On November 14, 2023 on the website of the Dutch tax authorities a position paper of their Knowledge Group special profit provisions for corporate income tax purposes has been published regarding the carrying-back of losses for Dutch corporate income tax purposes (KG:011:2023:14). In this position paper the Knowledge Group answered the question whether the carry-back of a 2022 loss to 2021 is subject to the temporization measure of Article 20, Paragraph 2 of the Dutch corporate income tax Act (hereafter: DCIT Act) as that provision reads as of January 1, 2022. The Knowledge Group also answered the question what the consequences are if the carry-back of the 2022 loss takes place against the remaining 2021 profit takes place after previously already a loss from a financial year prior to 2021 was carried forward to 2021.

The cause

The Knowledge Group received a question about the carrying-back of a 2022 loss against a 2021 profit and the applicability of the temporization measure of Article 20, Paragraph 2 second sentence, of the DCIT Act as it reads as of January 1, 2022.

Questions

- Is the carry-back settlement of a loss from 2022 with a profit from 2021 subject to the temporization rule as laid down in Article 20, Paragraph 2 second sentence, of the DCIT Act as it reads as of January 1, 2022? and, if so;

- How does the loss temporization measure work out if a loss stemming from an older year from was first carried-forward to 2021?

Legal context

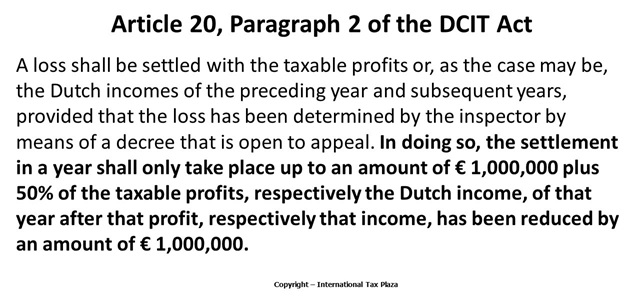

The so-called temporization measure was introduced under the tax plan 2021. Under this tax plan the text of Article 20, Paragraph 2 of the DCIT Act was amended as per Januari 1, 2022. As of January 1, 2022 Article 20, Paragraph 2 of the DCIT Act reads as follows:

“2. A loss shall be settled with the taxable profits or, as the case may be, the Dutch incomes of the preceding year and subsequent years, provided that the loss has been determined by the inspector by means of a decree that is open to appeal. In doing so, the settlement in a year shall only take place up to an amount of € 1,000,000 plus 50% of the taxable profits, respectively the Dutch income, of that year after that profit, respectively that income, has been reduced by an amount of € 1,000,000.”

Until January 1, 2022 Article 20, Paragraph 2 of the DCIT Act read as follows:

“2. A loss shall be settled with the taxable profits, respectively the Dutch incomes, of the preceding year and the six following years, provided that the loss has been determined by the inspector by a decree that open to appeal."

A comparison of the texts of the provision shows that the loss settlement is not only being temporized, but also that the carry-forward period is no longer limited in time.

In the tax plan 2021 the following is noted with respect to the entering into force:

“The new regulations enter into force at a time to be determined by Royal Decree, with the understanding that it may also be determined that the changes regarding the loss carry-forward, in deviation from the text of the DCIT Act as applicable until December 31, 2021, apply to losses suffered in financial years starting on or after January 1, 2013 , insofar as these losses are being settled with taxable profits or Dutch incomes realized in financial years starting on or after January 1, 2022.”

In the Royal Decree of May 21, 2021 the following was included with respect to the entering into force:

“The new text of Article 20, Paragraph 2 of the DCIT Act comes into effect on January 1, 2022 and will apply for the first time to financial years commencing on or after January 1, 2022, with the understanding that the changes regarding the loss carry-forward, in deviation from the text of the DCIT Act as applicable until December 31, 2021, apply to losses that have been incurred in financial years starting on or after January 1, 2013, to the extent that these losses are being settled with taxable profits, or Dutch incomes, realized in financial years starting on or after January 1, 2022. (...)”

Answers

- The entitlement to settle losses is governed by the legal text that applies to the (financial) year in which the loss was incurred. The carry-back settlement of a 2022 loss against a 2021 profit is subject to the temporization measure as laid in Article 20, Paragraph 2 of the DCIT Act as it applies as of January 1, 2022.

- The temporization measure does not apply to the carry-forward settlement of losses stemming from before 2021 with 2021 profits. If after this settlement still an unsettled part of the 2021 profit remains, a loss from 2022 can be settled with it. The temporization measure does apply to this carry-back loss settlement. The amount of the taxable profit for 2021 that is eligible for settlement (the so-called "loss settlement space") is partly limited by the carry-forward settlement of losses from before 2021 with the profit for 2021 that previously took place.

From the considerations of the tax authorities

Question 1

With respect to the fist question the Knowledge Group concludes that from the legal text, the legal system and the parliamentary history it follows that the right to a loss settlement is governed by the legal text that is into force in the year in which the loss is incurred. Therefore, the carry-back of a loss from 2022 with the profit from 2021 is subject to the temporization measure that was introduced with effect from 2022.

Question 2

With respect to the second question the Knowledge Group has the following numerical example in its position paper:

|

Result/loss from 2020 |

- € 1.300.000 |

|

Result/taxable profit from 2021 |

€ 4.000.000 |

|

Result/loss from 2022 |

- € 5.500.000 |

First, the loss from 2020 will be forwarded. This loss carry-forward is not limited by the temporization measure. This for the example means that the 2020 loss of € 1.3 Mio can be fully offset against the 2021 profit of € 4 Mio. After loss settlement, a profit of € 2.7 Mio remains for 2021.

Subsequently the 2022 loss will be settled with the remaining profit of 2021. As explained above, the temporization measure does apply to this loss carry-back. In position paper KG:011:2022:3 the Knowledge Group explained that the settlement capacity must be determined once, i.e. per financial year. This means that the settlement capacity for 2021 is partly limited by the previous settlement of the 2020 loss.

The calculation goes as follows:

1 Available 2021 loss settlement capacity: € 2.500.000 (= € 1.000.000 + 50% of (€ 4.000.000 - € 1.000.000));

2 Settlement of the 2021 loss (€ 1.300.000);

3 2021 loss settlement capacity remaining after the settlement of the 2020 loss: € 1.200.000 (= € 2.500.000 – € 1.300.000);

4 Partial settlement of the 2022 loss with the 2021 profit;

5 Remaining profit for 2021 over which Dutch corporate income tax is due: € 1.500.000 (= € 4.000.000 - € 1.300.000 - € 1.200.000);

6 Remaining loss of 2022 that can be carried forward to future years: € 4.300.000 (= € 5.500.000 - € 1.200.000).

Remarks ITP

Under the loss settlement rules as they apply as of January 1, 2022 losses can still be carried back and carried forward. However, unlike before 2022 the settlement of a loss with the profits of a previous year or with the profits of later years can no longer lead to no Dutch corporate income tax being due over a financial year in which the taxpayer realized a taxable profit. It should however be noted that this doesn’t mean that losses cannot fully be settled with profits realized in other financial years. Depending on the loss incurred and the profits realized in other financial years it might only take a taxpayer longer to fully settle the losses that it incurred in a financial year because it might take the profits of more financial years to be able to fully settle the losses.

The full Dutch version of the position paper containing an extensive assessment can be found here.

Other position papers Dutch corporate income tax that we have reported on earlier can be found here.

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)