On July 14, 2022 on the website of the Court of Justice of the European Union (CJEU) the opinion of Advocate General Kokott in Case C-247/21, Luxury Trust Automobil GmbH (ECLI:EU:C:2022:588), was published. Other party in the proceedings was the Finanzamt Österreich.

Introduction

This case gives the Court the opportunity to clarify and nuance its ‘substance over form’ case-law. In that context, it is possible that the telos of the respective provisions will have to be taken into account to a greater degree than before. The present case concerns a special case of an intra-Community chain transaction, the ‘intra-Community triangular transaction’. Such transactions have barely been the subject of decisions of the Court.

If goods are sold from A (NL) to B (AT) and then from B to C (CZ), and are then delivered directly from A to C, and the supply from A to B is the exempt (in the Netherlands) intra-Community supply, then the following applies, in accordance with the normal rules: B must register in the Czech Republic (that is to say, the country of destination) in order to pay, in that country, tax on the intra-Community acquisition of the goods and VAT on the sale of the goods to C. Until it is established that tax has been applied to the acquisition in the country of destination, B must additionally pay tax on an intra-Community acquisition in Austria. The latter situation is the subject matter of the present dispute.

In order to reduce that complexity, the legislature created a special scheme for that case (three undertakings from three Member States with three identification numbers originating from those Member States trade in goods which are transported directly from the first undertaking to the last one) by way of Article 141 in conjunction with Article 42 and Article 197 of the VAT Directive (‘the intra-Community triangular transaction’).

It allows the intermediate undertaking (B) to avoid registration in the country of destination (CZ) and the existence – subject to a condition subsequent – of an intra-Community acquisition in the Member State that issued the VAT identification number under which the acquisition was made (AT), if and because the tax liability for its supply is transferred to the last undertaking in the chain (and thus also to the country of destination). However, in order that the latter undertaking (C) is aware of this and pays, in the country of destination, the appropriate tax on the acquisition of the goods, the scheme is tied to, inter alia, the issuing of an invoice which refers to that transfer of the tax liability.

But what happens if there is no such reference in the invoice? In some decisions, the Court has taken the view that merely formal errors cannot call the deduction of input tax into question. Does this also apply to the use of that special scheme? Or is the reference to a reverse charge in the invoice a substantive requirement in that regard?

The particular – and also practical – importance of that question of law, which has hitherto not been clarified by the Court, is reflected in the fact that in Germany alone there are now three finance court decisions on precisely that issue with different outcomes. It is interesting to note that all three cite the Court’s case-law in equal measure. This has led to two appeals on points of law being brought before the Bundesfinanzhof (Federal Finance Court, Germany), which is now awaiting the ruling to be given by the Court in the present case.

Facts and preliminary ruling procedure

17. Luxury Trust Automobil GmbH is an Austrian limited liability company with its registered office in Austria (‘the applicant’). Its business includes cross-border brokering and cross-border sales of luxury vehicles.

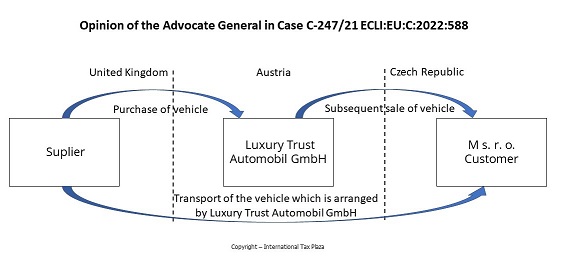

18. On multiple occasions in 2014, the applicant purchased vehicles from a supplier in the United Kingdom and sold them on to a company with its registered office in the Czech Republic (‘M s. r. o.’). The three undertakings involved each acted under the VAT identification number (‘the VAT ID’) of their State of establishment. The vehicles arrived directly from the supplier in the United Kingdom to the recipient in the Czech Republic; the transport of the vehicles had been arranged by the applicant.

19. The applicant’s three invoices (each from March 2014) stated the Czech VAT ID of the recipient, the Austrian VAT ID of the applicant and the United Kingdom VAT ID of the supplier. Each of the invoices included the reference ‘Exempt intra-Community triangular transaction’. VAT was not mentioned on the invoices (only the ‘net amount of the invoice’ in each case).

20. In the recapitulative statement for the month of March 2014, the applicant reported these supplies of goods in relation to the VAT ID of the Czech recipient and reported the existence of triangular transactions.

21. The Czech company M s. r. o. is classified by the Czech tax authorities as a ‘missing trader’. The company could not be contacted by the Czech tax authorities and it did not declare or pay VAT in the Czech Republic on the triangular transactions. However, during the period in which the supplies at issue were made, M s. r. o. was registered for VAT purposes in the Czech Republic.

22. In its decision dated 25 April 2016, the Finanzamt (Tax Office, Austria) assessed the applicant’s VAT liability for the year 2014. In the grounds of its decision, the Tax Office stated that the three invoices issued by the applicant to the Czech company M s. r. o. did not contain any reference to the transfer of the tax liability (Article 25(4) of the UStG). Due to the use of the Austrian VAT ID, an intra-Community acquisition in Austria was assumed to exist in accordance with Article 3(8) of the UStG.

23. The Bundesfinanzgericht (Federal Finance Court, Austria) dismissed the action brought by the applicant against that decision. In its statement of grounds, the Bundesfinanzgericht (Federal Finance Court) added that the applicant had amended the three invoices by adding amendments dated 23 May 2016, making reference to the transfer of the tax liability to the person to whom the supply is made. Proof of actual service of the invoice amendments to the Czech company has not been established, however. Therefore, in the absence of any amendment of the incorrect invoices, the court believes there is no need to examine the question further of whether a subsequent correction of an invoice makes it possible to benefit from the simplification rules for triangular transactions. In the present case, no tax was paid in the country of destination.

24. It stated that the provisions relating to triangular transactions are not mandatorily applicable in a set of circumstances as referred to in Article 25(1) of the UStG. Rather, the acquirer (the intermediate undertaking in a triangular transaction) has the right to choose whether or not to apply the triangular transaction regime with respect to a particular supply. If the acquirer wishes to obtain tax exemption for its intra-Community acquisition in the Member State of destination and to transfer the tax liability relating to its supply to the recipient, it must include in the invoice the details stipulated in Article 25(4) of the UStG. This did not take place in the present case. Consequently, the provisions of Article 25 of the UStG are not applicable.

25. The applicant brought an appeal against that judgment before the Verwaltungsgerichtshof (Supreme Administrative Court, Austria). That court stayed the proceedings and referred the following questions to the Court for a preliminary ruling under Article 267 TFEU:

‘(1) Is Article 42(a) of [the VAT Directive] in conjunction with Article 197(1)(c) of that Directive … to be interpreted as meaning that the person to whom the supply is made is to be designated as liable for payment of VAT if the invoice, which does not show the amount of value added tax, states: “Exempt intra-Community triangular transaction”?

(2) If the first question is answered in the negative:

(a) Can such a mention on the invoice be amended so as to apply retroactively (by stating: “Intra-Community triangular transaction in accordance with Article 25 of [the UStG]. Liability for payment of VAT is transferred to the customer”)?

(b) Is it necessary for the invoice recipient to receive the amended invoice in order for an amendment to be effective?

(c) Does the effect of the amendment apply retroactively to the original date of invoicing?

(3) Is Article 219a of [the VAT Directive] to be interpreted as meaning that the rules on invoicing to be applied are those of the Member State whose provisions would be applicable if a “customer” has not (yet) been designated on the invoice as the person liable for payment of VAT; or are the rules to be applied those of the Member State whose provisions would be applicable if the designation of the “customer” as the person liable for payment of VAT is accepted as valid?’

26. The applicant, the Republic of Austria and the European Commission submitted written observations in the proceedings before the Court. In accordance with Article 76(2) of the Rules of Procedure of the Court, the Court did not consider it necessary to hold a hearing.

Conclusion

Advocate General Kokott proposes that the Court answer the questions referred by the Verwaltungsgerichtshof (Supreme Administrative Court, Austria) for a preliminary ruling as follows:

(1) The person to whom the supply is made is to be regarded as having been designated as liable for payment of VAT within the meaning of Article 197 of Council Directive 2006/112/EC on the common system of value added tax only if the invoice concerned referred to a reverse charge to the recipient of the supply. The indication ‘Exempt intra-Community triangular transaction’ is not sufficient in that regard.

(2) An invoice that contains the required indication ‘Reverse charge’ can still be issued subsequently, but only with ex nunc effect. In that respect, it is necessary that that invoice be received by the recipient of the supply.

Legal framework

A. European Union law

7. The legal framework under EU law is formed by the VAT Directive.

8. Article 40 of the VAT Directive reads as follows:

‘The place of an intra-Community acquisition of goods shall be deemed to be the place where dispatch or transport of the goods to the person acquiring them ends.’

9. Article 41 of the VAT Directive provides as follows:

‘Without prejudice to Article 40, the place of an intra-Community acquisition of goods as referred to in Article 2(1)(b)(i) shall be deemed to be within the territory of the Member State which issued the VAT identification number under which the person acquiring the goods made the acquisition, unless the person acquiring the goods establishes that VAT has been applied to that acquisition in accordance with Article 40.

If VAT is applied to the acquisition in accordance with the first paragraph and subsequently applied, pursuant to Article 40, to the acquisition in the Member State in which dispatch or transport of the goods ends, the taxable amount shall be reduced accordingly in the Member State which issued the VAT identification number under which the person acquiring the goods made the acquisition.’

10. Article 42 of the VAT Directive is worded as follows:

‘The first paragraph of Article 41 shall not apply and VAT shall be deemed to have been applied to the intra-Community acquisition of goods in accordance with Article 40 where the following conditions are met:

(a) the person acquiring the goods establishes that he has made the intra-Community acquisition for the purposes of a subsequent supply, within the territory of the Member State identified in accordance with Article 40, for which the person to whom the supply is made has been designated in accordance with Article 197 as liable for payment of VAT;

(b) the person acquiring the goods has satisfied the obligations laid down in Article 265 relating to submission of the recapitulative statement.’

11. Article 141 of the VAT Directive is worded as follows:

‘Each Member State shall take specific measures to ensure that VAT is not charged on the intra-Community acquisition of goods within its territory, made in accordance with Article 40, where the following conditions are met:

…

(e) the person referred to in point (d) has been designated in accordance with Article 197 as liable for payment of the VAT due on the supply carried out by the taxable person who is not established in the Member State in which the tax is due.’

12. Article 197(1) of that directive provides as follows:

‘VAT shall be payable by the person to whom the goods are supplied when the following conditions are met:

(a) the taxable transaction is a supply of goods carried out in accordance with the conditions laid down in Article 141;

…

(c) the invoice issued by the taxable person not established in the Member State of the person to whom the goods are supplied is drawn up in accordance with Sections 3 to 5 of Chapter 3.’

13. Sections 3 to 5 of Chapter 3 cover Articles 219a to 237 of the VAT Directive. Article 219a of that directive provides as follows:

‘Without prejudice to Articles 244 to 248, the following shall apply:

(1) Invoicing shall be subject to the rules applying in the Member State in which the supply of goods or services is deemed to be made, in accordance with the provisions of Title V.

(2) By way of derogation from point (1), invoicing shall be subject to the rules applying in the Member State in which the supplier has established his business or has a fixed establishment from which the supply is made or, in the absence of such place of establishment or fixed establishment, the Member State where the supplier has his permanent address or usually resides, where:

(a) the supplier is not established in the Member State in which the supply of goods or services is deemed to be made, in accordance with the provisions of Title V, or his establishment in that Member State does not intervene in the supply within the meaning of Article 192a, and the person liable for the payment of the VAT is the person to whom the goods or services are supplied.

…’

14. Points 11 and 11a of Article 226 of the VAT Directive are worded as follows:

‘Without prejudice to the particular provisions laid down in this Directive, only the following details are required for VAT purposes on invoices issued pursuant to Articles 220 and 221:

…

(11) in the case of an exemption, reference to the applicable provision of this Directive, or to the corresponding national provision, or any other reference indicating that the supply of goods or services is exempt;

(11a) where the customer is liable for the payment of the VAT, the mention “Reverse charge”’.

B. Austrian law

15. Article 25(1) to (5) of the Umsatzsteuergesetz 1994 (1994 Law on turnover tax; ‘the UStG’), in the version applicable in 2014 (BGBl. I No 112/2012) is worded as follows:

‘(1) A triangular transaction occurs where three undertakings effect taxable transactions concerning the same goods in three different Member States, those goods are sent directly by the first supplier to the final customer and the conditions set out in paragraph 3 are satisfied. That shall also apply where the final customer is a legal person which is not an undertaking or is not acquiring the goods for its undertaking.

(2) The intra-Community acquisition within the meaning of the second sentence of Article 3(8) shall be deemed to be taxed when the undertaking (customer) proves that a triangular transaction has occurred and that it has complied with its obligations concerning the duty to declare under paragraph 6. If the undertaking does not comply with its duty to declare, the tax exemption shall be forfeited retroactively.

(3) The intra-Community acquisition shall be exempt from VAT where the following conditions are met:

…

(e) in accordance with paragraph 5, the recipient is liable to pay the tax.

(4) The issuing of the invoice shall be governed by the provisions of the Member State in which the acquirer operates its undertaking. If the supply is made from the acquirer’s permanent establishment, the law of the Member State in which the establishment is situated shall be applicable. If the recipient of the supply to whom liability for the tax is transferred settles by means of a credit note, the issuance of the invoice shall be governed by the provisions of the Member State in which the supply is made.

Where the provisions of this Federal Law are applicable to the issuance of the invoice, the invoice must additionally contain the following details:

– an express reference to the existence of an intra-Community triangular transaction and the fact that the final customer is liable for the tax;

– the VAT identification number under which the undertaking (acquirer) made the intra-Community acquisition and subsequent supply of the goods; and

– the VAT identification number of the recipient of the supply.

(5) In the case of a triangular transaction, the recipient of the taxable supply shall be liable to pay the tax where the invoice issued by the acquirer corresponds to paragraph 4.’

16. Article 3(8) of the UStG is worded as follows:

‘The intra-Community acquisition is made within the territory of the Member State in which the goods are located when their dispatch or transport ends. If the acquirer uses, in its dealings with the supplier, a VAT identification number issued to it by another Member State, the acquisition shall be deemed to have been made in the territory of that Member State, unless and until the acquirer proves that the acquisition has been taxed by the Member State referred to in the first sentence. …’

From the legal assessment of the AG

A. The questions referred

27. The questions referred concern, in essence, the handling of a specific cross-border chain transaction between three persons, which may become very expensive for the intermediate undertaking (the applicant) due to a ‘formal error’ in the invoice. Had the applicant stated for example the following in the invoice, it would not have to pay any tax in Austria: ‘Intra-Community triangular transaction in accordance with Article 42 in conjunction with Article 141 of the VAT Directive. We hereby inform you that liability for payment of VAT is transferred to you as the recipient of the supply in accordance with Article 197(1) of the VAT Directive.’

28. Unfortunately – from the point of view of the applicant – it only stated ‘Exempt intra-Community triangular transaction’, for which reason the tax authorities in Austria are taxing an intra-Community acquisition in Austria. This is based on the premiss that the supply to the applicant is the exempt intra-Community supply.

29. In that case, in accordance with Article 41(1) of the VAT Directive, the acquisition is additionally taxable in the Member State which issued the VAT ID under which the acquisition was made. In accordance with paragraph 2 of that article, the situation would be different only if the applicant had paid tax on the intra-Community acquisition in the Czech Republic. It has not done so yet. However, in accordance with the case-law of the Court, the applicant cannot neutralise the VAT under Article 41(1) of the VAT Directive by means of the deduction of the input VAT. That VAT thus becomes a cost factor for a taxable person, even though – as the Court has frequently stated – the latter is entirely to be relieved of the burden of VAT due or paid in the course of his or her economic activities.

30. For that reason, amongst others, the Court is quite generous when it comes to absent or incorrect invoice details. That ‘substance over form’ case-law has hitherto extended to the deduction of input VAT and the exemption of intra-Community supplies. It is true that the problems associated with that case-law that were encountered by the Member States in the monitoring of, in particular, cross-border transactions led to an amendment of the VAT Directive, which now expressly emphasises the particular importance of the VAT ID – which was previously treated as a mere formality – in a mass procedure such as VAT law. However, in the present case, that amendment is not temporally relevant and, moreover, the VAT ID is not missing.

31. The only issue in the present case is the lack of a reference to the transfer of the tax liability to the last undertaking in the chain in the context of an intra-Community triangular transaction. Another aspect of that situation is that an undertaking which receives an invoice that does not state VAT separately and indicates that there is an ‘exempt intra-Community triangular transaction’ may even come to the conclusion that it, as the recipient of the supply, owes VAT.

32. It is precisely for that reason that the referring court asks whether, despite the ‘formally’ incorrect invoice, there is nevertheless an intra-Community triangular transaction (from a substantive point of view), with the result that the applicant’s intra-Community acquisition is to be deemed as taxed in Austria (see section B). If that question is answered in the negative, the referring court asks whether it is at least permissible for the incorrect invoice to be corrected with retroactive effect and whether the corrected invoice must be received by the recipient of the supply (see section C). In addition, the referring court seeks to ascertain what should be stated in a corrected invoice, that is to say, according to which invoicing rules of which Member State (country of destination or country of the identification number used by the supplier) the invoice is to be corrected (see section D).

B. Need for an invoice that expressly refers to a reverse charge

1. ‘Substance over form’ case-law of the Court

33. The doubts as to whether such an invoice is in fact necessary in order to be able to make use of the special scheme result from the case-law of the Court. It is true that Article 178 of the VAT Directive requires ‘an invoice drawn up in accordance with Sections 3 to 6 of Chapter 3 of Title XI’ in order to be able to exercise the right of deduction. According to the Court’s case-law, the fundamental principle of VAT neutrality requires the deduction of input VAT to be allowed if the substantive requirements are satisfied, even if the taxable person has failed to comply with some of the formal requirements. Holding an invoice showing the details mentioned in Article 226 of the VAT Directive is a formal condition, not a substantive condition, of the right to deduct VAT.

34. In connection with the intra-Community triangular transaction, Article 141(e) of the VAT Directive, in conjunction with Article 197(1)(c) thereof, requires that the invoice issued be drawn up in accordance with ‘Sections 3 to 5 of Chapter 3’. If the Court were consistently to continue its above case-law, this would mean that that criterion would also be only formal in nature. It could then certainly be argued – in line with the view taken by the applicant and two of the German finance courts referred to above – that an infringement of formal requirements cannot lead to an outcome which is at odds with the principle of neutrality. Therefore, according to that argument, the Austrian tax authorities’ insistence on an express reference to the transfer of tax liability is disproportionate.

35. However, as I have already stated in several recent Opinions, formal requirements are certainly justified in mass proceedings such as those in VAT law. In particular, the requirement to comply with certain formal requirements which are known from the outset is not disproportionate per se.

36. In my view, the decisive question is not so much whether the requirements are formal or substantive in nature, but rather what purpose the legislature – that is to say, in this context, the legislature which adopted the directive – pursues by prescribing those formal requirements. Only if that purpose is established can it be decided whether an infringement of the formal requirement precludes the outcome that certain rights can be exercised. The categorisation of a requirement of the VAT Directive as a ‘merely’ formal requirement or as a substantive requirement is of secondary importance in that respect.

37. The fact that a numerical error in the indication of the invoice number on the invoice (a required indication under Article 226(2) of the VAT Directive) does not lead to refusal of the right of deduction does not result from the formal nature of that indication, but from the fact that such an invoice can adequately fulfil its purpose – monitoring of transactions and informing the recipient of the supply and the tax authorities of the content of the transaction – despite that error. If the tax authorities discern, on the basis of their tax audit, that such an invoice was issued only once in respect of the specific supply, refusal of the right of deduction on the basis of the numerical error is disproportionate. In that case, such an invoice does not even have to be corrected, or can automatically be corrected with retroactive effect.

38. The question as to whether failure to refer to the reverse charge in the context of an intra-Community triangular transaction is also immaterial therefore depends on the purpose of that statutorily prescribed indication in the invoice. Consequently, the purpose of the scheme for intra-Community triangular transactions must first be established (see section 2). After that, the importance of the reference – which is required in that respect – to the transfer of the tax liability to the recipient of the supply (see section 3) must be clarified. This will determine whether such a reference is a mandatory requirement of an intra-Community triangular transaction (see section 4).

2. Purpose of the scheme for intra-Community triangular transactions

39. As the Court already stated in its first decision concerning Article 141 of the VAT Directive, the purpose of the special scheme for intra-Community triangular transactions is to simplify matters for the parties involved. That simplification is twofold.

40. On the one hand, Article 141 of the VAT Directive allows the intermediate trader (in the present case, the applicant) to avoid having to register in the country of destination (in the present case, the Czech Republic). This is achieved by virtue of the fact that it does not have to pay tax there on either an intra-Community acquisition (first sentence of Article 141) or its supply, because Article 197 prescribes that the recipient of that (second) supply (in the present case, M s. r. o.) becomes the person liable for payment of the VAT (reverse charge to the recipient of the supply). In order for that to be the case, M s. r. o. must, according to Article 141(e) of that directive, have been ‘designated in accordance with Article 197 as liable for payment of the VAT due on the supply’.

41. On the other hand, according to Article 42 of the VAT Directive, VAT is deemed to have been applied to the intra-Community acquisition within the meaning of Article 40 of that directive (that is to say, the acquisition in the Czech Republic). Moreover, the further application of VAT to the intra-Community acquisition (subject to a condition subsequent) under Article 41 of the directive (in the present case, the acquisition in Austria) does not apply. However, under Article 42 of the directive, this is subject to the condition that the person acquiring the goods (in the present case, the applicant) provides certain evidence (point (a)) and submits a recapitulative statement (point (b)). In particular, the applicant must establish that the recipient of the supply (in the present case, M s. r. o.) ‘has been designated in accordance with Article 197 as liable for payment of VAT’.

42. Both simplifications are based on the fact that the recipient of the applicant’s supply has been designated in accordance with Article 197 of the VAT Directive as liable for payment of VAT. In order for that to be the case, paragraph 1 of that provision requires, inter alia, that an invoice be drawn up in accordance with Sections 3 to 5 of Chapter 3 (point (c)), that is to say, that the invoice for the applicant’s supply to M s. r. o. contains a reference to the reverse charge to M s. r. o. in accordance with Article 226(11a) of that directive – which is in Section 4 of Chapter 3.

43. This clearly shows that that simplification measure is available to the intermediate trader (in the present case, the applicant). That trader can avail itself of the simplifications, but is not obliged to do so. Through the content of the invoice to its own customer, it can decide whether to avail itself of the simplification measure. Accordingly, a right of option is conferred on the intermediate trader in question.

3. Importance of the reference to the reverse charge in the context of the intra-Community triangular transaction

44. However, that right of option in favour of the intermediate trader also has an impact on the recipient of the supply. The latter now becomes the person liable for payment of the VAT on the supply made to it and is required to pay the VAT not to its contracting partner, but to the tax authorities in the country of destination.

45. In that respect, it is understandable, if not even inevitable, that Article 226(11a) requires the mention ‘Reverse charge’ on such an invoice. That mention is intended to ensure that the recipient of the supply is aware of his or her tax liability and duly pays the tax on the supply in the country of destination instead of the supplier. An invoice that does not state VAT separately, on the other hand, only indicates that the supplier assumes that he or she is not required to collect VAT. Why he or she assumes that is not clear from such an invoice. The assumption could be based, for example, on the exemption or non-taxability of the transaction. The fact that VAT is not stated does not necessarily entail a reverse charge to the recipient of the supply.

46. As I have already stated elsewhere, one of the purposes served by an invoice – and thus all its details required under Article 226 of the VAT Directive – is to inform the addressee of the invoice of the legal assessment of the transaction (in particular the amount of VAT due and passed on to the addressee of the invoice) of the supplier/issuer of the invoice. That purpose becomes all the more important where the supplier takes the view that, on an exceptional basis, it is not he or she but the recipient of the supply who is liable for the VAT and, therefore, the price was stated without VAT. Without such information, there would be an increased risk of the VAT not being paid by anyone.

47. Therefore, the invoice detail referred to in Article 226(11a) of the VAT Directive is necessary in order that the recipient of the supply can be said to have been ‘designated in accordance with Article 197 as liable for payment of VAT’ (see Article 42(a) and, similarly, Article 141(e) of that directive). The aim of that is to inform the recipient of the supply (addressee of the invoice) and to ensure that the latter pays the VAT in the country of destination.

48. For that reason, the wording ‘Exempt intra-Community triangular transaction’ used by the applicant in the present case may indeed satisfy the requirements of Article 226(11) of the VAT Directive, but it does satisfy the requirements of Article 226(11a) thereof. If the legislature expressly distinguishes between the reference to exemption and the reference to a reverse charge in Articles 226(11) and (11a), that legislative intention must also be taken into account.

49. A broad interpretation according to which the wording ‘Exempt intra-Community triangular transaction’ satisfies the requirements of Article 197 of the VAT Directive because an intra-Community triangular transaction ultimately requires that the recipient of the supply becomes the person liable for payment of the tax at the end of the chain is therefore not possible. Rather, the wording of Article 197 of the VAT Directive, in conjunction with Article 226(11a) thereof, requires an express reference to a reverse charge, but there was no such reference in the present case. That decision by the legislature is binding on the administration and the courts in equal measure.

50. Moreover, it is not disproportionate to require a taxable person such as the applicant to issue an invoice containing that mention if it wishes to avail itself of its right of option and the associated administrative simplification in its favour. The express invoice requirement under Article 197 of the VAT Directive, in conjunction with Article 226(11a) thereof, pursues a legitimate objective (informing the recipient of the supply and the tax administration of the use of the simplification scheme by transferring the tax liability) and is appropriate for achieving that objective. An equally appropriate means of achieving it is not apparent. In view of the low amount of effort required on the part of the applicant, such a formal requirement is also proportionate.

4. Invoice containing a reference to a reverse charge as a condition for exercising the right of option

51. Without such an invoice, it must therefore be assumed that the intermediate trader (in the present case, the applicant) has not exercised its right of option and that the recipient of the supply (in the present case, M s. r. o.) has not been designated in accordance with Article 197 of the VAT Directive as liable for payment of VAT. Consequently, the intra-Community acquisition will not be deemed to be taxed and Article 41 will continue to apply. Therefore, the applicant must pay tax on an intra-Community acquisition in Austria as long as it does not establish that it has paid tax on the acquisition in the Czech Republic. If the conditions for non-application of the ‘normal’ taxation scheme to an intra-Community acquisition that are set out in Article 42(a) of the VAT Directive are not met, use cannot be made of the simplification scheme.

52. Nothing to the contrary follows from the case-law of the Court to date. Rather, in its decision on Article 42 of the VAT Directive, the Court expressly distinguished between the conditions of point (a) and point (b). Point (b) refers to a corresponding tax return (the recapitulative statement). The Court described that as an arrangement that ‘must be regarded as being formal’. However, the relevant condition requiring an invoice referring to a reverse charge (‘for which the person to whom the supply is made has been designated in accordance with Article 197 as liable for payment of VAT’) is prescribed in point (a), which the Court described as a ‘basic condition’.

53. Therefore, the answer to Question 1 is that the person to whom the supply is made is to be regarded as having been designated as liable for payment of VAT within the meaning of Article 197 of the VAT Directive only if the invoice concerned refers to a reverse charge to the recipient of the supply. The mere indication ‘Exempt intra-Community triangular transaction’ is not sufficient in that regard.

C. Issuance of an invoice with retroactive effect in the case of an intra-Community triangular transaction (or in the case where a right of option is exercised)?

54. Consequently, without an invoice referring to a reverse charge to the recipient of the supply, the normal treatment of chain transactions applies. Therefore, the applicant is required to pay tax on an intra-Community acquisition in the Czech Republic (Article 40 of the VAT Directive) and, until it has established that it has done so, it is required to pay tax on an intra-Community acquisition in Austria (Article 41 of the VAT Directive). Likewise, tax on the supply made to M s. r. o. must be paid in the Czech Republic.

55. However, the applicant did not collect the VAT from its contracting partner (M s. r. o.) because it assumed an ‘exempt intra-Community triangular transaction’. Subsequent collection is likely to be unsuccessful due to the impossibility of contacting the recipient of the supply, which has not paid any VAT (either on the supplies made to it or on the supplies made by it).

56. For that reason, the applicant apparently attempted to issue a corrected invoice. Although the precise content of the corrected invoice is not apparent from the order for reference, in its second question the referring court asks, in essence, whether a subsequent correction of the invoice (with retroactive effect) is possible at all.

57. However, I have doubts as to whether one should speak of an invoice correction at all in the context of the present case. As stated above, one of the conditions (that is to say, a corresponding invoice) for assuming an intra-Community triangular transaction and a reverse charge to the recipient of the supply is not met. However, the retrospective fulfilment of a mandatory condition is not a correction, but rather an issuance of the required invoice for the first time.

58. Therefore, the real question is not whether it is possible for an invoice to be corrected retrospectively, but what legal consequences are triggered when an invoice is issued retrospectively – if that is indeed possible. In that respect, the circumstance of whether the applicant had already issued an invoice of any nature or no invoice at all makes no difference to the existence of an intra-Community triangular transaction in the present case.

59. As the VAT Directive does not set a time limit within which use can be made of the simplification scheme, this can still be done subsequently. Therefore, a corresponding invoice can be issued at a later point. Possible time limits result, at best, from national procedural law, but not from the VAT Directive.

60. However, it also follows from the purpose of an invoice as explained above that – if it triggers legal consequences for the recipient of the supply, as in the present case – the recipient of the supply must necessarily receive it. How is the recipient of the supply supposed to know that the supplier has exercised its right of option to make use of the simplification scheme and has designated it as liable for payment of VAT in accordance with Article 197 of the VAT Directive if it is never informed of this?

61. For the same reason, the question as to retroactive effect can be answered quite clearly. Such an issuance of an invoice (for the first time) cannot have retroactive effect. Once such an invoice has been issued, and is received by the recipient, the legal consequences of the administrative simplification scheme are triggered ex nunc.

62. This is in line with a general principle of VAT law according to which changes that are decisive for taxation purposes are legally significant only when they occur.

63. This is made clear by, for example, the second sentence of Article 187(2) of the VAT Directive, which concerns changes to the use of goods. The change does not take place retroactively as a result of an adjustment to the deduction at the time, but only when the goods are used differently from how they were used at the time when the deduction was effected. Even subsequent changes to the purchase price – see Article 90 of the VAT Directive – do not have retroactive effect on the conclusion of the purchase contract (that is to say, on the tax originally due), but are to be taken into account only at the point at which they occur. The same applies in accordance with Article 185 of the VAT Directive to the case where the amount deducted is too high after the purchase price is reduced at a later stage.

64. That approach – whereby, in principle, there is no retroactive effect in the context of general and indirect excise duty – is confirmed by the case-law of the Court concerning the deduction of input tax in accordance with the intended use. Even if taxable transactions are subsequently never made, the deduction made is not corrected with retroactive effect, but remains unaltered. This is clearly shown by the Court’s case-law – which is now more developed – concerning the need to hold an invoice in order to deduct input tax. Accordingly, a retroactive issuance of a (first-time) invoice cannot lead to a retroactive input tax refund.

65. In addition, the recipient’s tax liability cannot be unilaterally and retroactively changed by the supplier. If it were to be assumed that the applicant had consciously proceeded on the basis of a ‘normal’ chain transaction, it would have issued an invoice stating Czech VAT to M s. r. o., received that VAT and paid it in the Czech Republic. Should the applicant then be able to make use of the simplification scheme retroactively by means of a new invoice? The consequence would be that M s. r. o. would retroactively become liable for payment of VAT against its will (and even without its knowledge if it does not receive the invoice) and would have to pay the VAT again (after having already paid it to the applicant) to the tax authorities. If at all, this would be possible only ex nunc and, following payment of the price including VAT, only with the consent of the recipient of the supply.

66. Consequently, it remains the case that the conditions (in the present case: for the use of a simplification scheme) cannot be fulfilled retroactively. Until the corresponding invoice exists, the conditions of the simplification scheme for an intra-Community triangular transaction are not met. Only when the corresponding invoice has been issued can that be said to be the case. Therefore, a correction is possible only ex nunc, and not ex tunc (retroactively).

67. By contrast, in so far as reference is made to the case-law of the Court concerning the ex tunc correction of an invoice, this comes to nothing. On the one hand, that case-law concerned the deduction of input tax and not the exercise of a right of option linked to a specific invoice.

68. On the other hand, in those cases the Court ‘only’ held that the tax authority cannot refuse the right to deduct VAT on the sole ground, for example, that an invoice does not satisfy the conditions required by Article 226(6) and (7) of the VAT Directive (precise description of the quantity and nature of supply and date of the supply) if they have available all the information to ascertain whether the substantive conditions for that right are satisfied. The same applies to the information mentioned in Article 226(3) (supplier’s VAT ID) or Article 226(2) (invoice number). It was only in that respect that the Court ascribed retroactive effect to the correction of a (formally incorrect) invoice already held by the recipient of the supply.

69. This is convincing in the context of the deduction of input tax. A document that charges for a supply of goods or services is in fact an invoice within the meaning of Article 178(a) of the VAT Directive if it enables both the recipient of the supply and the tax authorities to establish which supplier has passed on to which recipient of the supply which amount in VAT for which transaction, and when it has done so. That means it needs to state the supplier, the recipient of the supply, the goods or services supplied, the price and the VAT, which must be stated separately. As I have already stated elsewhere, if those five essential items of information are provided, the spirit and purpose of the invoice in the context of the deduction of input tax are fulfilled and the right of deduction ultimately arises.

70. However, as stated above, a reference to a reverse charge is a necessary condition for an intra-Community triangular transaction (see point 44 et seq. above). It is only by virtue of that reference that the recipient of the supply knows that it is liable for the tax. It is only with such a reference that the tax authorities can check whether the simplification scheme applies and that the supplier can avoid having to register in the country of destination with a clear conscience. The existence of those required items of information and their effects cannot be established with retroactive effect.

71. Therefore, the answer to the second question is that an invoice containing the mention ‘Reverse charge’ can be issued subsequently, but only with ex nunc effect, whereby it is necessary that that invoice is received by the recipient of the supply.

D. The content of the correction and the relevant national rules for invoices

72. By its third question, the referring court seeks an interpretation of Article 219a of the VAT Directive. That provision determines according to which rules of which Member State an invoice is to be issued. Since it has been established that the invoice is so defective that there is no intra-Community triangular transaction, this question can arise in respect of the present dispute in the main proceedings only if an invoice could still be issued with retroactive effect. As stated above, that is not the case, with the result that the question need not be answered.

73. The position is similar with respect to Question 2(a). In that question, the referring court seeks to ascertain whether the mention ‘Intra-Community triangular transaction in accordance with Article 25 of [the UStG]. Liability for payment of VAT is transferred to the customer’ is sufficient. On the one hand, this also presupposes that it is possible for an invoice to be corrected with retroactive effect. On the other hand, the specific content of the invoice results from national law (see Article 219a of the VAT Directive). However, the Court cannot assess national law. The Court cannot rule on the question as to whether the applicant must in fact cite Article 25 of the UStG in an invoice.

74. Moreover, the only invoice details which the Member States can in principle require result from Article 226 of the VAT Directive. It follows from Article 226(11) of the VAT Directive that reference must be made to exemption if a supply of goods or service is exempt. Unlike Article 2(1) of the VAT Directive, which distinguishes between a supply of goods (point (a)), a supply of services (point (c)) and an intra-Community acquisition (point (b)), Article 226(11) does not refer to an intra-Community acquisition. As evidenced by Article 42 of that directive, the intra-Community acquisition is also not exempt, but VAT is deemed to have been applied to it, without Article 41 of the directive being applicable.

75. It follows from Article 226(11a) of the VAT Directive that, where the customer is liable for the payment of the VAT, the mention ‘Reverse charge’ is required. The wording ‘Liability for payment of VAT is transferred to the customer’ expresses the same thing. A reference to the basis on which that transfer of liability for payment of VAT is based – under national law or EU law – is helpful (see Article 226(11) of the VAT Directive) but not mandatory. It follows from the comparison between Article 226(11) and (11a) of the VAT Directive that it is not necessary to indicate the basis of the reverse charge. The only decisive factor is that the recipient of the supply knows that the supplier assumes that the recipient of the supply is liable for the tax and must pay it in the country of destination.

Copyright – internationaltaxplaza.info