Last week I finally took the time to study and digest the Pillar Two model rules that the OECD released on December 20, 2021 and the thereupon based proposal of the European Commission for an EU Council Directive on ensuring a global minimum level of taxation for multinational groups in the Union that was published on December 22, 2021. And what I envisioned to take a day, quickly turned out to take much longer than I expected.

This article basically functions as the introduction to a set of 9 seperate articles which provide information to each of the 9 steps identified below. Links to each of these nine articles you can find at the bottom of this article.

The article is mainly based on the European Commission’s proposal for a Council Directive on ensuring a global minimum level of taxation for multinational groups in the Union. The reason here for is twofold:

1. The first and most obvious one is that I am an EU-resident; and

2. Because both documents are similar, but somehow I found the Commission’s proposal more reader friendly.

Although the rules laid down in both documents are similar, one very clear distinction between both sets of rules is that where the OECD Model rules only apply to large-scale international (MNE) groups that meet certain conditions, the rules laid down in the European Commission’s proposal for a Directive also apply to pure domestic large-scale groups.

IIR and UTPR

Both the OECD Model Rules and the proposed EU Directive establish common measures for the minimum effective taxation of (MNE) groups in the form of:

(a) an Income Inclusion Rule (IIR) in accordance with which a parent entity of a (MNE) group computes and collects its allocable share of top-up tax in respect of the low-taxed constituent entities of the group; and

(b) an UnderTaxed Payments Rule (UTPR) in accordance with which a constituent entity of a MNE group collects an allocable share of top-up tax computed by the ultimate parent entity (UPE) of the group that was not charged under the IIR in respect of the low-taxed constituent entities of the group.

What will I discuss in this set of articles?

As stated above in this set of articles I will mainly focus on the Commission’s proposal for a Directive. However, since the proposed Directive is the EU’s proposal to implement the OECD Model Rules most remarks will also apply to the OECD Model Rules. In this set of articles my main focus will be on what my approach would be if I would have to apply the regulations to a (MNE) group and I tried to make some sort of a workplan on how to efficiently work with the proposed Directive and proposed OECD Pillar 2 regulations. Therefore, I will try to do my best not to go into too much detail (which I might do in future articles).

I am aware that the articles and my workplan certainly are not yet perfect. The workplan is still work in progress and many questions still have to be answered and even more remarks can be made. Still, I decided to share it and hopefully this set of articles is somehow helpful for tax specialists that will have to work with either the proposed OECD Model Rules or the proposed EU Directive.

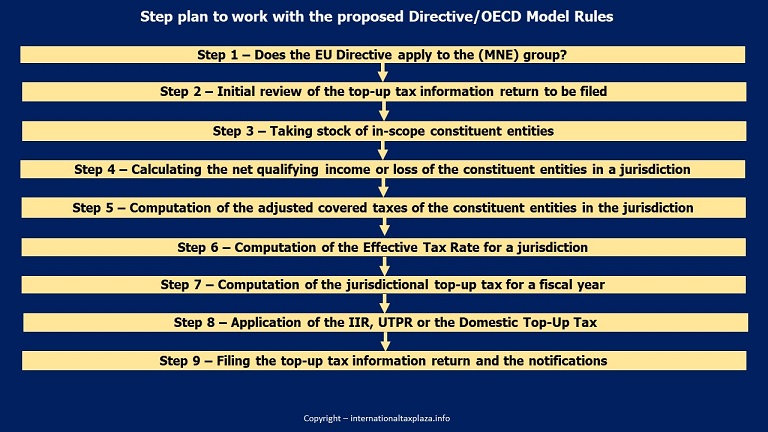

As stated in my approach I have identified 9 steps. To keep my approach readable I have drafted 9 articles in which I describe what is to be done in each of the 9 identified steps, what information you need to gather, etc. The links below forward you to the article I drafted with respect to each separate step. Furthermore in each article I have included links that forward you to definitions of the terms used:

· Step 1 – Does the EU Directive apply to the (MNE) group?

· Step 3 – Taking stock of in-scope constituent entities

· Step 4 – Calculating the net qualifying income or loss of the constituent entities in a jurisdiction

· Step 5 – Computation of the adjusted covered taxes of the constituent entities in the jurisdiction

· Step 6 – Computation of the Effective Tax Rate for a jurisdiction

· Step 7 – Computation of the jurisdictional top-up tax for a fiscal year

· Step 8 – Application of the IIR, UTPR or the Domestic Top-Up Tax

· Step 9 – Filing the top-up tax information return and the accompanying notifications

The text of the proposed EU Directive can be found here.

Copyright – internationaltaxplaza.info

Follow International Tax Plaza on Twitter