On July 1, 2022 the judgments of the Dutch Supreme Court in 2 similar cases were published on the website of the Dutch courts. Both cases regard the interpretation of the remittance provision, as included in Article 2, Paragraph 5 of the Agreement between the Kingdom of the Netherlands and Malta for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income and on capital (Hereafter: the Dutch-Maltese DTA or the Treaty), in case of a dual resident entities. In particular the taxpayers and the Dutch tax authorities are disputing whether or not the Netherlands the remittance provision grants the Netherlands the right to tax owed/unpaid interest that is owed to a dual resident entity which was incorporated under Dutch law and effectively managed from Malta.

The case in which the Dutch Supreme Court ruled on July 1, 2022 are case number: 20/03826 (ECLI:NL:HR:2022:974) and case number: 22/01140 (ECLI:NL:HR:2022:979). Since the cases are very similar and the Dutch Supreme Court ruled in the same way, in this article we will focus on case number: 20/03826.

The facts of case number: 20/03826

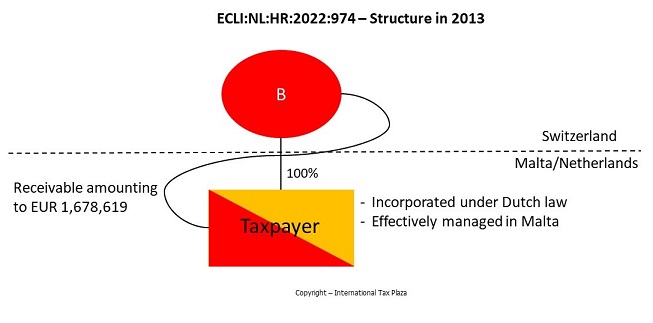

In 1994 the taxpayer was incorporated under Dutch law and has its registered office in Malta. The taxpayer has the legal form of a BV (a private limited company). As of June 24, 2004 all shares in the taxpayer are owned by B, which is an individual.

In 2004 B emigrated to Switzerland and he/she has lived there ever since.

The taxpayer is effectively managed in Malta.

The 2013 financial statements of the taxpayer state a shareholders' equity of EUR 3,275,969 at year-end 2013. A’s balance sheet total amounts to EUR 4,208,477 and partly consists of a receivable from B (A’s shareholder) of EUR 1,678,619.

A’s result for the year 2013 amounts to EUR 35,188. A’s result for the year comprises out an amount of EUR 53,485 of (unpaid) interest owed by B, EUR 13 interest received form a bank and interest costs amounting to EUR 18,310.

Under Maltese tax law the taxpayer is considered non-domiciled, which means that in Malta it is taxed for:

- The income it generated in Malta; and

- The income it generated outside of Malta, to the extent that this income is remitted to Malta.

Capital gains arising outside Malta are not subject to tax in Malta, regardless of whether they are received in Malta.

In its Maltese profit tax return for the year 2013, the taxpayer stated the interest owed by B amounting to EUR 53,485 as 'Investment income not arising and not remitted to Malta'. On that basis, no profit tax has been levied in Malta over this amount.

In its 2013 Dutch corporate income tax return the taxpayer reported a taxable profit amounting to nil.

The Dutch tax inspector issued a 2013 Dutch corporate income tax assessment for a taxable profit of EUR 53,498.

The amount of EUR 53,498 interest due by the taxpayer’s shareholder was still outstanding as per November 2020.

The dispute

The taxpayer and the tax inspector are disputing whether or not based on Article 2, Paragraph 5 of the Dutch-Maltese DTA the Netherland is allowed to tax the amount of EUR 53,498 to the extent that the interest has been not remitted to, nor received in Malta.

The District Court of Gelderland ruled that the Netherlands is not allowed the interest. In appeal the Court of Appeal of Arnhem-Leeuwarden ruled that the Netherlands is allowed to tax the interest.

The taxpayer appealed against the judgment of the Court of Appeal of Arnhem-Leeuwarden. In his conclusion the Advocate General proposed that the Dutch Supreme Court denies the taxpayer’s appeal and rules that based on Article 2, Paragraph 5 of the Dutch Maltese DTA the Netherlands is allowed to tax the interest to the extent the interest has not been remitted to, nor received in Malta.

Pleas of the taxpayer

I. the Court of Appeal incorrectly or insufficiently substantiated that pursuant to Article 2, Paragraph 5 of the Dutch-Maltese DTA the Netherlands may levy taxes over the interest to the extent that it was not transmitted to Malta:

(i) The Court of Appeal wrongly assumed that in principle the Netherlands is allowed to tax the taxpayer’s worldwide profit. Pursuant to Article 4 and Article 7 of the Dutch-Maltese DTA and the Ireland II judgment, the Netherlands is no longer allowed to the treat the taxpayer as a resident taxpayer and to subsequently tax its worldwide profit. Article 2, Paragraph 5 of the Dutch-Maltese DTA does not change that.

(ii) The Court disregarded the appeal on the purpose and scope of the remittance provision, which is based on Maltese tax law. Article 2, Paragraph 5 is a unilateral provision that ensures that income from the Netherlands that is not transferred to Malta can be taxed in the Netherlands. For Swiss income that has not been transferred to Malta, the Netherlands is neither the source state nor the recipient state. From the treaty perspective of Malta, where the taxpayer is residing, there is no reason whatsoever to grant taxing rights in Switzerland for interest not transferred to Malta to the Netherlands, where the interested party has no connection point other than its right of incorporation. The Swiss interest is a matter between Switzerland and Malta.

(iii) Article 2, Paragraph 5 of the Dutch-Maltese DTA does not allocate taxing rights, but merely limits the relieve obligation arising from other Treaty provisions. It does not mean that unremitted income falls outside the scope of the Treaty and thus falls within Dutch levying rights pursuant to Article 2, Paragraph 4 of the Dutch corporate income tax (DCIT) Act. The Court therefore wrongly failed to indicate under which Treaty provision the interest would fall. According to the taxpayer the interest does not fall within the scope of Article 11, nor within the scope of Article 7; Article 11 does not apply because it only concerns interest stemming from a Contracting State and Article 7 does not apply because the interested party does not have a permanent establishment in the Netherlands. Neither from the text of the remittance provision nor otherwise is it unequivocally clear, as HR BNB 1977/111 demands, that the Netherlands has reserved the right to tax profits that are not attributable to a permanent establishment in the Netherlands. Article 7 allocates taxing rights, but there is nothing to apportion if no permanent establishment exists.

II. The Court erred in ruling that Article 2, Paragraph 5 of the treaty also covers income for which the treaty contains an unabridged allocation rule, such as Article 7, which allocates the entire profit exclusively to Malta. After all, with exclusive allocation (object exemption) one cannot obtain a 'relieve' of tax, because with an object exemption there is no tax at all. The taxpayer does not consider it likely that the contracting states took into account the unfavorable outcome of HR BNB 1977/111 for the Netherlands on the (later repaired) remittance provision in the old treaty with the UK.

Judgment of the court

The Dutch Supreme Court denied the appeal of the taxpayer and confirmed the judgement of the Court of Appeal of Arnhem-Leeuwarden. Hence the Dutch Supreme Court ruled that based on Article 2, Paragraph 5 of the Dutch Maltese DTA the Netherlands is allowed to tax the interest to the extent the interest has not been remitted to, nor received in Malta.

Legal context

Dutch law

Article 2, Paragraph 4 of the DCIT Act

If an entity has been incorporated/established under Dutch law, then for the purposes of this Act, with the exception of Articles 13 to 13d, 13i to 13k, 14a, 14b, 15 and 15a, the company is always deemed to be to be residing in the Netherlands. In the case of an entity that would not be a resident taxpayer without the application of the first sentence, by derogation of Chapter II, the benefit stemming form a substantial interest as referred to in Article 17, Paragraph 3, under b, is determined on the basis of Chapter III. A European public limited liability company that was governed by Dutch law at the time of its incorporation is deemed to have been incorporated/established under Dutch law for the purposes of the first sentence.

Article 8, Paragraph 1 of the DCIT Act

The profit is interpreted and determined on the basis of Articles 3.8, 3.11 and 3.12, 3.13, first paragraph, parts a, g, h and i, 3.14, first paragraph, parts b to i, and second to fifth paragraph, 3.21 to 3.30, 3.30a, first to seventh paragraph, 3.31 to 3.54, 3.55 to 3.57, 10.10, 10a.2, 10a.3 and 10a.18 of the Individual Income Tax Act 2001, whereby for entrepreneur is to be read a taxpayer.

Article 3.8 Individual Income Tax Act

Profit from an enterprise (profit) is the amount of joint benefits obtained, under whatever name and in whatever form, from an enterprise.

The Dutch-Maltes DTA

Article 2, Paragraph 5 - Taxes covered

Where under any provision of this Agreement income is relieved from tax in one of the States, either in full or in part, and, under the law in force in the other State, a person, in respect of the said income, is subject to tax by reference to the amount thereof which is remitted to or received in that other State and not by reference to the full amount thereof, then the relief to be allowed under this Agreement in the first-mentioned State shall apply to so much of the income as is remitted to or received in the other State.

Article 3, Paragraph 2 - General definitions

As regards the application of this Agreement by either of the States, any term not otherwise defined shall, unless the context otherwise requires; have the meaning which it has under the laws of that State relating to the taxes which are the subject of this Agreement.

Article 4 - Fiscal domicile

1 For the purposes of this Agreement, the term “resident of one of the States” means any person who, under the law of that State, is liable to taxation therein by reason of his domicile, residence, place of management or any other criterion of a similar nature. The term does not include any person who is liable to tax in that State in respect only of income from sources therein or capital situated in that State.

2 For the purposes of this Agreement an individual, who is a member of a diplomatic or consular mission of one of the States in the other State or in a third State and who is a national of the sending State, shall be deemed to be a resident of the sending State if he is submitted therein to the same obligations in respect of taxes on income and capital as are residents of that State.

3 Where by reason of the provisions of paragraph 1 an individual is a resident of both States, then his status shall be determined as follows:

a. he shall be deemed to be a resident of the State in which he has a permanent home available to him. If he has a permanent home available to him in both States, he shall be deemed to be a resident of the State with which his personal and economic relations are closest (centre of vital interests);

b. if the State in which he has his centre of vital interests cannot be determined, or if he has not a permanent home available to him in either State, he shall be deemed to be a resident of the State in which he has an habitual abode;

c. if he has an habitual abode in both States or in neither of them, he shall be deemed to be a resident of the State of which he is a national;

d. if he is a national of both States or of neither of them, the competent authorities of the States shall settle the question by mutual agreement.

4 Where by reason of the provisions of paragraph 1, a person other than an individual is a resident of both States, then it shall be deemed to be a resident of the State in which its place of effective management is situated.

Article 5 - Permanent establishment

1 For the purposes of this Agreement, the term “permanent establishment” means a fixed place of business in which the business of the enterprise is wholly or partly carried on.

2 The term “permanent establishment” shall include especially:

a. a place of management;

b. a branch;

c. an office;

d. a factory;

e. a workshop;

f. a mine, quarry or other place of extraction of natural resources;

g. a building site or construction or assembly project or supervisory activities in connection therewith, where such site, project or activity continues for more than twelve months.

3 The term “permanent establishment” shall not be deemed to include:

a. the use of facilities solely for the purpose of storage, display or delivery of goods or merchandise belonging to the enterprise;

b. the maintenance of a stock of goods or merchandise belonging to the enterprise solely for the purpose of storage, display or delivery;

c. the maintenance of a stock of goods or merchandise belonging to the enterprise solely for the purpose of processing by another enterprise;

d. the maintenance of a fixed place of business solely for the purpose of purchasing goods or merchandise, or for collecting information, for the enterprise;

e. the maintenance of a fixed place of business solely for the purpose of advertising, for the supply of information, for scientific research or for similar activities which have a preparatory or auxiliary character, for the enterprise.

4 A person acting in one of the States on behalf of an enterprise of the other State - other than an agent of an independent status to whom paragraph 5 applies - shall be deemed to be a permanent establishment in the first-mentioned State if he has, and habitually exercises in that State, an authority to conclude contracts in the name of the enterprise, unless his activities are limited to the purchase of goods or merchandise for the enterprise.

5 An enterprise of one of the States shall not be deemed to have a permanent establishment in the other State merely because it carries on business in that other State through a broker, general commission agent or any other agent of an independent status, where such persons are acting in the ordinary course of their business.

6 The fact that a company which is a resident of one of the States controls or is controlled by a company which is a resident of the other State, or which carries on business in that other State (whether through a permanent establishment or otherwise), shall not of itself constitute either company a permanent establishment of the other.

Article 7 - Business profits

1 The profits of an enterprise of one of the States shall be taxable only in that State unless the enterprise carries on business in the other State through a permanent establishment situated therein. If the enterprise carries on business as aforesaid, the profits of the enterprise may be taxed in the other State but only so much of them as is attributable to that permanent establishment.

2 Subject to the provisions of paragraph 3, where an enterprise of one of the States carries on business in the other State through a permanent establishment situated therein, there shall in each State be attributed to that permanent establishment the profits which it might be expected to make if it were a distinct and separate enterprise engaged in the same or similar activities under the same or similar conditions and dealing wholly independently with the enterprise of which it is a permanent establishment.

3 In the determination of the profits of a permanent establishment, there shall be allowed as deductions expenses which are incurred for the purposes of the permanent establishment including executive and general administrative expenses so incurred, whether in the State in which the permanent establishment is situated or elsewhere.

4 Insofar as it has been customary in one of the States to determine the profits to be attributed to a permanent establishment on the basis of an apportionment of the total profits of the enterprise to its various parts, nothing in paragraph 2 shall preclude that State from determining the profits to be taxed by such an apportionment as may be customary; the method of apportionment adopted shall, however, be such that the result shall be in accordance with the principles embodied in this Article.

5 No profits shall be attributed to a permanent establishment by reason of the mere purchase by that permanent establishment of goods or merchandise for the enterprise.

6 For the purposes of the preceding paragraphs, the profits to be attributed to the permanent establishment shall be determined by the same method year by year unless there is good and sufficient reason to the contrary.

7 Where profits include items of income which are dealt with separately in other Articles of this Agreement, then the provisions of those Articles shall not be affected by the provisions of this Article.

Article 11 - Interest

1 Interest arising in one of the States and paid to a resident of the other State may be taxed in that other State.

2 However, such interest may be taxed in the State in which it arises and according to the law of that State, but if the recipient is the beneficial owner of the interest, the tax so charged shall not exceed 10 per cent of the gross amount of the interest.

3 Notwithstanding the provisions of paragraph 2:

a. interest arising in Malta and paid to the Netherlands Government, the Central Bank of the Netherlands, the Nederlandse Financieringsmaatschappij voor Ontwikkelingslanden N.V. (Netherlands finance company for developing countries), and the Nederlandse Investeringsbank voor Ontwikkelingslanden N.V. (Netherlands investment bank for developing countries) shall be exempt from Malta tax;

b. interest arising in the Netherlands and paid to the Malta Government, the Central Bank of Malta or the Malta Development Corporation shall be exempt from Netherlands tax;

c. the exemptions granted by this paragraph shall also apply to any other statutory body of one of the States if such body possesses a distinct legal personality.

4 The term “interest” as used in this Article means income from Government securities, income from bonds or debentures, whether or not secured by mortgage but not carrying a right to participate in profits, and income from debt-claims of every kind whether or not secured by mortgage, as well as all other income assimilated to income from money lent by the taxation law of the States in which the income arises.

5 The provisions of paragraphs 1 and 2 shall not apply if the recipient of the interest, being a resident of one of the States, carries on business in the other State in which the interest arises, through a permanent establishment situated therein, or performs in that other State professional services from a fixed base situated therein, and the debt-claim in respect of which the interest is paid is effectively connected with such permanent establishment or fixed base. In such a case, the provisions of Article 7 or Article 15, as the case may be, shall apply.

6 Interest shall be deemed to arise in one of the States when the payer is that State itself, a political subdivision, a local authority or a resident of that State. Where, however, the person paying the interest, whether he is a resident of one the States or not, has in one of the States a permanent establishment in connection with which the indebtedness on which the interest is paid was incurred, and such interest is borne by such permanent establishment, then such interest shall be deemed to arise in the State in which the permanent establishment is situated.

7 Where, owing to a special relationship between the payer and the recipient or between both of them and some other person, the amount of the interest paid, having regard to the debt-claim for which it is paid, exceeds the amount which would have been agreed upon by the payer and the recipient in the absence of such relationship, the provisions of this Article shall apply only to the last-mentioned amount. In that case, the excess part of the payments shall remain taxable according to the law of each State, due regard being had to the other provisions of this Agreement.

From the considerations of the court

2.2 Before the Court of Appeal it was amongst others disputed whether the application of Article 2, Paragraph 5 of the Dutch-Maltese DTA (hereinafter: the Treaty) leads to the Netherlands is competent to levy tax on the interest, to the extent that the interest has not been remitted to or received in Malta. The Court of the Appeal answered this question in the affirmative and ruled that the interest is part of the Dutch tax base of the taxpayer. Both pleas are directed against this.

2.3

2.3.1 The Court has ruled – and this has not been contested in cassation – that the taxpayer is regarded by both the Netherlands and Malta as a resident within the meaning of Article 4, Paragraph 1 of the Treaty, and that for the purposes of the Treaty, in accordance with Article 4, Paragraph 4 of the Treaty (the tie-breaker rule) shall be deemed to be a resident of Malta. The taxpayer does not have a permanent establishment in the Netherlands as referred to in Article 5 of the Convention. This means that, in accordance with Article 7, Paragraph 1 of the Treaty, the benefits of the taxpayer, such as the interest, are taxable only in Malta. Although the interested party was incorporated/established under Dutch law and must therefore be regarded as a resident Dutch taxpayer, pursuant to Article 2, Paragraph 4 of the DCIT Act 1969 ,this does not mean that those benefits are included in the profit of the taxpayer that is to be taxed in the Netherlands.

2.3.2 From Article 2, Paragraph 5 of the Treaty it follows that a total or partial relieve of tax on certain income which the Netherlands is required to grant according to a provision of the Treaty shall apply only to that part of the income which has been remitted to Malta or which has been received there, if under the laws applicable Malta a person is not subject to tax in respect of such income in full but only to the extent that such income is remitted or received there.

Considering the wording used in this provision – “…relieved from tax in one of the States, either in full or in part,” – the purpose of the provision is to arrange that income which, as a result of the application of Chapter III of the Treaty, would not be included (in the whole) or only to a limited extent in the levying of Dutch tax, are included in that levy to the extent that that income is not (yet) included in the levying of tax in Malta because the income has not been transferred to Malta and has not been received there. For answering the question whether a total or partial relieve of Dutch tax as referred to in Article 2, Paragraph 5 of the Treaty occurs, the decisive factor is whether application of Chapter III of the Treaty results in the levying of Dutch tax, which would have been due without the application of the Treaty, is wholly or partly omitted. From this it follows that Article 2, Paragraph 5 of the Treaty also covers income for which the Treaty allocates the taxing rights exclusively to a Contracting State.

2.3.3 In view of the considerations made in 2.3.1, the levying rights of the income of the taxpayer as defined in Article 7 of the Treaty are exclusively allocated to Malta. Therefore, that income is included in the income for which a full relieve of Dutch tax as referred to in Article 2, Paragraph 5 of the Treaty applies.

If, however, under the laws in force in Malta, the income in question is subject to tax in Malta only to the extent that it has been remitted to Malta or it was received there, Article 2, Paragraph 5 of the Treaty provides that the relieve of Dutch tax shall apply only to the extent that such income has been transferred to or received in Malta. For income as defined in Article 7 of the Treaty, this means that, with due observance of the relevant Dutch tax legislation, they are and to that extent are included in the profit that is to be taxed in the Netherlands.

2.3.4. The income as defined in Article 7 of the Treaty includes all benefits of an enterprise of one of the Contracting States, so including benefits stemming from a source that is located in another jurisdiction that the Netherlands or Malta.

Admittedly, there are arguments for the view that the application of Article 2, Paragraph 5 of the Treaty, according to which the Netherlands is not required to grant a relief on certain income in cases such as that of the interested party, does not result in the income from a source in a third state is to be included in the profit to be taxed in the Netherlands. After all, if the interest had been transferred to Malta, or if it had been received there, under the Treaty the interest would not be allocated to the Netherlands for taxation. In that case, the levying rights regarding the interest would not have been allocated to the Netherlands under the Dutch-Switzerland Tax Treaty (conform Article 11, Paragraph 1 of said treaty). However, the text of Article 2, Paragraph 5 of the Treaty does not contain a reference that supports that view. With regard to income for which Chapter III of the Treaty provides for a total or partial relief of Dutch tax, this text makes no distinction between situations in which the income arises from a source in the Netherlands, Malta or another state. Nor is this view supported by any apparent common intention of the Contracting States.

2.3.5 Based on what has been considered in 2.3.2 to 2.3.4 above, it must be assumed that in cases such as that of the taxpayer, income from a source located in a state other than the Netherlands or Malta, is also considered to be part of the income that is to be taxed in the Netherlands, except to the extent that it has been transferred to Malta or that it has been received there. The Court of Appeal was therefore right in its judgment that Article 2, Paragraph 5 of the Treaty grants the Netherlands the right to levy tax over the interest to the extent that the interest has not been transferred to Malta or has not been received there. The pleas fail.

2.4 The following deserves noticing. The term “income” used in Article 2, Paragraph 5 of the Treaty is not defined in this provision or elsewhere in the Treaty. In cases as meant in Article 2, Paragraph 4 of the DCIT Act, Article 3, Paragraph 2 of the Treaty entails that that expression must be interpreted in accordance with the provisions of the DCIT Act on the determination of the income of resident taxpayers . According to Article 8, Paragraph 1, of the DCIT Act, read in conjunction with Article 3.8 of the Dutch Individual Income Tax Act, the amount of the joint income, under whatever name and in whatever form, are obtained by a company, is included in the profits of resident taxpayers. The income described in these provisions include capital gains. Therefore, for the purposes of Article 2, Paragraph 5 of the Treaty in cases as the aforementioned ones, capital gains should be regarded as income within the meaning of this provision. Neither the context of Article 2, Paragraph 5 of the Treaty nor any other provision of the Treaty precludes this interpretation.

Observations by AJT

'Remittance base' provisions are amongst others included in the tax treaties that the Netherlands has concluded with Malaysia, Malta, Singapore and the United Kingdom.

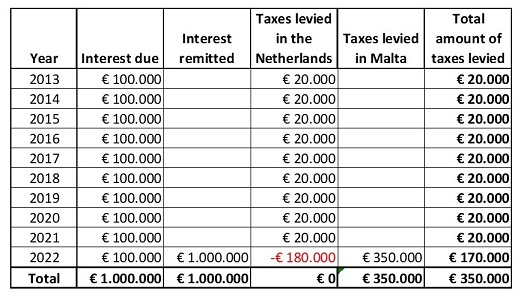

The judgments of the Dutch Supreme Court of July 1, 2022 raises a question. Based on these Supreme Court’s judgments the Netherlands is allowed to tax the interest income in 2013 because of the fact that the debtor did (not yet) remit the interest to a (Maltese) bank account of the taxpayer as a result of which that interest income was not yet taxed in Malta. But what happens if for example the shareholder pays/remits the interest still due in a future year?

Example

A shareholder has an outstanding debt to his dual resident Dutch-Maltese entity, which is effectively managed in Malta. The debt amounts to EUR 2 million. The annual interest due over the debt amounts to EUR 100k. The shareholder does not pay/remit the interest that is due over the years 2013 through 2021, instead the interest is added to the amount outstanding on the debt. In the year 2022 the shareholder pays/remits the total amount of interest that is due over the years 2013 through 2022 (EUR 1 million).

Since no interest is paid/remitted to Malta in the years 2013 through 2021 each year the Netherlands will levy taxes over the unpaid/interest (EUR 100k interest per year). Whereas Malta will not levy any taxes over this accrued but unpaid interest.

In 2022 the shareholder pays/remits an amount of 1 million of interest relating to the years 2013 through 2022. Since at this moment the interest is remitted to Malta, Malta will levy taxes over the EUR 1 million of interest. The Netherlands on its turn will grant a 'relief' since the relevant income or capital gains are transferred to Malta. Not only for the amount of EUR 100k of interest that relates to the year 2022, but also for the interest that accrued over the period 2013 through 2021. This follows not only from the text of the remittance provision itself, but is also made more explicit, for example in the explanation of the remittance provision in the Dutch-Irish DTA which reads as follows:

“As far as the Netherlands is concerned in view of the provisions of the Treaty this means that the Netherlands will grant a refund of any excess tax when the relevant item of income is transferred to Ireland.”

In figures the aforementioned looks as follows*:

* The calculations above are made under the assumption that in the Netherlands a DCIT rate of 20% applied for the full period 2013-2022. Whereas it is assumed that a 35% corporate income tax rate applied in Malta for the full period 2013-2022.

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)