- Details

In this edition: IFRS – IFRS Interpretations Committee March 2016 (Agenda point 5 is interesting - IAS 12 - Income Taxes: Accounting for income tax consequences of payments on financial instruments that are classsified as equity); Australia – Automatic exchange of information - guidance material; Poland – MF docenia inicjatywę KE w sprawie zmian w VAT

Read more: International Tax Plaza’s Quick News from April 7, 2016

- Details

On April 7, 2016 the Court of Justice of the European Union (CJEU) judged in Case C‑546/14 Degano Trasporti Sas di Ferruccio Degano & C., in liquidation (intervening party: Pubblico Ministero presso il Tribunale di Udine), (ECLI:EU:C:2016:206).

On a proper construction, do the principles and rules contained in Article 4(3) TEU and the VAT Directive, as already interpreted in the judgments of the Court of Justice in Commission v Italy (C‑132/06, EU:C:2008:412), Commission v Italy (C‑174/07, EU:C:2008:704) and Belvedere Costruzioni (C‑500/10, EU:C:2012:186), also preclude a national rule (and, therefore, in respect of the case in the main proceedings, an interpretation of Articles 162 and 182ter of the Law on bankruptcy) under which a proposal for an arrangement with creditors with the liquidation of the debtor’s assets, which provides for only partial payment of the State’s claim in respect of VAT, is permissible where there is no tax settlement and where, in respect of that claim, a larger payment in the event of bankruptcy is not foreseeable on the basis of an assessment by an independent expert and following the formal review of the court?

- Details

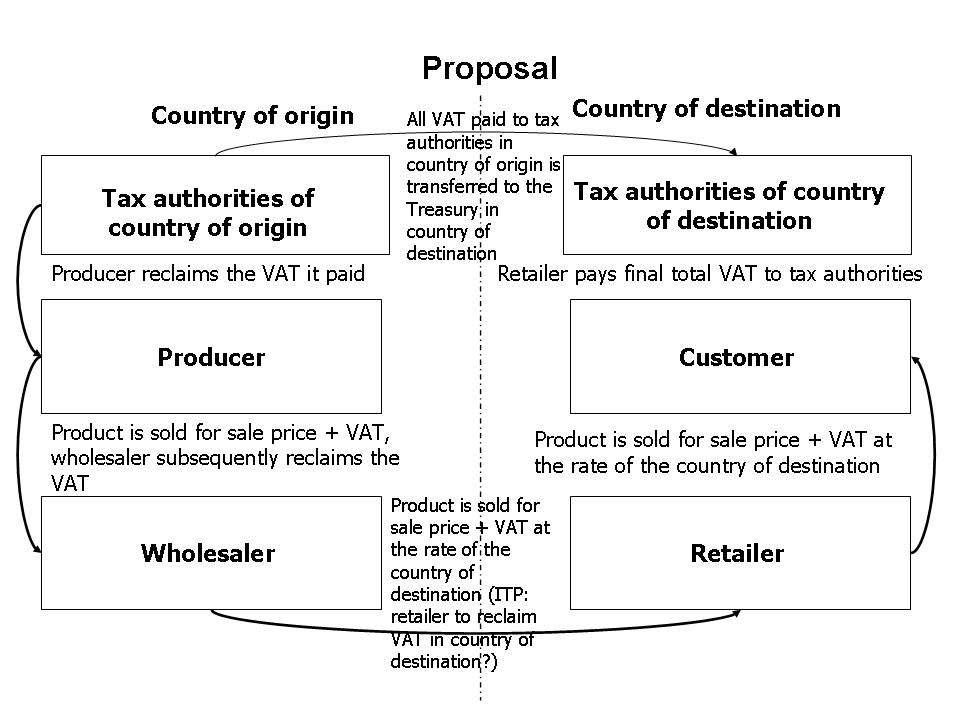

On April 7, 2016 the European Commission presented its long awaited Action Plan on VAT.

The Action Plan identifies the following 4 main key actions:

· Recent and ongoing policy initiatives

· Urgent measures to tackle the VAT Gap

· Towards a robust single European VAT area

· Towards a modernised VAT rates policy

In its Action Plan the European Commission provides a high-level overview of the ideas it has with respect to the different key actions mentioned above. The Action Plan also provides insight in when the Commission expects to present legislative proposals with respect to each of the key actions.

Read more: The European Commission presents its Action Plan on VAT

- Details

In this edition: CJEU - Opinion of Advocate General Saugmandsgaard Øe delivered in C-24/15; Plöckl; Australia – NATIONAL INNOVATION AND SCIENCE AGENDA – INTANGIBLE ASSET DEPRECIATION; Australia – NATIONAL INNOVATION AND SCIENCE AGENDA – INCREASING ACCESS TO COMPANY LOSSES; IMF – Opening Address at the Open Workshop on International Taxation of the 7th IMF-Japan High Level Tax Conference for Asian Countries

Read more: International Tax Plaza’s Quick News from April 6, 2016

- Details

On April 6, 2016 the OECD published the public comments received on its discussion draft on the treaty residence of pension funds, which it released on February 29, 2016. The OECD invited interested parties to comment on a discussion draft that includes proposals for changes to the OECD Model Tax Convention concerning the treaty residence of pension funds.

Page 6 of 7