Since a few years the Dutch tax authorities have the policy that they publish an anonymized version of advance tax rulings that have been concluded between the tax authorities and taxpayers. On February 21, 2023 the Dutch tax authorities published an interesting ruling on the question whether or not in the underlying case the Dutch employees that work from their home offices constitute a Dutch permanent establishment of the foreign entity that employs them?

Summary of the facts

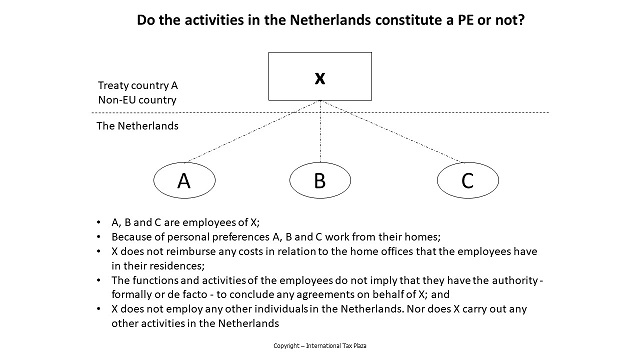

X is a company incorporated under the law of, and actually established in, a non-EU country with which The Netherland has concluded a Treaty for the Avoidance of Double Taxation (treaty country A). X is the headquarters of an internationally operating group which is active in the service sector. X is subject to a profits tax in treaty country A.

In 2021 and 2022, A, B and C, all individuals, have become employees of X. These employees are residents of the Netherlands and out of personal preferences they work from their homes in the Netherlands. X does not employ any other individuals in the Netherlands. Nor does X carry out any other activities in the Netherlands. X does not reimburse any costs in relation to the home offices that the employees have in their residences. The functions and activities of the employees do not imply that they have the authority - formally or de facto - to conclude any agreements on behalf of X.

The request for a ruling

X's request for certainty in advance confirming that there is no permanent establishment in the Netherlands regards the application of Article 3, Paragraph 4, sub a of the Dutch Corporate Income Tax (DCIT) Act in combination with Article 17, Paragraph 3, sub a of the DCIT Act. If based on the aforementioned articles it must be concluded that a permanent establishment or permanent representative exists, it subsequently has to be determined on the basis of the relevant provisions of the DTA as concluded between the Netherlands and treaty country A whether the Netherlands is allowed to levy taxes.

Legal context

Article 3, Paragraph 4, sub a of the DCIT Act

For the purposes of this Act and the provisions based thereon, permanent establishment or permanent representative means:

a. insofar as a treaty or an arrangement has been made in relation to the other state that provides for an arrangement regarding the taxation of elements of the profit: the concept of permanent establishment as it applies for the application of that arrangement.

(...)

Article 17, Paragraph 3, sub a of the DCIT Act

The Dutch income is the combined amount of:

a. the taxable profit from an enterprise carried on in the Netherlands, being the amount of the joint benefits obtained from an enterprise that, or part of an enterprise that is carried on through a permanent establishment in the Netherlands or a permanent representative in the Netherlands (Dutch enterprise);

(...)

Considerations of the Dutch tax authorities

In Paragraph 3, sub a of the Decree on preliminary consultations on rulings with an international character it is stated that access to such preliminary consultations to obtain certainty in advance in the form of a ruling with an international character is reserved for cases in which sufficient economic nexus exists in the Netherlands. In that same paragraph an exception to the aforementioned is made in the last sentence. In this sentence it is arranged means the provision regarding the necessary economic nexus by its very nature does not apply if certainty is requested regarding the absence of a permanent establishment in the Netherlands.

In addition, the saving of Dutch or foreign tax is not the sole or the decisive motive for executing the (legal) act(s) or transactions for which certainty in advance is requested. Nor does the requested certainty in advance relate to the tax consequences of direct transactions with entities that are located in states that are listed in the Arrangement low-taxing jurisdictions and non-cooperative jurisdictions for tax purposes (Regeling laagbelastende staten en niet-coöperatieve rechtsgebieden voor belastingdoeleinden).

Pursuant to Article 3, Paragraph 4, sub a of the DCIT Act, for the purposes of the DCIT Act, the term “permanent establishment” or “permanent representative” is understood to mean “permanent establishment” as it applies to the relevant provisions of the applicable DTA. Therefore it is directly assessed whether based on the relevant provisions of the applicable DTA the Netherlands will be entitled to levy taxes.

Based on the relevant provisions of the applicable DTA, a permanent establishment exists if X has a fixed place of business in which the business of the enterprise is wholly or partly carried on. However, if the activities carried on are solely of an auxiliary character, no permanent establishment will exist. Furthermore, based on the DTA a permanent establishment may exist if a person in the Netherlands is authorized to act on behalf and at the risk of X and that authorization is habitually exercised (permanent representative).

The employees perform activities on behalf of X from their home offices in the Netherlands. X has no other activities in the Netherlands. The homes of the employees are not at the disposal of X. This means that X does not have a fixed place of business in the Netherlands to its disposal. Consequently, the activities of X in the Netherlands do not lead to a permanent establishment as referred to in the DTA.

Also no situation exists in which the employees are authorized to conclude agreements on behalf of X and usually exercise that right. As a result also no permanent representative of X in the Netherlands exists.

Conclusion

In view of Article 3, Paragraph 4 of the DCIT Act in combination with the relevant provisions of the DTA as concluded between the Netherlands and treaty country A., for the application of the DCIT Act X does not exercise its business with the use of a permanent establishment in the Netherlands. This is laid down in a settlement agreement (advance tax ruling) with a validity from December 13, 2021 through December 31, 2025.

It is not completely clear to us how decisive the fact that the employees work from home out of personal preferences is for the outcome and whether the conclusion would be different if the employees would have worked from home because their foreign employer demanded them to do so (for example because of measures the employer took with respect the covid pandemic)? In principle we would say it shouldn't make a difference since generally speaking activities that are solely of an auxilliary nature do not constitute a pe under a DTA. Also not if the taxpayer has a place of business to its disposal in the Netherlands. However since a specific reference is made to the fact that the employees work from home out of personal preferences, it will nevertheless be interesting to see whether any further rulings will be published in this respect.

Here you can download the full text of the anonymized ruling as available on the website of the Dutch tax authorities. (only available i9n the Dutch language)

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter (@IntTaxPlaza)