On February 16, 2023 on the website of the Court of Justice of the European Union (CJEU) the judgment of the CJEU in Case C-519/21, ASA versus DGRFP Cluj (with joined parties BP and MB), ECLI:EU:C:2023:106, was published.

This request for a preliminary ruling concerns the interpretation of Council Directive 2006/112/EC of 28 November 2006 on the common system of value added tax (OJ 2006 L 347, p. 1; ‘the VAT Directive’) and the principles of proportionality, fiscal neutrality and legal certainty.

The request has been made in proceedings between ASA, a natural person, and the Direcția Generală Regională a Finanțelor Publice Cluj-Napoca (Regional Directorate-General of Public Finance, Cluj-Napoca, Romania; ‘the tax authorities’) concerning the imposition of value added tax (VAT) on transactions for the sale of apartments.

The dispute in the main proceedings and the questions referred for a preliminary ruling

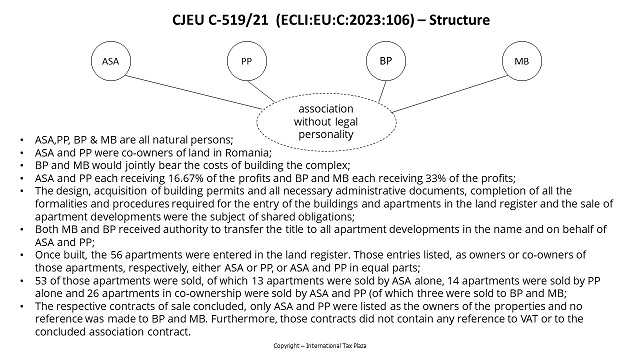

23 The sisters ASA and PP were co-owners of land in Romania.

24 At the end of 2006, they entered into a contract relating to an association without legal personality with BP and MB, two other natural persons, with a view to the construction of a building complex consisting of eight residential properties with 56 apartments, intended for sale to third parties.

25 The association contract provided in particular that BP and MB would jointly bear the costs of building the complex, with ASA and PP each receiving 16.67% of the profits and BP and MB each receiving 33% of the profits.

26 In addition, under the terms of that association contract, the design, acquisition of building permits and all necessary administrative documents, completion of all the formalities and procedures required for the entry of the buildings and apartments in the land register and the sale of apartment developments were the subject of shared obligations.

27 Finally, both MB and BP received authority to transfer the title to all apartment developments in the name and on behalf of ASA and PP.

28 Once built, the 56 apartments were entered in the land register. Those entries listed, as owners or co-owners of those apartments, respectively, either ASA or PP, or ASA and PP in equal parts.

29 Over the period from 13 May 2008 to 28 November 2008, 53 of those apartments were sold, of which 13 apartments were sold by ASA alone, 14 apartments were sold by PP alone and 26 apartments in co-ownership were sold by ASA and PP (of which three were sold to BP and MB).

30 In the respective contracts of sale concluded, only ASA and PP were listed as the owners of the properties and no reference was made to BP and MB. Furthermore, those contracts did not contain any reference to VAT or to the concluded association contract.

31 Following a tax inspection, the tax authorities issued, on 26 October 2011, a tax notice against ASA declaring the latter liable for RON 537 287 (approximately EUR 109 000) in VAT and for RON 482 269 (approximately EUR 98 000) in interest and penalties for late payment.

32 The tax authorities took the view that, in 2008, ASA, alone or jointly with PP, had carried out an economic activity for the purpose of obtaining income therefrom. In particular, it considered that the sales made as part of that activity were transactions subject to VAT and that she could therefore be classified as a taxable person under national law. In addition, since the sum received by ASA and PP in the sales at issue exceeded the VAT exemption threshold laid down in Article 152(1) of the Tax Code, ASA and PP should have identified themselves as being liable for VAT on 1 July 2008. The tax authorities thus concluded that ASA was liable for the VAT applicable to those sales after that date.

33 In order to reach those findings, the tax authorities relied on the association contract, since it was not formally registered and was presented to it only at the beginning of the tax inspection.

34 The complaint lodged by ASA against that tax notice was rejected by the tax authorities in 2012.

35 ASA brought an action at first instance before the Curtea de Apel Cluj (Court of Appeal, Cluj, Romania), the referring court, seeking, principally, the annulment of the decision rejecting the complaint and of the tax notice. In 2014, in the context of those proceedings, ASA sought to have BP and MB joined as third parties, so that, if she were unsuccessful, they would have to pay an amount equal to two thirds of the VAT claim brought against her by the tax notice.

36 By judgment of 28 January 2016, that court partially upheld ASA’s action and partially annulled the decision rejecting the complaint, the tax notice and the related tax inspection report, on the basis of the method used to calculate the VAT and related charges.

37 By judgment handed down in 2016, the Înalta Curte de Casație și Justiție (High Court of Cassation and Justice, Romania) upheld the appeals brought by ASA and the tax authorities against that judgment of 28 January 2016 and referred the case back to the referring court for re-examination.

38 By judgment of 14 March 2019, the referring court partially upheld ASA’s action against the tax authorities, by partially annulling the decision rejecting the complaint, the tax notice and the related tax inspection report, taking the view that the price agreed in the transactions with ASA already included VAT.

39 ASA and the tax authorities appealed against that judgment.

40 By judgment of 23 July 2020, the Înalta Curte de Casație și Justiție set aside that judgment and again referred the case back to the referring court for re-examination.

41 In that regard, the referring court states at the outset that, in the dispute in the main proceedings, the determination that, first, ASA is a taxable person and, secondly, the economic activity carried out by ASA, alone or jointly with PP, is a transaction subject to VAT, has acquired the force of res judicata.

42 In that context, the referring court seeks to ascertain, first, whether BP and MB also have the status of taxable persons in regard to the transactions relating to the sale of the apartments at issue in the main proceedings.

43 That court notes that only ASA and PP participated in the chargeable event for VAT, by means of sales, by supplying the goods and collecting the price. In addition, it states that the participation of BP and MB was essential for the construction of the eight buildings and, therefore, for the economic activity as such.

44 In that regard, the referring court considers that, since the tax authorities took into account the association contract in order to justify the taxation of ASA, they could not claim that they were unaware of the provisions of that contract on the pretext that it had not been registered for tax purposes before the economic activity commenced and that that contract did not comply with the formal requirements laid down in Article 86(2) of the Tax Code. Furthermore, the view could be taken, in the light of the judgment of 9 April 2013, Commission v Ireland (C‑85/11, EU:C:2013:217), that the persons referred to in Article 11 of the VAT Directive need not individually satisfy the definition of a taxable person set out in Article 9(1) of that directive, since the relationship between those two provisions appears to allow persons, taken together and closely bound to one another by financial, economic and organisational links, to satisfy collectively that definition. In other words, by failing to take into account the association contract, it may present a tax situation that does not correspond to the actual situation. Therefore, in the light of the judgments of 15 July 2010, Pannon Gép Centrum (C‑368/09, EU:C:2010:441, paragraph 43), and of 8 May 2013, Petroma Transports and Others (C‑271/12, EU:C:2013:297, paragraph 34), the decisive question should be whether the tax authorities were aware of that association contract before the tax notice was issued.

45 Second, the national court is unsure to what extent the right to deduct should be granted to a person in ASA’s situation. Relying on the case-law of the Court of Justice, the referring court first finds that ASA could not be denied the right to deduct VAT charged on the investment transactions carried out for the purposes of the association’s activities, including the VAT corresponding to the invoices issued in the names of BP, MB and PP, on the sole ground that ASA was not liable for tax and did not personally pay the input VAT on goods and services used in connection with the transactions at issue in the main proceedings. However, that court considers that, as regards the input VAT paid by PP, ASA could be denied the right to deduct VAT on the ground that PP was herself subject to taxation, meaning that she should be recognised as having the right to deduct the input VAT paid.

46 Furthermore, the referring court also relies on the judgment of 21 November 2018, Vădan (C‑664/16, EU:C:2018:933, paragraph 44), in which the Court of Justice held that the taxable person is required to provide objective evidence that goods and services were actually provided to it as inputs by taxable persons for the purposes of its own transactions subject to VAT, in respect of which it has actually paid VAT. It follows that ASA was not in a position to deduct VAT on the input invoices issued in the name of PP, given that she had herself invoked the right to deduct in court and that that right cannot be exercised twice. As regards the VAT corresponding to the invoices issued in the names of BP and MB, that court assumes that the VAT could not be deducted by ASA either, since ASA did not pay input VAT and BP and MB were not taxable persons.

47 Third, the referring court expresses doubts as to whether it is possible for ASA to have BP and MB joined as third parties so that they have to bear the VAT paid in proportion to their rights to the profits provided for in the association contract. It notes that third-party proceedings of that kind, once held to be well founded, could result in the tax notice being amended, thereby depriving BP and MB of the rights conferred on them by the Codul de procedură fiscală (Tax Procedure Code) in the event of a direct action by the tax authorities against them.

48 In those circumstances, the Curtea de Apel Cluj (Court of Appeal, Cluj) decided to stay the proceedings and to refer the following questions to the Court of Justice for a preliminary ruling:

‘(1) Can [the VAT Directive] in general, and Articles 9, 12, 14, 62, 63, 65, 73 and 78 in particular, be interpreted, in a specific context such as that of the dispute in the main proceedings, as meaning that, as regards the occurrence of the chargeable event in the case of taxable transactions involving the supply of immovable property and the method for determining the relevant taxable amount, natural persons who are parties to a contract relating to an association without legal personality concluded with the taxable person liable for tax on output transactions which it should have collected, also have the status of taxable person since the association contract was not registered with the tax authorities before the activity commenced but was presented to them before the administrative acts relating to taxation were issued?

(2) Can [the VAT Directive] in general, and [Article 167, Article 168(a), Article 178(a) and Article 179] in particular, and the principles of proportionality and neutrality, be interpreted, in a specific context such as that of the dispute in the main proceedings, as:

(a) recognising the possibility of conferring the right of deduction on a taxable person, where [that taxable person] does not owe tax or has not paid personally the input VAT on goods and services used in connection with the taxable transactions, and the VAT is due/paid at the preceding stage by natural persons in respect of whom the status of taxable persons has not been established, but who are parties to a contract relating to an association without legal personality concluded with the taxable person liable for tax on output transactions which [that taxable person] should have collected, since the association contract was not registered with the tax authorities before the activity commenced

(b) recognising the possibility of conferring the right of deduction on a taxable person, in a specific context such as that of the dispute in the main proceedings, where [that taxable person] does not owe tax or has not paid personally the input VAT on goods and services used in connection with the taxable transactions, and the VAT is due/paid at the preceding stage by a natural person in respect of whom the status of taxable person has been established, who is party to a contract relating to an association without legal personality and who, together with the taxable person, intends also to exercise, or could exercise, his [or her] own right of deduction, and the latter are liable for tax on output transactions which they should have collected, since the association contract was not registered with the tax authorities before the activity commenced?

(3) In the event that the answer to the questions is in the negative and/or in the light of the principle of legal certainty: is a claim by the taxable person, which is liable for VAT and related charges, admissible against natural persons in respect of whom the status of taxable persons has not been established and who are parties to a contract relating to an association without legal personality concluded with the taxable person liable for tax on output transactions which [that taxable person] should have collected, since the association contract was not registered with the tax authorities before the activity commenced, in order to obtain the proportion of tax which was laid down for the distribution of profits accruing to those persons under the association contract in relation to the liability for VAT and related charges imposed on the taxable person?’

Judgment

The CJEU (Seventh Chamber) ruled as follows:

- Articles 9 and 11 of Council Directive 2006/112/EC of 28 November 2006 on the common system of value added tax must be interpreted as meaning that the parties to a contract relating to an association without legal personality, which was not registered with the competent tax authorities before the economic activity concerned commenced, cannot be regarded as ‘taxable persons’ along with the taxable person which is liable for tax on the taxable transaction.

- Directive 2006/112, the principle of proportionality and the principle of fiscal neutrality must be interpreted as meaning that a taxable person, where it does not hold an invoice issued in its name, must be granted the right to deduct the input value added tax paid by another party to an association without legal personality with a view to carrying out that association’s economic activity, even if the taxable person is liable in respect of that activity, where there is no objective evidence that the goods and services at issue in the main proceedings were actually provided as inputs by taxable persons for the purposes of its own transactions subject to value added tax.

Legal context

European Union law

3 Pursuant to the second subparagraph of Article 1(2) of the VAT Directive:

‘On each transaction, VAT, calculated on the price of the goods or services at the rate applicable to such goods or services, shall be chargeable after deduction of the amount of VAT borne directly by the various cost components.’

4 Article 9(1) of that directive provides:

‘“Taxable person” shall mean any person who, independently, carries out in any place any economic activity, whatever the purpose or results of that activity.

Any activity of producers, traders or persons supplying services, including mining and agricultural activities and activities of the professions, shall be regarded as “economic activity”. The exploitation of tangible or intangible property for the purposes of obtaining income therefrom on a continuing basis shall in particular be regarded as an economic activity.’

5 Article 11 of that directive states:

‘After consulting the advisory committee on value added tax …, each Member State may regard as a single taxable person any persons established in the territory of that Member State who, while legally independent, are closely bound to one another by financial, economic and organisational links.

A Member State exercising the option provided for in the first paragraph may adopt any measures needed to prevent tax evasion or avoidance through the use of this provision.’

6 Article 12 of the VAT Directive provides:

‘1. Member States may regard as a taxable person anyone who carries out, on an occasional basis, a transaction relating to the activities referred to in the second subparagraph of Article 9(1) and in particular one of the following transactions:

(a) the supply, before first occupation, of a building or parts of a building and of the land on which the building stands;

(b) the supply of building land.

2. For the purposes of paragraph 1(a), “building” shall mean any structure fixed to or in the ground.

Member States may lay down the detailed rules for applying the criterion referred to in paragraph 1(a) to conversions of buildings and may determine what is meant by “the land on which a building stands”.

Member States may apply criteria other than that of first occupation, such as the period elapsing between the date of completion of the building and the date of first supply, or the period elapsing between the date of first occupation and the date of subsequent supply, provided that those periods do not exceed five years and two years respectively.

3. For the purposes of paragraph 1(b), “building land” shall mean any unimproved or improved land defined as such by the Member States.’

7 Pursuant to Article 14(1) of the VAT Directive:

‘“Supply of goods” shall mean the transfer of the right to dispose of tangible property as owner.’

8 Article 62 of that directive provides:

‘For the purposes of this Directive:

(1) “chargeable event” shall mean the occurrence by virtue of which the legal conditions necessary for VAT to become chargeable are fulfilled;

(2) VAT shall become “chargeable” when the tax authority becomes entitled under the law, at a given moment, to claim the tax from the person liable to pay, even though the time of payment may be deferred.’

9 Under Article 63 of that directive:

‘The chargeable event shall occur and VAT shall become chargeable when the goods or the services are supplied.’

10 Article 65 of that directive provides:

‘Where a payment is to be made on account before the goods or services are supplied, VAT shall become chargeable on receipt of the payment and on the amount received.’

11 Article 73 of the VAT Directive states:

‘In respect of the supply of goods or services, other than as referred to in Articles 74 to 77, the taxable amount shall include everything which constitutes consideration obtained or to be obtained by the supplier, in return for the supply, from the customer or a third party, including subsidies directly linked to the price of the supply.’

12 Article 78 of that directive is worded as follows:

‘The taxable amount shall include the following factors:

(a) taxes, duties, levies and charges, excluding the VAT itself;

(b) incidental expenses, such as commission, packing, transport and insurance costs, charged by the supplier to the customer.

For the purposes of point (b) of the first paragraph, Member States may regard expenses covered by a separate agreement as incidental expenses.’

13 Under Article 167 of that directive:

‘A right of deduction shall arise at the time the deductible tax becomes chargeable.’

14 Article 168 of that directive states:

‘In so far as the goods and services are used for the purposes of the taxed transactions of a taxable person, the taxable person shall be entitled, in the Member State in which he carries out these transactions, to deduct the following from the VAT which he is liable to pay:

(a) the VAT due or paid in that Member State in respect of supplies to him of goods or services, carried out or to be carried out by another taxable person;

…’

15 Article 178 of the VAT Directive states:

‘In order to exercise the right of deduction, a taxable person must meet the following conditions:

(a) for the purposes of deductions pursuant to Article 168(a), in respect of the supply of goods or services, he must hold an invoice drawn up in accordance with Articles 220 to 236 and Articles 238, 239 and 240;

…’

16 Article 179 of that directive provides:

‘The taxable person shall make the deduction by subtracting from the total amount of VAT due for a given tax period the total amount of VAT in respect of which, during the same period, the right of deduction has arisen and is exercised in accordance with Article 178.

However, Member States may require that taxable persons who carry out occasional transactions, as defined in Article 12, exercise their right of deduction only at the time of supply.’

17 Under Article 226 of that directive:

‘Without prejudice to the particular provisions laid down in this Directive, only the following details are required for VAT purposes on invoices issued pursuant to Articles 220 and 221:

(1) the date of issue;

(2) a sequential number, based on one or more series, which uniquely identifies the invoice;

(3) the VAT identification number referred to in Article 214 under which the taxable person supplied the goods or services;

(4) the customer’s VAT identification number, as referred to in Article 214, under which the customer received a supply of goods or services in respect of which he is liable for payment of VAT, or received a supply of goods as referred to in Article 138;

(5) the full name and address of the taxable person and of the customer;

(6) the quantity and nature of the goods supplied or the extent and nature of the services rendered;

(7) the date on which the supply of goods or services was made or completed or the date on which the payment on account referred to in points (4) and (5) of Article 220 was made, in so far as that date can be determined and differs from the date of issue of the invoice;

(8) the taxable amount per rate or exemption, the unit price exclusive of VAT and any discounts or rebates if they are not included in the unit price;

(9) the VAT rate applied;

(10) the VAT amount payable, except where a special arrangement is applied under which, in accordance with this Directive, such a detail is excluded;

…’

Romanian law

18 Article 86(2) to (5) of Legea nr. 571/2003 privind Codul fiscal (Law No 571/2003 establishing the Tax Code) (Monitorul Oficial al României, Part I, No 927 of 23 December 2003), in the version applicable to the main proceedings (‘the Tax Code’), provided:

‘(2) The members of any association without legal personality formed in accordance with the law shall, when the activity commences, conclude written association contracts containing, inter alia, the following information:

(a) the contracting parties;

(b) the objects and registered office of the association;

(c) the assets and rights contributed by the members;

(d) the percentage of each member’s share in the association’s profits or losses commensurate with its contribution;

(e) the designation of the member responsible for fulfilling the association’s obligations towards the public authorities;

(f) the conditions for termination of the association. Contributions made by members in accordance with the association contract shall not be regarded as income of the association. The association contract shall be registered with the competent tax authorities within 15 days from the date of its conclusion. The tax authorities shall have the right to refuse to register a contract if it does not contain the information required under this paragraph.

(3) Where there are family ties up to and including the fourth degree between the members of the association, the parties must prove that they are involved in making a profit from assets or rights belonging to them. Members of an association may also be natural persons with limited capacity.

(4) Associations shall submit to the competent tax authorities, by 15 March of the following year at the latest, an annual income statement in accordance with the model drawn up by the Ministry of Public Finances, including a breakdown of net profits/losses by member.

(5) The annual profits/losses of the association shall be distributed to the members in proportion to the percentage share commensurate with their contribution, pursuant to the association contract.’

19 Pursuant to Article 1251(1) of the Tax Code:

‘Pursuant to this Title, the following terms and expressions shall have the following meaning:

…

18 “taxable person” shall have the same meaning as under Article 127(1) and shall refer to a natural person, a group of persons, a public institution, a legal person and any entity capable of carrying out an economic activity;

…’

20 Article 127(8) and (9) of the Tax Code states:

‘(8) A group of taxable persons established in Romania, which are legally independent but have close organisational, financial and economic links with each other, shall be regarded as a single taxable person, subject to the conditions and limits set out in the implementing rules.

(9) Any member or partner of an association or organisation without legal personality shall be regarded as a separate taxable person in respect of any economic activity not carried out in the name of that association or organisation.’

21 Under Article 152(1) of that code:

‘A taxable person established in Romania whose annual turnover, declared or achieved, is below the threshold of EUR 35 000, the equivalent of which in [Romanian lei (RON)] shall be set according to the exchange rate provided by the Banca Națională a României [(National Bank of Romania)] on the date of accession and rounded to the nearest thousandth, may apply the exemption from taxation, referred to hereinafter as the “special exemption scheme”, to operations pursuant to Article 126(1), excluding intra-community supplies of new means of transport, which are exempted in accordance with Article 143(2)(b).’

22 The Hotărârea Guvernului nr. 44/2004 pentru aprobarea Normelor metodologice de aplicare a Legii nr. 571/2003 privind Codul fiscal (Government Decision No 44/2004 approving the detailed rules for the implementation of Law No 571/2003 establishing the Tax Code) (Monitorul Oficial al României, Part I, No 112 of 6 February 2004), in the version applicable to the main proceedings (‘Government Decision No 44/2004), provided, in paragraph 4, which was adopted pursuant to Article 127 of the Tax Code:

‘(1) For the purposes of Article 127(8) of the Tax Code, a group of taxable persons established in Romania, which are legally independent but have close organisational, financial and economic links, may choose to be treated as a single taxable person (“tax group”), subject to the following conditions:

(a) a taxable person may belong only to one single tax group; and

(b) the option must cover a period of at least two years; and

(c) all taxable persons in the group must file for the same tax period.

(2) The tax group may consist of two to five taxable persons.

(3) Until 1 January 2009, a tax group may consist only of taxable persons which are regarded as large taxpayers.

(4) Taxable persons shall be regarded as having close organisational, financial and economic links within the meaning of paragraph (1) in the case where more than 50% of their capital is held, directly or indirectly, by the same shareholders.

(5) An application to form a tax group must be submitted to the competent tax authorities, signed by all the members of the group, and contain the following information:

(a) the name, address, objects and VAT number of each member;

(b) evidence that the members are closely linked within the meaning of paragraph (2);

(c) the name of the member appointed to be the representative.

(6) The competent tax authorities shall adopt an official decision approving or denying the formation of the tax group and shall communicate that decision to the group representative and to each tax authority in the territory of which the members of the tax group are situated within 60 days of receipt of the application referred to in paragraph (5).

(7) The formation of the tax group shall take effect on the first day of the second month following the date of the decision referred to in paragraph (6).

…’

The request for an expedited procedure

49 The referring court has requested that the Court deal with the present request for a preliminary ruling under the expedited procedure set out in Article 105(1) of the Rules of Procedure of the Court of Justice. In support of its request, that court stated that the dispute in the main proceedings has been pending before the national courts since 2 July 2012.

50 Article 105(1) of the Rules of Procedure provides that, at the request of the referring court or, exceptionally, of his or her own motion, the President of the Court may decide, after hearing the Judge-Rapporteur and the Advocate General, that a reference for a preliminary ruling is to be determined pursuant to an expedited procedure where the nature of the case requires that it be dealt with within a short time.

51 It must be borne in mind that such an expedited procedure is a procedural instrument intending to address matters of an exceptional urgency (judgment of 16 June 2022, Port de Bruxelles and Région de Bruxelles-Capitale, C‑229/21, EU:C:2022:471, paragraph 40 and the case-law cited).

52 Accordingly, the fact that the referring court is required to do everything possible to ensure that the case in the main proceedings is resolved swiftly is not in itself sufficient to justify the use of the expedited procedure under Article 105(1) of the Rules of Procedure (judgment of 14 July 2022, CC (Transfer of a child’s habitual residence to a third country), C‑572/21, EU:C:2022:562, paragraph 22 and the case-law cited).

53 Moreover, the uncertainty affecting the parties to a dispute over several years and their (legitimate) interest in knowing as quickly as possible the scope of the rights that they derive from EU law are not likely to constitute, in view of the fact that the accelerated procedure is used as a derogation, an exceptional circumstance that could justify the application of such a procedure (see, to that effect, order of the President of the Court of 19 September 2017, Magamadov, C‑438/17, not published, EU:C:2017:723, paragraph 21 and the case-law cited).

54 In the present case, by decision of 4 November 2021, the President of the Court, after hearing the Judge-Rapporteur and the Advocate General, rejected the application for an expedited procedure to be applied to the present case.

55 The interest, however important and legitimate, of individuals in having the scope of the rights that they derive from EU law determined as quickly as possible does not imply that the case in the main proceedings must be dealt with within a short time within the meaning of Article 105(1) of the Rules of Procedure.

From the considerations of the Court

Preliminary observations

56 As a preliminary point, it is appropriate to determine whether, for VAT purposes, the various transactions relating to the construction of a building complex and the sale of the completed apartments, carried out on the basis of an association contract, must be treated as distinct transactions which are taxable separately or as single complex transactions, composed of several elements.

57 In that regard, it is clear from the Court’s case-law that, where a transaction comprises a bundle of elements and acts, regard must be had to all the circumstances in which the transaction in question takes place in order to determine whether that operation gives rise, for the purposes of VAT, to two or more distinct supplies or to one single supply (judgment of 4 September 2019, KPC Herning, C‑71/18, EU:C:2019:660, paragraph 35 and the case-law cited).

58 The Court has also held, first, that it follows from the second subparagraph of Article 1(2) of the VAT Directive that every transaction must normally be regarded as distinct and independent and, second, that a transaction which comprises a single supply from an economic point of view should not be artificially split, so as not to distort the functioning of the VAT system (judgment of 4 September 2019, KPC Herning, C‑71/18, EU:C:2019:660, paragraph 36 and the case-law cited).

59 Accordingly, in certain circumstances, several formally distinct services, which could be supplied separately and thus give rise, separately, to taxation or exemption, must be considered to be a single transaction when they are not independent (judgment of 4 September 2019, KPC Herning, C‑71/18, EU:C:2019:660, paragraph 37 and the case-law cited).

60 A supply must be regarded as a single supply where two or more elements or acts supplied by the taxable person are so closely linked that they form, objectively, a single, indivisible economic supply, which it would be artificial to split. That is also the case where one or more supplies constitute a principal supply and the other supply or supplies constitute one or more ancillary supplies which share the tax treatment of the principal supply. In particular, a supply must be regarded as ancillary to a principal supply if it does not constitute, for customers, an end in itself but a means of better enjoying the principal service supplied (judgment of 4 September 2019, KPC Herning, C‑71/18, EU:C:2019:660, paragraph 38 and the case-law cited).

61 However, there is no absolute rule for determining the extent of a service for VAT purposes and, in order to determine the extent of a service, all the circumstances in which the transaction concerned takes place must, therefore, be taken into account (judgment of 4 September 2019, KPC Herning, C‑71/18, EU:C:2019:660, paragraph 39 and the case-law cited).

62 In the context of the cooperation established by Article 267 TFEU, in order to determine whether a commercial transaction comprises several independent services or a single service for the purposes of VAT, it is for the national court to examine the characteristic elements of the transaction concerned, taking into account the economic objective of that transaction and the interests of the recipients thereof and making all definitive findings of fact in that regard (see, to that effect, judgment of 18 October 2018, Volkswagen Financial Services (UK), C‑153/17, EU:C:2018:845, paragraphs 32 and 33 and the case-law cited).

63 In the present case, it is apparent from the order for reference that the transaction at issue in the main proceedings consisted of the construction of a complex of residential properties for the purpose of selling the completed apartments to third parties.

64 In the first place, it is apparent from the documents before the Court that ASA and PP participated in that transaction by contributing a piece of land of which each held half, whereas BP and MB supplied building materials and bore the expenses relating to the construction of the building complex for which each provided half, including the expenses incurred with a view to obtaining the necessary administrative documents. Consequently, BP and MB had invoices drawn up in their names for the goods and services acquired with a view to the construction of the complex at issue in the main proceedings.

65 In the second place, in accordance with the association contract, the sale of the completed immovable properties formed part of the common obligations of the contracting parties. As is also apparent from the documents before the Court, first, under the contracts of sale concluded by notarial acts, the owners of the immovable property at issue in the main proceedings were ASA and PP, without any mention being made in the contracts of BP and MB or of the association contract. Second, BP and MB acted under authorisation to transfer, in the name and on behalf of ASA and PP, to the persons of their choice and at the price agreed with the purchaser, the property rights which ASA and PP held over the apartments in question.

66 In so far as the transactions relating, on the one hand, to the construction of the building complex at issue in the main proceedings and, on the other hand, to the sale of the immovable property appear to have distinct characters, since each of them has its own economic characteristic and cannot be regarded as the principal – or ancillary – characteristic of the other, they must be treated as distinct transactions which are taxable separately, this being nevertheless a matter for the referring court to determine in the light of the facts in the main proceedings.

The first question

67 By its first question, the referring court asks, in essence, whether Articles 9 and 11 of the VAT Directive must be interpreted as meaning that the parties to a contract relating to an association without legal personality, which was not registered with the competent tax authorities before the economic activity concerned commenced, must be regarded as ‘taxable persons’ along with the taxable person liable for tax on the taxable transaction.

68 As regards, in the first place, Article 9(1) of that directive, it must be borne in mind that that provision defines the concept of ‘taxable person’ as meaning ‘any person who, independently, carries out in any place any economic activity, whatever the purpose or results of that activity’.

69 According to settled case-law of the Court, the terms used in Article 9 of the VAT Directive, in particular the term ‘any person who’, give to the notion of ‘taxable person’ a broad definition focused on independence in the pursuit of an economic activity, to the effect that all persons – natural or legal, both public and private, and entities devoid of legal personality – who, in an objective manner, satisfy the criteria set out in that provision must be regarded as being taxable persons for the purposes of VAT (judgment of 16 September 2020, Valstybinė mokesčių inspekcija (Joint activity agreement), C‑312/19, EU:C:2020:711, paragraph 39 and the case-law cited).

70 In order to determine who, in circumstances such as those at issue in the main proceedings, must be regarded in respect of the supplies at issue as a ‘taxable person’ for the purposes of VAT, it is necessary to establish who has independently carried out the economic activity referred to. The criterion of independence concerns allocation of the transaction concerned to a particular person or entity, whilst also guaranteeing that the customer can exercise any right of deduction with legal certainty (judgment of 16 September 2020, Valstybinė mokesčių inspekcija (Joint activity agreement), C‑312/19, EU:C:2020:711, paragraph 40).

71 To that end, it is necessary to examine whether the person concerned carries out an economic activity in his or her own name, on his or her own behalf and under his or her own responsibility, and whether he or she bears the economic risk associated with the carrying out of those activities (judgment of 16 September 2020, Valstybinė mokesčių inspekcija (Joint activity agreement), C‑312/19, EU:C:2020:711, paragraph 41 and the case-law cited).

72 In the present case, it is ultimately for the national court, which has sole jurisdiction to assess the facts, to determine, in the light of the considerations set out in paragraphs 56 to 60 above, whether BP and MB must be regarded as ‘independently’ carrying out an economic activity in the light of the association contract at issue in the main proceedings.

73 However, the Court, which is called on to provide answers of use to the referring court, may provide guidance, based on the case file in the main proceedings and on the written observations that have been submitted to it, in order to enable the national court to give judgment in the particular case pending before it (see, by analogy, judgment of 17 December 2020, WEG Tevesstraße, C‑449/19, EU:C:2020:1038, paragraph 31).

74 As regards the taxable transaction at issue in the main proceedings, namely the supply of immovable property, it is true, as has been pointed out in paragraph 65 of the present judgment, that the sale of the completed apartments formed part, under the association contract, of the common obligations of the contracting parties.

75 However, first, it follows from the order for reference that the contracts of sale concluded by notarial acts stipulated that the profits from the sale were intended to form part of the assets of ASA and PP as owners of the immovable property at issue in the main proceedings, without any mention being made in those contracts of BP and MB or of the association contract.

76 On the other hand, although, as is apparent from the order for reference, BP and MB acted under authorisation to transfer, in the name and on behalf of ASA and PP, to the persons of their choice and at the price agreed with the purchaser, the property rights which ASA and PP held over the apartments in question, the fact remains that the legal effects of the contracts of sale concluded by one of the agents with a third party concerned only ASA and PP, since the supply of the immovable property was carried out solely on the basis of the sales contracts and not on the basis of the promises of sale concluded by MB in his own name as agent for ASA and PP.

77 It follows that BP and MB cannot be regarded, so far as the supply of the immovable property is concerned, as having independently carried out an economic activity in accordance with Article 9(1) of the VAT Directive, with the result that they are not ‘taxable persons’ within the meaning of that provision.

78 In the second place, it is necessary to ascertain whether the parties to an association contract such as the one at issue in the main proceedings must be regarded as a single taxable person within the meaning of Article 11 of the VAT Directive.

79 In that regard, the first paragraph of Article 11 of the VAT Directive provides that each Member State may regard as a single taxable person any persons established in its territory who, while legally independent, are closely bound to one another by financial, economic and organisational links, while the second paragraph of Article 11 specifies that a Member State exercising that option may adopt any measures needed to prevent tax evasion or avoidance through the use of that provision.

80 By that provision, the EU legislature intended, either in the interests of simplifying administration or with a view to combating abuses such as, for example, the splitting-up of one undertaking among several taxable persons so that each might benefit from a special scheme, to ensure that Member States would not be obliged to treat as taxable persons those whose ‘independence’ is purely a legal technicality (judgment of 15 April 2021, Finanzamt für Körperschaften Berlin, C‑868/19, not published, EU:C:2021:285, paragraph 35 and the case-law cited).

81 Treatment as a single taxable person under the first paragraph of Article 11 of the VAT Directive precludes persons who are thus closely linked from continuing to submit VAT declarations separately and from continuing to be identified, within and outside their group, as taxable persons, since the single taxable person alone is authorised to submit such declarations (judgment of 15 April 2021, Finanzamt für Körperschaften Berlin, C‑868/19, not published, EU:C:2021:285, paragraph 36 and the case-law cited).

82 In the present case, the Romanian Government submits that the national legislature did not exercise the option available to Member States under Article 11 of the VAT Directive and that, therefore, that provision does not apply to the dispute in the main proceedings. The Commission, for its part, states that, under Romanian law, until 1 January 2009, the possibility of forming a group as referred to in that provision was open only to large taxpayers, to the exclusion therefore of natural persons such as the parties to the association contract at issue in the main proceedings.

83 It should be pointed out in this regard that, since the Court does not have jurisdiction to interpret national law, it is for the referring court alone to determine whether it follows from the wording of Article 1251(18) and Article 127(8) of the Tax Code and from Government Decision No 44/2004 that the Romanian legislature exercised that option and that it could, at the time of the facts in the main proceedings, have been applicable to the parties to the association contract concerned.

84 Even if that had been the case, it is important that the Court, in order to give an answer that is helpful to the referring court, should provide it with information enabling it to assess whether the national legislation at issue in the main proceedings is consistent with the principles of proportionality and fiscal neutrality.

85 It is apparent from the Court’s case-law that Member States are, in the context of their margin of discretion, entitled to make the application of the scheme under Article 11 of the VAT Directive subject to certain restrictions provided that they fall within the objectives of that directive to prevent abusive practices and behaviour or to combat tax evasion or tax avoidance, and provided that EU law and its general principles, in particular the principles of proportionality and fiscal neutrality, are respected (judgment of 15 April 2021, Finanzamt für Körperschaften Berlin, C‑868/19, not published, EU:C:2021:285, paragraph 57 and the case-law cited).

86 It is thus for the referring court to determine whether the requirement of a prior declaration of registration by the members of the tax group to the competent tax authorities, set out in paragraph 4(5) of Government Decision No 44/2004, constitutes a measure which is necessary and appropriate to the achievement of the objectives of preventing abusive practices and behaviour or of combating tax evasion or tax avoidance (see, by analogy, judgment of 15 April 2021, Finanzamt für Körperschaften Berlin, C‑868/19, not published, EU:C:2021:285, paragraph 58 and the case-law cited).

87 As regards the principle of proportionality, national legislation which requires members of the tax group to register with the competent tax authorities before carrying out taxable transactions does not appear to go beyond what is necessary to achieve the objective of Article 11 of the VAT Directive, which is to prevent abusive practices or behaviour or to combat tax evasion or tax avoidance, in that it enables the tax authorities to identify the taxable person before those transactions are carried out, thereby facilitating tax inspections.

88 The principle of fiscal neutrality, which was intended by the EU legislature to reflect, in matters relating to VAT, the general principle of equal treatment, precludes in particular treating economic operators carrying out the same transactions differently for VAT purposes (see, to that effect, judgments of 17 December 2020, WEG Tevesstraße, C‑449/19, EU:C:2020:1038, paragraph 48 and the case-law cited, and of 15 April 2021, Finanzamt für Körperschaften Berlin, C‑868/19, not published, EU:C:2021:285, paragraph 65 and the case-law cited).

89 In the present case, the prior declaration by the tax group concerned to the competent tax authorities, imposed by the national legislation at issue in the main proceedings, appears to refer to the fact that those authorities keep a register of persons required to pay income or corporation tax and, therefore, that requirement cannot be interpreted as being contrary to the principle of fiscal neutrality.

90 It follows that, even if the provisions of national law referred to in paragraph 83 above constitute the transposition of Article 11 of the VAT Directive and those provisions were applicable to the parties to the association contract at issue in the main proceedings, Article 11 does not preclude such an association, which has no legal personality and has not been registered with the tax authorities before the transactions concerned commenced, from being unable to benefit from those provisions.

91 In the light of the foregoing, the answer to the first question is that Articles 9 and 11 of the VAT Directive must be interpreted as meaning that the parties to a contract relating to an association without legal personality, which was not registered with the competent tax authorities before the economic activity concerned commenced, cannot be regarded as ‘taxable persons’ along with the taxable person which is liable for tax on the taxable transaction.

The second question

92 By its second question, the referring court asks, in essence, whether the VAT Directive, the principle of proportionality and the principle of fiscal neutrality must be interpreted as meaning that a taxable person, where it does not hold an invoice issued in its name, must be granted the right to deduct the input VAT paid by another party to an association without legal personality with a view to carrying out that association’s economic activity.

93 According to settled case-law of the Court, the right of VAT deduction is a fundamental principle of the common system of VAT, which in principle may not be limited, and is exercisable immediately in respect of all the taxes charged on the taxable person’s input transactions (judgment of 10 February 2022, Grundstücksgemeinschaft Kollaustraße 136, C‑9/20, EU:C:2022:88, paragraph 47 and the case-law cited).

94 That system is designed to relieve the trader entirely of the burden of the VAT due or paid in the course of all his or her economic activities. The common system of VAT consequently ensures that all economic activities, whatever their purpose or results, provided that they are themselves subject to VAT, are taxed in a wholly neutral way (judgment of 10 February 2022, Grundstücksgemeinschaft Kollaustraße 136, C‑9/20, EU:C:2022:88, paragraph 48 and the case-law cited).

95 Under Article 167 of the VAT Directive, a right of deduction arises at the time when the deductible tax becomes chargeable. The substantive conditions which must be met in order for the right to arise are set out in Article 168(a) of that directive. Thus, for that right to be available, first, the person concerned must be a taxable person within the meaning of that directive and, secondly, the goods or services relied on to give entitlement to the right of deduction must be used by the taxable person for the purposes of his or her own taxed output transactions and those goods or services must be supplied by another taxable person as inputs (judgment of 21 November 2018, Vădan, C‑664/16, EU:C:2018:933, paragraph 39 and the case-law cited).

96 As regards the formal conditions for the right of deduction, it is apparent from Article 178(a) of the VAT Directive that the exercise of that right is subject to the holding of an invoice drawn up in accordance with Article 226 of that directive (judgment of 21 November 2018, Vădan, C‑664/16, EU:C:2018:933, paragraph 40 and the case-law cited).

97 The Court has held that the fundamental principle of the neutrality of VAT requires deduction of input VAT to be allowed if the substantive requirements are satisfied, even if the taxable persons have failed to comply with some formal conditions. It follows that the tax authorities cannot refuse the right to deduct VAT on the sole ground that an invoice does not satisfy the conditions required by Article 226(6) and (7) of the VAT Directive if they have available all the information to ascertain whether the substantive conditions for that right are satisfied (judgment of 21 November 2018, Vădan, C‑664/16, EU:C:2018:933, paragraph 41 and the case-law cited).

98 Thus, the strict application of the substantive requirement to produce invoices would conflict with the principles of neutrality and proportionality, inasmuch as it would disproportionately prevent the taxable person from benefiting from fiscal neutrality relating to his or her transactions (judgment of 21 November 2018, Vădan, C‑664/16, EU:C:2018:933, paragraph 42 and the case-law cited).

99 Nevertheless, it is for the taxable person seeking deduction of VAT to establish that he or she meets the conditions for eligibility (judgment of 21 November 2018, Vădan, C‑664/16, EU:C:2018:933, paragraph 43 and the case-law cited).

100 Accordingly, the taxable person is required to provide objective evidence that goods and services were actually provided as inputs by taxable persons for the purposes of his or her own transactions subject to VAT, in respect of which he or she has actually paid VAT (judgment of 21 November 2018, Vădan, C‑664/16, EU:C:2018:933, paragraph 44 and the case-law cited).

101 In the present case, it is apparent from the order for reference that BP and MB, who were responsible for the construction of the building complex at issue in the main proceedings, hold invoices drawn up in their names for the goods and services acquired personally for the purposes of that construction transaction, for the purposes of Article 168(a) and Article 178(a) of the VAT Directive, while ASA, who participated in the association by providing, with PP, the land on which that building complex was built, only holds invoices in her name for electricity services and tax receipts which she has submitted as having been paid by BP.

102 Having regard to the Court’s case-law cited in paragraphs 98 to 100 above, it is for ASA to provide objective evidence that goods and services connected with the construction of the building complex at issue in the main proceedings were actually provided as inputs by taxable persons for the purposes of her own transactions subject to VAT, namely the supply of immovable property, and in respect of which she has actually paid VAT, thereby avoiding the risk of double deduction of the same amount of VAT both by ASA and by BP and MB, which would infringe the principle of fiscal neutrality.

103 In the light of the foregoing, the answer to the second question is that the VAT Directive, the principle of proportionality and the principle of fiscal neutrality must be interpreted as meaning that a taxable person, where it does not hold an invoice issued in its name, must be granted the right to deduct the input VAT paid by another party to an association without legal personality with a view to carrying out that association’s economic activity, even if the taxable person is liable in respect of that activity, where there is no objective evidence that the goods and services at issue in the main proceedings were actually provided as inputs by taxable persons for the purposes of its own transactions subject to VAT.

The third question

104 By its third question, the referring court asks, in essence, if the answer to the second question is in the negative, whether the principle of legal certainty precludes a taxable person which is liable for the payment of VAT from being able to have other members of an association contract joined with a view to requiring them to pay VAT in proportion to their rights to the profits provided for in the association contract.

105 In that regard, it should be recalled that the principle of legal certainty, which is one of the general principles of EU law, requires that rules of law be clear, precise and predictable in their effects, especially where they may have negative consequences for individuals and undertakings, so that persons may ascertain unequivocally what their rights and obligations are and may take steps accordingly (judgment of 25 January 2022, VYSOČINA WIND, C‑181/20, EU:C:2022:51, paragraph 47 and the case-law cited).

106 The principle of legal certainty must be respected by national legislation which comes within the scope of EU law or implements it (see, to that effect, order of 17 July 2014, Yumer, C‑505/13, not published, EU:C:2014:2129, paragraph 37 and the case-law cited).

107 However, the referring court has failed to establish that an action brought by a taxable person against a third party for the purposes of obtaining, by means of an action on a warranty or guarantee, the repayment of input VAT comes within the scope of EU law or implements EU law, given that such an action on a warranty or guarantee is governed solely by national law.

108 In those circumstances, without evidence to support the conclusion that the VAT Directive is applicable to the situation referred to in the third question, that question is inadmissible.

Costs

109 Since these proceedings are, for the parties to the main proceedings, a step in the action pending before the national court, the decision on costs is a matter for that court. Costs incurred in submitting observations to the Court, other than the costs of those parties, are not recoverable.

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)