Consequently for determining the GloBE income or loss of A Company only the dividends distributed March 31 of the Years 2 and 3 qualify as excluded dividends. Whereas the dividend distribution of March 31 of Year 1 does not qualify as an excluded dividend.

Shareholding 2 is considered to constitute a short-term portfolio shareholding for the period from December 1 of Year 1 until November 30 of Year 2. Therefore with respect to Shareholding 2 only the dividend distribution of March 31 of Year 3 qualifies as an excluded dividend distribution for determining the GloBE income or loss of A Company. Whereas the dividend received with respect to Shareholding on March 31 of Year 2 does not qualify as an excluded dividend.

In numbers the aforementioned looks as follows (excluded dividends are marked green):

Under the proposed EU Directive

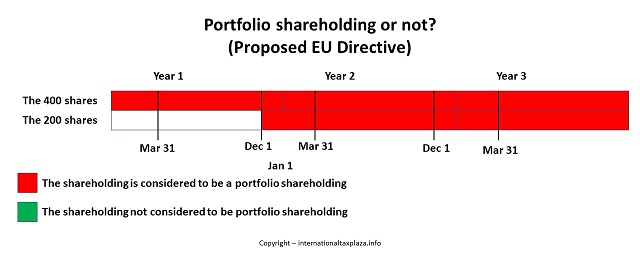

Since for the whole period of the Years 1 through 3 the total shareholdings that A Company has in B has been less than a 10% interest, the shareholding A Company has in B is considered to constitute a portfolio shareholding under rules as laid down in the proposal for an EU Directive for this whole period. Therefore under the proposal for the EU Directive none of the dividend distributions A Company receives on its shareholdings in B qualifies as an excluded dividend under the rules as laid down in the proposal for an EU Directive.

In numbers the aforementioned looks as follows (excluded dividends are marked green):

Conclusion

As follows from the numbers given above for determining the GloBE income or loss of A Company in Year 1 it doesn’t make a difference whether the OECD GloBE Model Rules apply or whether the rules as laid down in the proposal for an EU Directive apply.

However, in Year 2 the GloBE/qualifying income or loss of Company A will be EUR 4 million less if the OECD Model Rules are applied in comparison to what the GloBE/qualifying income or loss will be if the rules as laid down in the proposal for an EU Directive have to be applied.

In Year 3 the GloBE/qualifying income or loss of Company A will even be EUR 6 million less if the OECD Model Rules are applied in comparison to what the GloBE/qualifying income or loss will be if the rules as laid down in the proposal for an EU Directive have to be applied.

Depending on other circumstances (Are the dividends taxed at the level of A company under the national laws of jurisdiction A and if so against what rate? Did jurisdiction B withhold dividend withholding taxes over the distributed dividends and if so against what rate?) the fact that under one set of rules the dividends qualify as excluded dividends where they don’t under the other set of rules might also have an impact on the ETR of A Company and therefore ultimately also on whether or not a Top-up Tax might be due.

The abovementioned example shows that only studying the OECD GloBE Model Rules is not enough. One should all the time also review how the different jurisdictions will traspose/have transposed these OECD GloBE Rules into its domestic tax laws.

Copyright – internationaltaxplaza.info

and

Follow International Tax Plaza on Twitter (@IntTaxPlaza)