On December 21, 2023 on the website of the Dutch tax authorities a position paper of the Knowledge Group international tax law, corporate income tax and profits of the Dutch tax authorities was published (KG:040:2023:9). In this position paper the Knowledge Group answers the question at which moment a discontinuation loss incurred with respect to a permanent establishment can be taken into account for Dutch corporate income tax/Dutch individual income tax purposes, if in the financial year of discontinuation it has not yet been established that no compensation has been granted by the pe-state for the net tax loss incurred in that state.

Facts

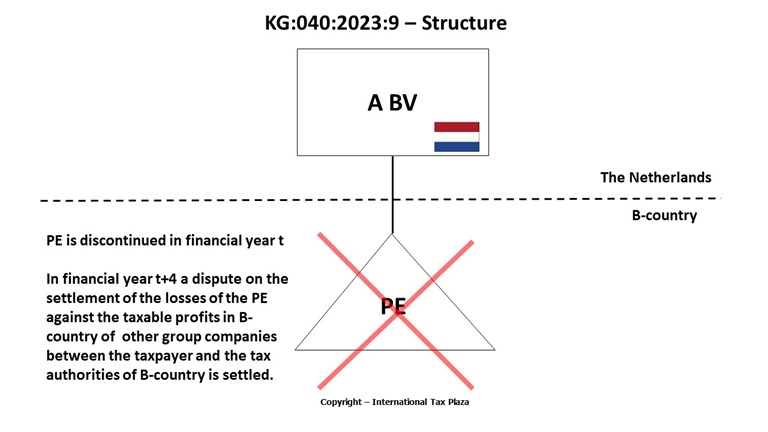

A BV is a resident of the Netherlands and part of the A-group. A BV has a permanent establishment (Hereinafter: PE) in B-country. The object exemption for Dutch tax purposes applies to the results realized through the PE. In year t, activities in B-country are discontinued and A BV ceases to realize profits in B-country. A BV has suffered a net loss of € 1,000 from B country. In year t A BV wishes to take a discontinuation loss into account with respect to this net loss of the aforementioned € 1,000.

From year t onwards the A-group and the tax authorities of B-country are disputing to which extent the losses incurred by the PE in B country can be offset against profits of group companies of A BV that are residents of B country. In year t+4, the dispute is settled and an amount of € 200 is offset against the profits of group companies. As a result thereof, A BV adjusts the discontinuation loss to € 800 (= € 1,000 -/- € 800).

After year t, A BV has not realized any further (negative) profits from B country. The other conditions of Article 15i of the Dutch corporate income tax Act (hereinafter: the DCIT Act) have been met.

Question

Is the discontinuation loss of € 800 deductible in the year financial year t or in the financial year t+4?

Answer

Pursuant to Article 15i, Paragraph 5, opening words of DCIT Act the discontinuation loss is to be deducted at the moment at which A BV ceases to realize profits in the other state. In the underlying case that moment is in the financial year t.

The burden of proof that and up to what amount a discontinuation loss can be taken into account rests on A BV. The fact that A BV only manages to provide that proof in year t+4 does not influence the moment at which the discontinuation loss is deductible.

From the legal assessment of the tax authorities

Pursuant to Article 15i, Paragraph 5, opening words of the DCIT Act the discontinuation loss is deductible “at the time when the taxpayer ceases to realize profits from the other state”.

Pursuant to Article 15i, Paragraph 2 of the DCIT Act a discontinuation loss exists if the balance of the amounts that are taken into account as profit/loss from the other state under the object exemption results is a negative amount, insofar as no tax relief of any kind has been granted in that other state regarding this negative balance.

If such a tax relief has been granted (in the other state), the negative balance does not qualify as a 'discontinuation loss' in so far as a tax relief was granted by the other state.

The burden of proof that and for which amount a discontinuation loss can be taken into account rests on the taxpayer. The taxpayer will have to convincingly demonstrate the amount, since under Article 15i, Paragraph 5, under c of the DCIT Act a discontinuation loss is only taken into account if the taxpayer demonstrates the amount of the loss.

In the underlying case A BV therefore (among others) has to demonstrate that the other state did not grant a tax relief as meant in Article 15, Paragraph 2 of the DCIT Act with respect to the amount for which a deductible discontinuation loss was claimed.

The fact that A BV only manages to provide that proof in financial year t+4 does not affect the fact that the discontinuation loss will be deductible at the moment at A BV ceases to realize profits in the other state. In the underlying case that moment is in financial year t.

(Remark ITP: Where above the tax authorities use the phrase ‘ceases to realize profits’ it refers to both positive profits as well as negative profits/losses for tax purposes)

Other position papers of the Knowledge Group international tax law, corporate income tax and profits that we already discussed can be found here.

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)