On October 29, 2021, we already reported on the judgment of the Court of Justice of the EU (CJEU) in Case C-324/20, X-Beteiligungsgesellschaft (TVA – Paiements successifs). The case regards the interpretation of the Articles 64 Paragraph 1 and 90 Paragraph 1 of Council Directive 2006/112/EC of 28 November 2006 on the common system of value added tax. This judgment and the way how the CJEU interprets Articles 64 Paragraph 1 and 90 Paragraph 1 of Council Directive 2006/112/EC can cause serious cashflow issues in case of a one-time supply of services, which are remunerated by means of payment in installments.

In 2012, X supplied mediation services to T-GmbH for the purposes of the latter’s sale of a plot of land to another. It is clear from the fee agreement which X and T entered into on 7 November 2012 that X had already complied with its contractual obligations by that date. As regards the remuneration for the services in question, a fee of EUR 1,000,000 plus VAT was agreed and it was specified that that fee was to be paid in five annual installments of EUR 200,000 plus VAT payable on June 30, 2013. At the time of the respective due dates, X issued an invoice for each installment and paid tax corresponding to the sum received.

X and the German tax authorities were disputing the moment of chargeability of the VAT. X is of the opinion that a pro-rate part of the VAT becomes chargeable every time that an invoice for an annual installment is issued. Whereas the German tax authorities are of the opinion that the services had been supplied in 2012 and that therefore X should have paid, in respect of that year, VAT on the entire fee.

In the underlying case the CJEU has judged that VAT is to become chargeable when the goods or services are supplied, that is, when the transaction in question takes place, regardless of whether the consideration due for that transaction has already been paid. Accordingly, VAT is due to the tax authorities by the supplier of goods or services, even where he or she has not yet received from his or her client the payment relating to the transaction carried out. The CJEU also ruled that Article 90, Paragraph 1 of Directive 2006/112 must be interpreted as meaning that, in the case of an agreement on payment in instalments, the fact that an instalment of the remuneration has not been paid before its term cannot be regarded as non-payment of the price, within the meaning of that provision, and, as a result, cannot lead to a reduction of the taxable amount. Consequently taxable persons may ultimately pre-finance the VAT which they are required pay to the State when supplying one-time services for which the price is paid in instalments.

Conclusion

So based on the judgment of the CJEU taxable persons making a one-time supply of services, for which they are remunerated by means of payment in instalments may ultimately pre-finance the VAT which they are required pay to the State. For X this means the following;

· X made a one-time supply of services in 2012;

· The total remuneration amounted to EUR 1 mio excl VAT;

· The total remuneration is due in 5 equal annual installments of EUR 200k excl, VAT;

· The first annual installment is due on June 30, 2013;

· The last annual installment is due on June 30, 2017;

· The VAT rate is 19%;

· According to the CJEU judgment X has to remit the full amount of VAT (EUR 190k) to the German tax authorities in the year 2012;

So, what does the aforementioned means for the cash-flow position of X?

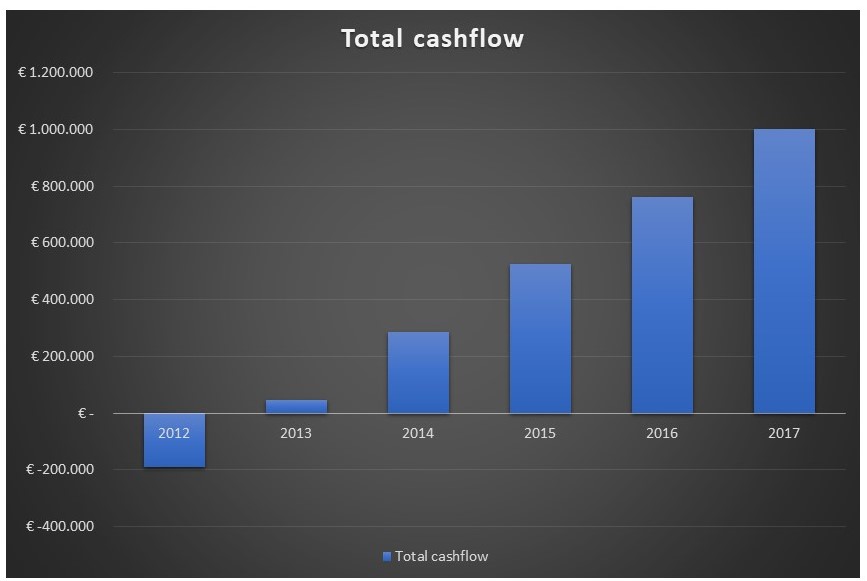

In 2012 X will not receive any payment from its client/customer. It will however have to remit EUR 190,000 of VAT to the German tax authorities. From 2013 until 2017 X will each year receive an installment of EUR 238,000 (EUR 200,000 + 19% VAT) from its client/customer. Therefore, the total cashflow that X will have over the years from this ‘project’ will look as follows:

Consequently until June 30, 2013, X will be pre-financing an amount of EUR 190,000 of VAT. As of June 30,2013, the net cashflow that X has realized will only amount to EUR 48,000 and not to the EUR 200,000 that X anticipated. And as of June 30, 2014, the net cashflow X realized will “only” amount to EUR 286,000 and not to the EUR 400,000 that X anticipated. Etc.

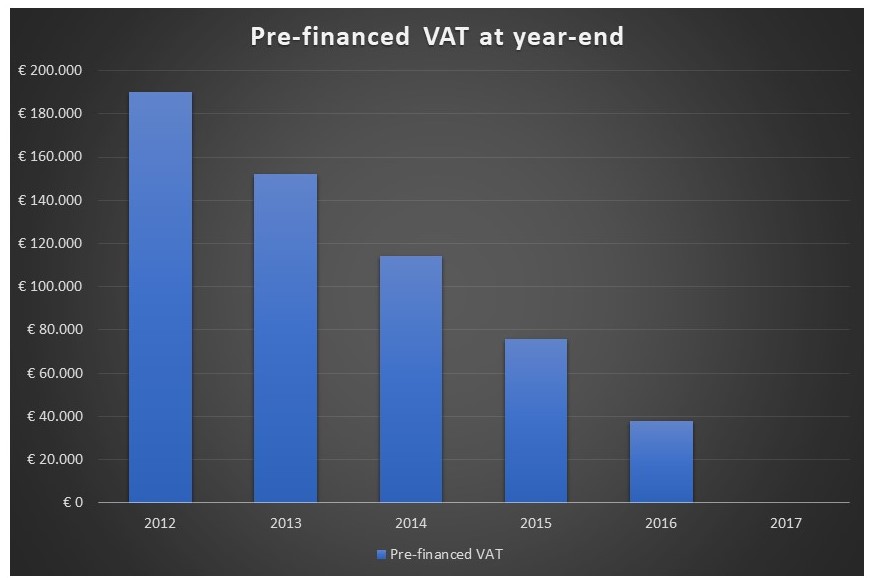

The amount of VAT that X is prefinancing will decrease with EUR 38,000 per year. The chart below shows the amount of VAT that X is pre-financing per December 30 of each respective year.

Copyright – internationaltaxplaza.info