On September 30, 2021, on the website of the Dutch courts (De Rechtspraak) the judgment of the Court of Appeal of The Hague in Case number: BK-19/00759, ECLI:NL:GHDHA:2021:1714 was published. In the underlying case the taxpayer and the tax authorities are disputing whether or not the taxpayer is entitled to take a liquidation loss into account with respect to the liquidation of 2 of its (indirect) Irish subsidiaries.

Introduction

As most of our readers might know, the Dutch corporate income tax contains a participation exemption. The participation exemption arranges that profits stemming from a qualifying participation are exempt for Dutch corporate income taxes. At the same time costs/losses incurred with respect to a qualifying participation in principle are not deductible for Dutch corporate income tax purposes. Exception to this general principle are so-called liquidation losses. The provisions regarding liquidations losses are laid down in Articles 13d and 13e of the Dutch corporate income tax Act.

Facts of the underlying case

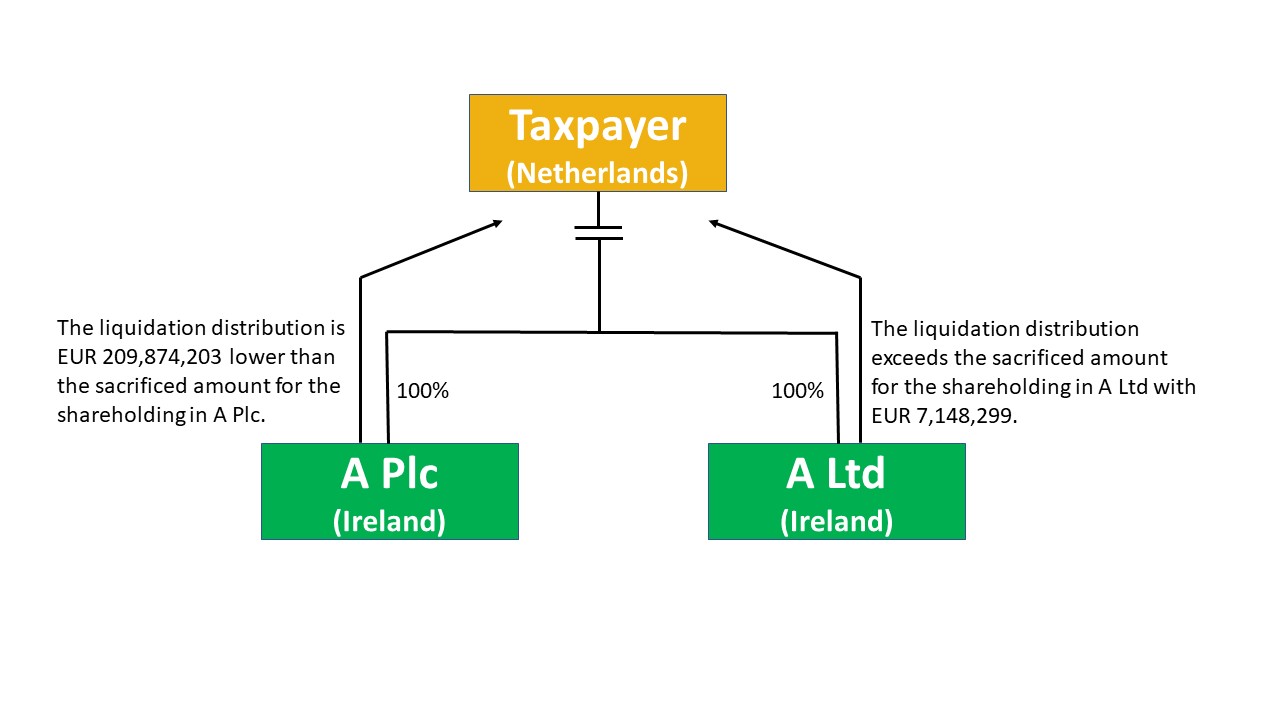

The Dutch taxpayer a.o. indirectly holds all the shares in A Plc and A Ltd, both incorporated under Irish law and both residents of Ireland. In Ireland A Plc and A Ltd both used the US dollar (USD) as their functional currency for commercial and for tax purposes.

On February 17, 2009, the taxpayer announced by means of a press release that it had taken the decision to as a group shift the focus from products generating a 'spread' ('spread-based') to services for which a fee is paid ('fee-based'). In that regard on March 28, 2012, it was decided to dissolve and liquidate A Plc. This liquidation took place on March 22, 2013, and the deregistration from the Irish Chamber of Commerce took place on June 28, 2013. A Ltd has also been liquidated.

The sacrificed amount for A Plc exceeds the total of the liquidation distributions made by A Plc with EUR 209,874,203. The total of the liquidation distributions made by A Ltd exceeds the sacrificed amount for that company by EUR 7,148,299. In view of the interconnectedness of the activities of both of these companies, for the purposes of the liquidation loss scheme of Article 13d of the Dutch Corporate Income Tax Act (text 2013) the loss of A Plc and the profit of A Ltd are considered in conjunction. Resulting in a (total) liquidation loss of EUR 202,687,308.

A Plc has made use of the Irish group relief scheme. Under this scheme, certain losses incurred within a financial year can be transferred to another group company that was profitable in the same year. It is not possible to offset losses against profits of other group companies from other years. Nor is it possible to offset losses incurred in the year of liquidation against profits realized by other companies after the liquidation. Under Irish tax law, any losses which are unused at the time of liquidation are permanently lost.

During A Plc's existence an amount of at least EUR 115,592,673 in losses has been transferred from A Plc to other Irish group companies under the group relief scheme. However, the group relief scheme has not been optimally used. At least an amount of USD 873,000 (EUR 649,340) in losses has not been transferred to group companies, although the possibility to transfer these losses under the group relief scheme existed.

According to the taxpayer, at the time of its dissolution, A Plc still had for an amount of EUR 109,981,275 available in unsettled losses. With regard to these losses, the Irish Revenue has stated the following:

“I confirm that [A Plc] (…) has unutilized trading losses carried forward of € 109,981,275 which appears on the CT1 filed for period 01/03/2012 to 28/03/2012 (Please see copy of CT return attached for reference).

(e-mail from the Irish Revenue addressed to the tax advisor of A Plc dated November 14, 2017);

“I confirm that [A Plc] (…) has unutilized trading losses carried forward of € 109,981,275 (…). I also confirm that these trading losses were not utilized in the subsequent CT returns filed for periods with years ending 22/03/2013 and 22/03/2014. These losses could not have been used after the date the company was finally dissolved at the end of the liquidation by any other Irish tax resident company in the [A] group or by the company itself as it continued to no longer be in existence.”

(e-mail from the Irish Revenue addressed to the tax advisor of A Plc dated January 9, 2018).

When issuing the 2013 Dutch corporate income tax assessment the Dutch tax authorities did not allow the taxpayer to take a liquidation loss into account. In its judgment in first instance the District Court of The Hague allowed the taxpayer to take a liquidation loss of EUR 202,687,308 into account. In the underlying judgment the Court of Appeal from The Hague judges on the appeal that the Tax Inspector filed against aforementioned judgment of the District Court.

The dispute

The taxpayer and the tax authorities are disputing whether the application of the Irish group relief scheme referred to above precludes the taxpayer from taking into account a liquidation loss of EUR 202,687,308 regarding the liquidations of its subsidiaries A Plc and A Ltd.

If the aforementioned question is answered in the affirmative, alternatively parties are disputing whether under EU law the taxpayer may charge the unsettled loss of A Plc to its (Dutch) taxable profit. If this question is answered in the affirmative, the amount of this loss is disputed.

The Tax Inspector argues that the Lower Court's judgment should be set aside, and the taxpayer argues that the Lower Court’s is to be confirmed.

From the considerations of the Court

5.1. On appeal, the Inspector took the position that the literal text of Article 13d, paragraph 9, opening sentence and sub a of the DCIT Act, leaves room for both a limited and a broad interpretation of this provision. According to the Tax Inspector however, in view of its anti-abuse nature a broad explanation should prevail. Moreover, a broad interpretation does justice to the purpose of this provision within the liquidation loss scheme: the prevention of double settlement of losses. From the parliamentary history the Tax Inspector deduces that it is not the legislator's intention to provide compensation for a loss that has already been or could be settled elsewhere. This is moreover in line with the purpose and intent of the participation exemption and with the provisions of paragraphs 4 and 8 of the aforementioned Article, which prevent losses already utilized from being deducted again. The Inspector also refers to the parliamentary discussion of the arrangement made for cessation losses of a permanent establishment when the object exemption was introduced (Article 15i DCIT Act); According to the Tax Inspector this parliamentary discussion shows that the legislator considers a loss settlement that took place in the past to constitute an obstacle for being allowed to take a cessation loss into account. In view of the analogy between the cessation loss scheme in the object exemption, and the liquidation loss scheme in the participation exemption, according to the Tax Inspector this legislative history is also relevant for the interpretation of the underlying provision (Article 13d, paragraph 9 of the DCIT Act).

5.2. The Court of Appeal does not follow the Tax Inspector in his argument here for it considers the following.

5.3. The text of Article 13d, paragraph 9, letter a, of the DCIT Act may leave some room for doubt as to when to assess whether the non-availability requirement has been met. Since the underlying provision has the character of an anti-abuse provision, the interpretation of this provision must therefore be tailored as closely as possible to the improper use that the legislator has sought to combat and in the manner the legislator envisaged in doing so (according to the Dutch Supreme Court June 7, 2019, ECLI:NL:HR:2019:886, BNB 2019/117, consideration 2.4.2).

5.4.1. The text of Article 13d, paragraph 9, opening sentence and sub a, DCIT Act (no entitlement “exists” and losses that “have remained unsettled” in sub a, as well as the opening sentence of paragraph 9: “the liquidation loss is only taken into account at the time the liquidation has been completed") points in the direction of the interpretation of the underlying provision as advocated by the taxpayer. In that case, the condition that “no entitlement to any compensation exists” must be assessed according to the situation at the time of liquidation. The aforementioned leads to the conclusion that a deduction of a liquidation loss can only be refused if any right to any sort of compensation for losses that have not yet been settled exists at the moment that the liquidation of the dissolved company is completed.

5.4.2. However, the Tax Inspector argues, that the text of the provision supports his position that the transfer of losses to another group company under the group relief scheme entails that these losses have "remained unsettled" at the (level of the) transferring company within the meaning of Article 13d, paragraph 9, letter a DCIT Act. Furthermore, no entitlement to “any compensation for tax purposes” may exist regarding such losses. Which, according to the Tax Inspector, according to the word “exists” does not only relate to the period after completion of the liquidation, but to the entire period of existence of the dissolved entity up to and including the moment of completion of the liquidation. Contrary to the Tax Inspector's view, the Court of Appeal is of the opinion that a settlement of losses at another group company should be regarded as a settlement of those losses as meant in Article 13d, paragraph 9, letter a DCIT Act. Regarding loss transfers in the past, it therefore applies that those losses have not remained unsettled, so that the explanation as advocated by the Tax Inspector cannot be reconciled with the text of the law.

5.5. The explanation of the text of the law as referred to above in 5.4.1 is in line with the system of the liquidation loss scheme, which in a general sense relates to the situation at the time when it is established that the loss settlement options at the level liquidated participation have been lost forever (according to the aforementioned judgment Dutch Supreme Court BNB 2019/117). Moreover, according to the system of the liquidation loss scheme, no numerical equality exists between the losses that are lost at the level of the subsidiary and the liquidation loss that can be taken into account by the parent company. Due to practical objections, the legislator has deliberately opted for a fairly crude and lump-sum system in which the link between the result of the participation and the liquidation loss has been abandoned (see also the judgment of the Dutch Supreme Court of November 3, 1993, ECLI:NL:HR:1993:BH8486, BNB 1994/11, consideration 3.3). This system has remained unchanged after the introduction of the underlying provision (see Parliamentary Papers II 1987/88, 19 968, no. 7, p. 22).

5.6. Like the District Court, the Court of Appeal further takes into account that no clear indications that the legislator intended a broader application can be found in the legislative history. From the article-by-article explanation of article 13d, paragraph 9 it appears that the provision aims to exclude specific situations of potential double loss set-off that are considered undesirable from the application of the liquidation loss scheme, i.e. situations in which losses can be passed on to the continuator of the enterprise or situation in which losses remain available to the parent company. This therefore concerns cases of compensation for losses that still exist at the level of the subsidiary at the moment of liquidation (see Parliamentary Papers II 1986/87, 19 968, no. 3, p. 12 and 13). Although the background to the introduction of the condition that no entitlement to any kind of loss compensation exists is to prevent double loss settlement, the legislator has not reconsidered the system, as described above in 5.5, that there is no relation between the loss incurred by the participation and the liquidation loss to be taken into account pursuant to Article 13d of the DCIT Act. Therefore, consciously the possibility was accepted that losses are deducted twice (as well as the possibility that losses are not fully deducted). Against this background, the rationale of the liquidation loss scheme and of the anti-abuse rule of Article 13d, paragraph 9, first sentence and sub a of the DCIT Act in particular, does not require that the liquidation loss is to be waived at the level of the Dutch parent company if the subsidiary has transferred losses prior to its liquidation.

5.7. In the context of the purpose and purport of 13d, paragraph 9, first sentence and sub a of the DCIT Act the Inspector has furthermore referred to the intermediate holding provision of Article 13d, paragraph 4 of the DCIT Act and the manner on which the sacrificed amount is determined after separation from a fiscal unity as laid down in Article 13d, paragraph 8 of the DCIT Act. The regulations as laid down in the provisions of those paragraphs of Article 13d DCIT Act cannot convince the Court of Appeal of the correctness of the interpretation of the provisions of paragraph 9, first sentence and sub a as proposed by the Inspector. In the provisions of the fourth and eighth paragraphs, for two specific situations the legislator has chosen to deviate from the system as described above in 5.5 in there is no connection between the loss suffered by the participation and the liquidation loss to be taken by the parent company. Although with the introduction of the underlying provision, the legislator also intended to prevent forms of double loss compensation, it however did not replace the rather crude and lump-sum scheme by a system in which the liquidation loss to be taken by the parent company is reconciled with the amount of losses that has not been and no longer can be compensated in any way by the participation.

5.8. Finally, the Inspector also referred to the cessation loss regulation as laid down in Article 15i of the DCIT Act. The Court notes in the first place that in the text of that provision, unlike in the underlying provision, a clear distinction is made between loss settlement prior to the cessation (paragraph 2) and the possibility that losses can still be settled after the cessation (paragraph 3). Furthermore, a cessation loss is the amount of losses that is actually incurred by the foreign enterprise (the negative balance of the positive and negative amounts of foreign profits to which the object exemption applies), while for the liquidation loss scheme not necessarily a link exists between the liquidation loss and the result of the participation (see 5.5 above). Finally, the Court of Appeal considers the legislative history of the posterior Article 15i DCIT Act to be irrelevant for the interpretation of the anterior Article 13d DCIT Act. Therefore, no reason exists to take the text and rationale of Article 15i DCIT Act into account when interpreting Article 13d of the DCIT Act.

Based on the above the Court of Appeal confirms the previous judgment of the District Court. Consequently, the taxpayer is allowed to take into account a liquidation loss of EUR 202,687,308 in the year 2013.

The full text of the judgement of the Court of Appeal in the underlying (only available in the Dutch language) can be found here.

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)