On the website of the European Parliament’s Special Committee on Tax Rulings and Other Measures Similar in Nature or Effect (TAXE 2) a Draft version of a report on tax rulings and other measures similar in nature or effect (2016/2038(INI)) from May 11, 2016 has been made available. The report contains a motion for a European Parliament resolution and was drafted by the co-rapporteurs Jeppe Kofod and Michael Theurer. For me especially conclusion/recommendation 17 of the motion for a European Parliament resolution gives rise to some questions.

Conclusion/recommendation 17 of the report reads as follows:

“Notes that until now, patent, knowledge and R&D boxes have not proven effective in fostering innovation in the Union, but are, rather, used by MNEs for profit-shifting through aggressive tax planning schemes, such as the well-known ‘double Irish with a Dutch sandwich’; considers that patent boxes are an ill-suited tool for achieving economic objectives; insists that R&D can be promoted through subsidies which should be given preference over patent boxes, as subsidies are less at risk of being abused by tax avoidance schemes; observes that the link between patent boxes and R&D activities is often arbitrary and that current models lead to a race to the bottom with regard to the effective tax contribution of MNEs;”.

(NB the selection was marked in bold by International Tax Plaza, because it's this part of the conclusion/recommendation that I will discuss below)

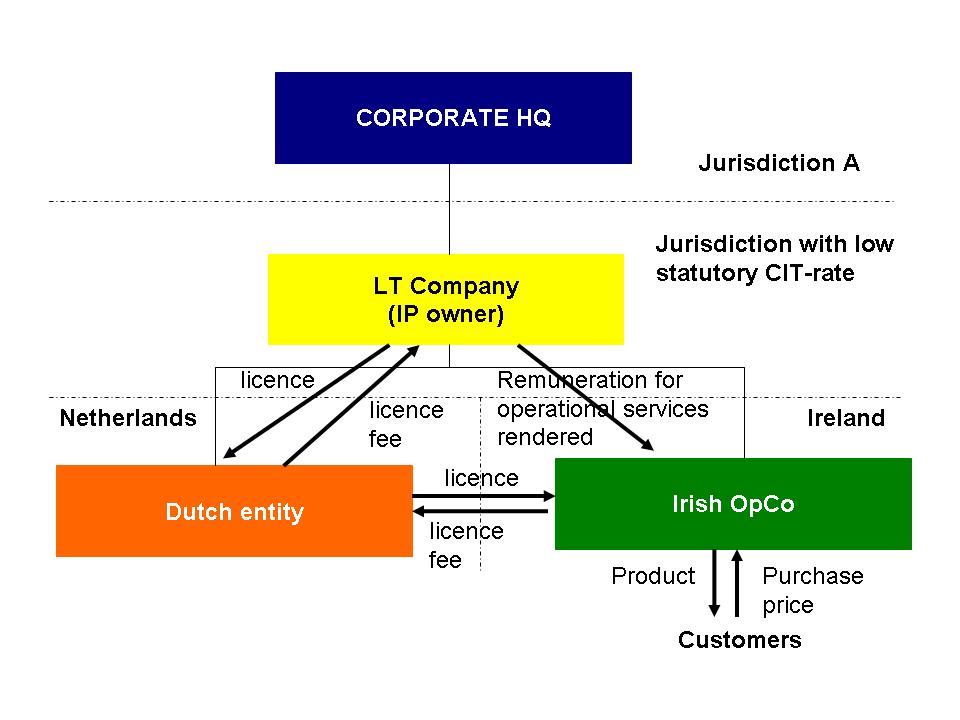

Patent/innovation boxes certainly can be helpful for optimizing a group’s effective tax rate. But what surprises me is that the co-rapporteurs link the use of patent/innovation boxes to the so-called double Irish with a Dutch sandwich structure. For as far as I understand, in the standard double Irish with a Dutch sandwich, the (non-US) IP (Hereafter: the IP) was developed on behalf of and for the risk of a company that has been incorporated under Irish law and that after its incorporation has moved its residence to a low taxed jurisdiction (Hereafter: LT Company). Therefore LT Company possesses the economic and juridical ownership of the IP. Assuming that ultimately large part of the net income realized through the IP is allocated to LT Company, and since LT Company is only subjected to corporate income in its ‘new’ country of residence, this net income is taxed against the rate of this low taxed jurisdiction.

For me that raises the question where the co-rapporteurs see an added value of using a patent box scheme in such so-called double Irish with a Dutch sandwich structure. The Irish operational company (Hereafter: OpCo), which is a second Irish entity, might also have royalty income. However, since it had to obtain a (sub-)licence it also incurs expenses regarding the sub-licence it obtained. So the net royalty income realized by OpCo is not that substantial. Furthermore it should be noted that since the Irish knowledge and development box was only introduced in 2016, this scheme was not available when the double Irish with a Dutch sandwich structures were set up.

So what about the Dutch entity? Like OpCo, the Dutch entity will have income from licence fees (paid by OpCo). At the same time the Dutch entity will have to pay licence fees to LT Company. These costs will lower the net royalty income allocated to the Dutch entity. Furthermore, the royalty income the Dutch entity realizes via the double Irish with a Dutch sandwich structure does not meet the conditions of the Dutch innovation box scheme. Therefore the scheme cannot be applied to the income realized by the Dutch entity.

In my view one either opted to use the double Irish with a Dutch sandwich structure or one opted to use a patent/innovation box scheme. In the latter case one had to arrange that the IP was developed on behalf and for the risk of another group entity than LT Company. Obviously this entity should then be an entity that is a resident of a country which has/had a patent/innovation box scheme. Therefore I would rather qualify the double Irish with a Dutch sandwich structure and the patent/innovation box schemes as ‘competitors’, instead of as tools that were to be used supplementary to each other (with respect to the same IP).

But what worries me even more is that the co-rapporteurs call the structure the “well-known ‘double Irish with a Dutch sandwich’”. That is what surprises me most. I would expect that by now the members of TAXE and TAXE 2 would have taken a so close look at the structure, that the structure would no longer have any secrets for them. Still, based on the motion for a European Parliament resolution as included in the Draft report, it seems that more than a year after the initial TAXE Committee has been established the co-rapporteurs of TAXE 2 have not yet been able to understand the basic principles of what they themselves call a well-known structure.

More generally it makes me wonder how much effort the members of TAXE and TAXE 2 have put in really trying to get an understanding of structures they have labeled as aggressive tax planning structures. And perhaps even more important and more in general: How well do the members of TAXE 2 understand the principles of the structures they talk about and the way such structures are implemented by tax advisors and in-house tax teams?

Click here to be forwarded to the Draft report of the co-rapporteurs Jeppe Kofod and Michael Theurer, as available on the website of TAXE 2, which will open in a new window.

Copyright – internationaltaxplaza.info

Are you looking for a motivated newcolleague? Then place your job ad on International Tax Plaza!

and

Stay informed: Subscribe to International Tax Plaza’s Newsletter! It’s completely FREE OF CHARGE!