On March 3, 2022, on the website of the Court of Justice of the European Union (CJEU) the opinion of Advocate General Pitruzzella in Case C-98/21, Finanzamt R versus W-GmbH (ECLI:EU:C:2022:160), was published.

The dispute in the main proceedings and the questions referred for a preliminary ruling

Facts

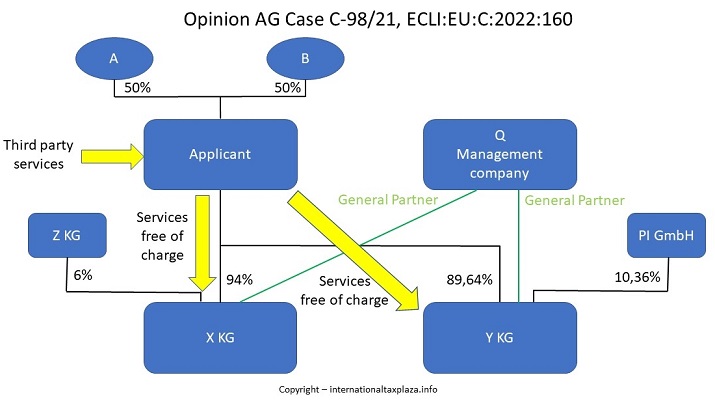

The applicant carries out the purchase, management and re-utilisation of its own property, as well as project planning, renovation, and preparation of building projects of all different types. Its shareholders in 2013, the year under dispute, were A and B, each with a stake of 50% (simultaneously sole managers).

The applicant held a stake in the limited partnerships under German law, X-KG and Y-KG, as a limited partner. Both companies built properties and sold the individual dwelling units predominantly free of value added tax (VAT).

During the year under dispute, stakes in X-KG were held by Q, the management company with limited liability under German law (Q Verwaltungs-GmbH) as the general partner, and by the applicant (with 94% of the shares) and Z, the limited partnership under German law (Z-KG) (with 6% of the shares) as limited partners. The applicant’s investment was EUR 940, and that of Z-KG was EUR 60. Q Verwaltungs-GmbH was not required to make any investment and does not have any capital share; it does not share in any profit or loss and does not possess any voting rights. The managing directors of Q Verwaltungs-GmbH are B and C. Neither A nor B nor closely associated persons hold a stake in Z-KG.

On January 31, 2013, it was agreed that Z-KG would pay a premium of EUR 600 000 as a shareholder contribution and that the applicant would provide services free of charge worth at least EUR 9.4 million for two building projects of X-KG. The applicant provided these services partly with its own personnel and its own machinery, and partly with assistance from other companies.

Furthermore, the applicant and X-KG agreed on January 31, 2013 that the applicant would provide accounting and management services for X-KG in connection with the two construction projects in the future in return for payment.

During the year under dispute, stakes were held in Y-KG by Q Verwaltungs-GmbH, as the general partner, and the applicant (with 89.64% of the shares) and P I, the limited liability company under German law (P I GmbH) (with 10.36% of the shares) as limited partners. Q Verwaltungs-GmbH was not required to make any investment and does not have any capital share; it does not share in any profit or loss and does not possess any voting rights. Neither A nor B nor closely associated persons hold a stake in P I GmbH.

On April 10, 2013, it was agreed that P I GmbH would pay a premium of EUR 3.5 million and that the applicant would provide services free of charge worth at least EUR 30.29 million for a building project of Y-KG. The applicant provided these services partly with its own personnel and its own machinery, and partly with assistance from other companies.

Furthermore, the applicant and Y-KG agreed on April 10, 2013 that the applicant would provide accounting and management services for Y-KG in connection with the construction project in the future in return for payment.

The applicant made a deduction in full on the basis of its input services for 2013. However, the Finanzamt (Tax Office), the defendant, assessed the applicant’s shareholder contributions for X-KG and Y-KG without consideration as activities that did not serve to earn income in the sense of value added tax law and therefore were not classifiable as a business activity of the applicant. It held the view that tax amounts that were directly and immediately linked to these activities are not deductible.

The Finanzgericht (Finance Court) upheld the action brought against the tax office. It stated that the supply of benefits in kind as a shareholder contribution forms part of the business activity. This is apparent from the case-law of the Court of Justice of the European Union. It deemed that no abuse of legal tax arrangements has taken place, and that there are grounds outside of the scope of tax law that justify the chosen arrangement.

The Tax Office lodged an appeal on a point of law against the decision of the Finance Court before the referring court (Bundesfinanzhof (Germany)).

Questions referred for a preliminary ruling

Under circumstances such as those in the main proceedings, is Article 168(a) in conjunction with Article 167 of Council Directive 2006/112/EC of 28 November 2006 on the common system of value added tax to be interpreted in such a way that a managing holding that supplies taxable output services for subsidiaries is entitled to deduction, also for services that it obtains from third parties and contributes to the subsidiaries in return for the grant of a share in the general profit, even though the obtained inputs are not directly and immediately linked to the holding’s own transactions but instead to the (largely) tax-exempt activities of the subsidiaries, the obtained input services are not included in the price of the taxable transactions (supplied to the subsidiaries), and they do not form part of the general cost components of the holding’s own economic activity?

If Question 1 is answered in the affirmative: Does it constitute abuse of rights in the sense of the case-law of the Court of Justice of the European Union, if a managing holding is involved as an ‘intermediary’ in obtaining services for subsidiaries in such a way that it obtains services itself for which the subsidiaries would have no entitlement to deduction if services were obtained directly, contributes these services to the subsidiaries in return for participation in its profit, and then claims full deduction on the basis of the inputs on the grounds of its position as a managing holding; or can acting as an intermediary in this way be justified on grounds that fall outside the scope of tax law, even though full deduction is in itself in conflict with the system and would result in a competitive advantage for holding structures over single-tier companies?

Conclusion of the AG

1) Article 168(a), in conjunction with Article 167 of Council Directive 2006/112/EC of 28 November 2006 on the common system of value added tax, must be interpreted as meaning that a managing holding, which in a subsequent stage carries out taxable transactions for subsidiaries, is not entitled to deduct input tax on services it obtains from third parties and contributes to the subsidiaries in return for the grant of a share in the general profit, if these earlier obtained services are not directly and immediately related to the holding’s own transactions but instead to the (largely) tax-exempt activities of the subsidiaries, and the obtained input services are not included in the price of the taxable transactions (supplied to the subsidiaries), and they do not form part of the general cost components of the holding’s own economic activity.

2) The fact that a managing holding is included as an "intermediate" in the chain of services to subsidiaries in such a way that it itself purchases the services for which the subsidiaries would not be entitled to deduct input tax in the event of a direct purchase, transfers them to the subsidiaries against a participation in their profits and then claims full deduction of the input tax on the services at an earlier stage, relying on the grounds of its position as a managing holding, constitutes a tax advantage, the grant of which conflicts with the purpose of the deduction scheme of the VAT Directive. Such a transaction constitutes an abuse of rights, even if it can be justified on non-tax objectives, if it appears that the essential purpose of the transaction is to obtain a tax advantage.”

Copyright – internationaltaxplaza.info